Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

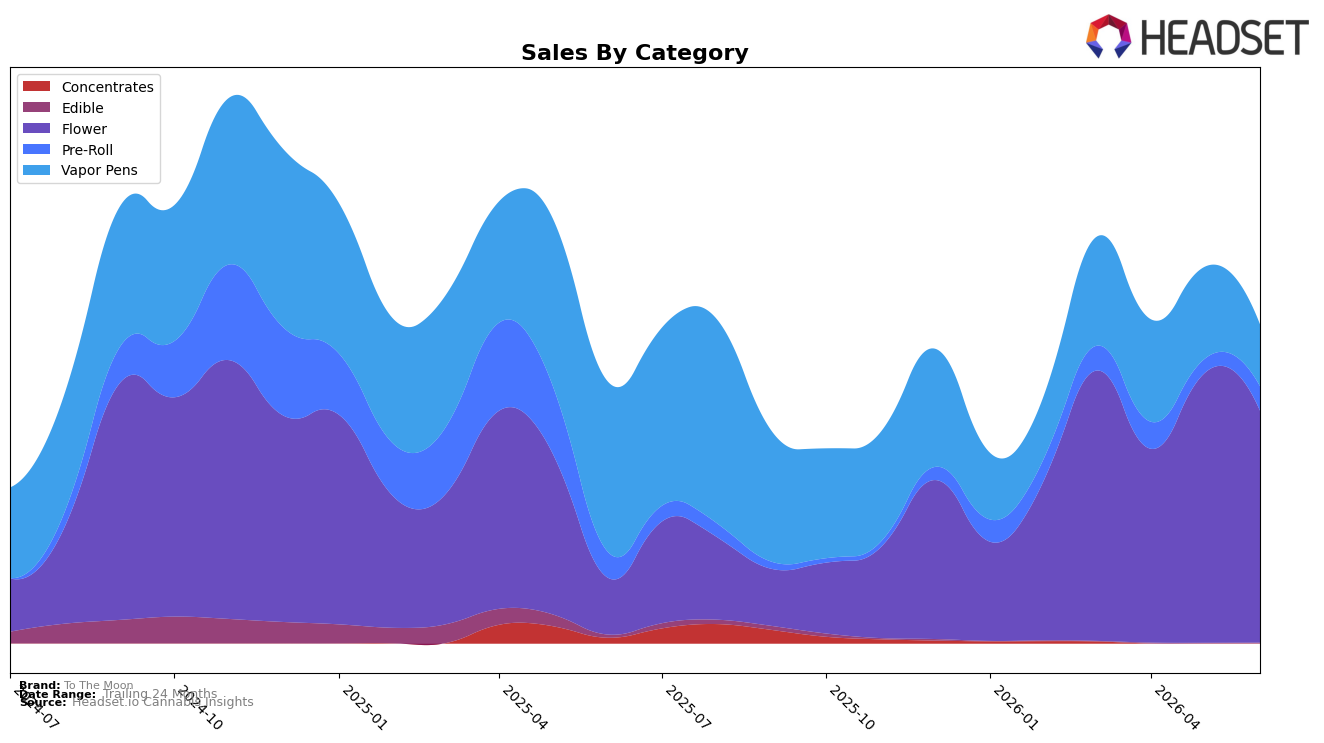

In June 2026, To The Moon concentrated 72.82% of sales in Flower, where year-over-year growth reached 311.17% even as month-over-month slipped 14.04%, while Vapor Pens fell to a 19.37% share with a 63.76% YoY drop and a 32.88% MoM decline. Pre-Roll expanded its role to 7.64% share with a 74.52% MoM surge despite a 4.50% YoY dip, and Edible remained minimal at 0.17% share with an 81.71% YoY contraction but a 45.43% MoM uptick. With average price down 5.78% YoY to $37.17 and Flower anchoring the portfolio, the pattern implies deliberate mix consolidation into lower-priced Flower volume while pruning underperforming Vapor Pens.

Positioning-wise, the 311.17% YoY spike in Flower alongside a 14.04% MoM pullback suggests the brand is pivoting to defend a mid-pack placement in Flower, reflected by a rank of 21 in New York, while using Pre-Roll’s 74.52% MoM lift as a secondary entry point. The 63.76% YoY decline in Vapor Pens combined with a 32.88% MoM slide indicates a retreat from a premium-extraction stance, and the 5.78% YoY drop in average price coupled with Flower’s 72.82% share signals a value-forward Flower-led identity that trades margin for share stability.

Competitive Landscape

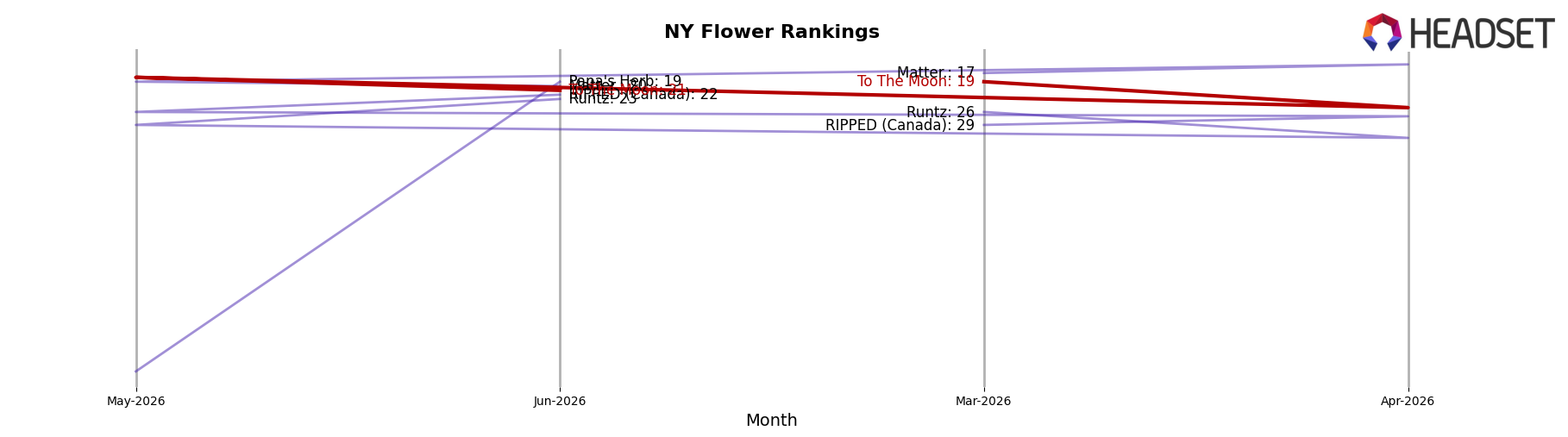

To The Moon sits at rank #21 in NY Flower in June 2026, improving 40 places year over year from #61, but slipping 2 spots since March 2026 when it was #19; the brand remains 9 ranks below its September 2024 peak at #12, indicating recovery but not yet a return to peak positioning. In contrast, Find. climbed from #3 to #1 while growing sales 35.6% year over year, and Leal advanced from #7 to #2 with a 44.4% YoY sales increase, whereas Dank. By Definition slipped from #1 to #3 alongside a 50.7% YoY sales decline; this mix suggests To The Moon’s 40-rank YoY jump is tied more to mid-tier share churn than to top-tier displacement, implying the trajectory points to opportunistic gains that require conversion into sustained top-15 presence.

Notable Products

Blue Dream (3.5g) posted the steepest decline in June 2026 at -52.9% MoM, sliding to rank 8, while Northern Lights (3.5g) surged +52.3% MoM to rank 1. Cookies & Cream (3.5g) inched up just +1.7% MoM yet held rank 3, and eight of the top ten are Flower SKUs, concentrating mix in a single category. The split between a +52.3% gainer at the top and a -52.9% laggard mid-pack implies To The Moon is reallocating velocity toward a narrower set of flagship Flower SKUs, prioritizing leaders over breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.