Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

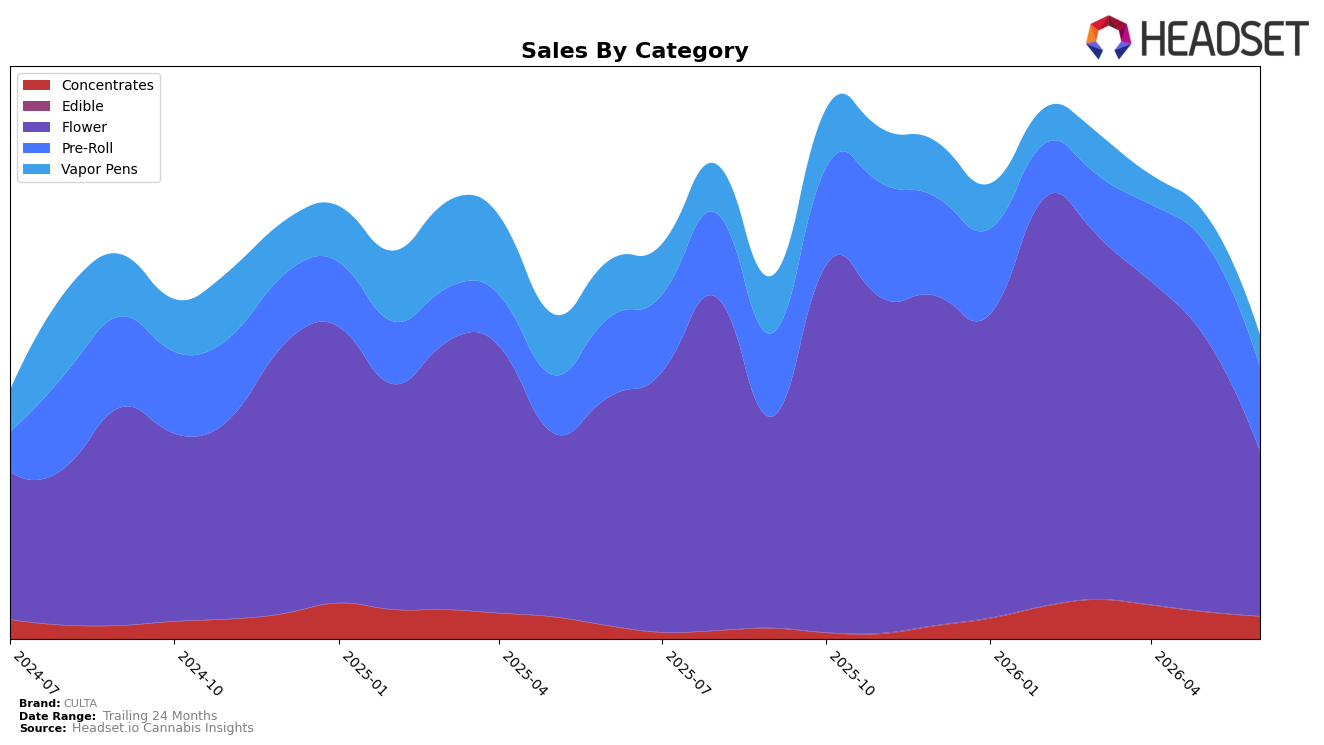

In June 2026, CULTA’s mix tilted toward Flower at 54.42% share, but Flower contracted by 27.67% year over year and 40.01% month over month, pulling overall momentum down even as average price ticked up 0.28%. Pre-Roll rose 6.41% year over year to 27.73% share but slipped 11.04% month over month, indicating the gain is not consistent across time frames; meanwhile, Vapor Pens fell 44.22% year over year yet grew 11.82% month over month to 10.48% share. Concentrates expanded 72.72% year over year but declined 16.75% month over month at 7.37% share, signaling volatility at a small base. With a 17th-place Flower rank in Maryland, the pattern implies overreliance on a shrinking lead category is suppressing total performance while secondary formats are too small or unstable to offset the drag.

The cross-current of a 27.67% Flower decline alongside a 6.41% Pre-Roll increase and a month-over-month 11.82% lift in Vapor Pens implies CULTA’s demand is fragmenting toward lower-price or convenience formats without yet achieving scale. Given Concentrates’ 72.72% year-over-year surge but 16.75% month-over-month dip, the brand’s gains appear episodic rather than embedded, and the 40.01% month-over-month Flower drop suggests sensitivity to supply, pricing, or promo cadence. The thesis is that CULTA’s positioning is anchored in Flower where it holds rank 17 in Maryland, but durable share growth likely depends on converting recent category interest in Pre-Roll and Vapor Pens into sustained mix expansion that reduces exposure to Flower volatility.

Competitive Landscape

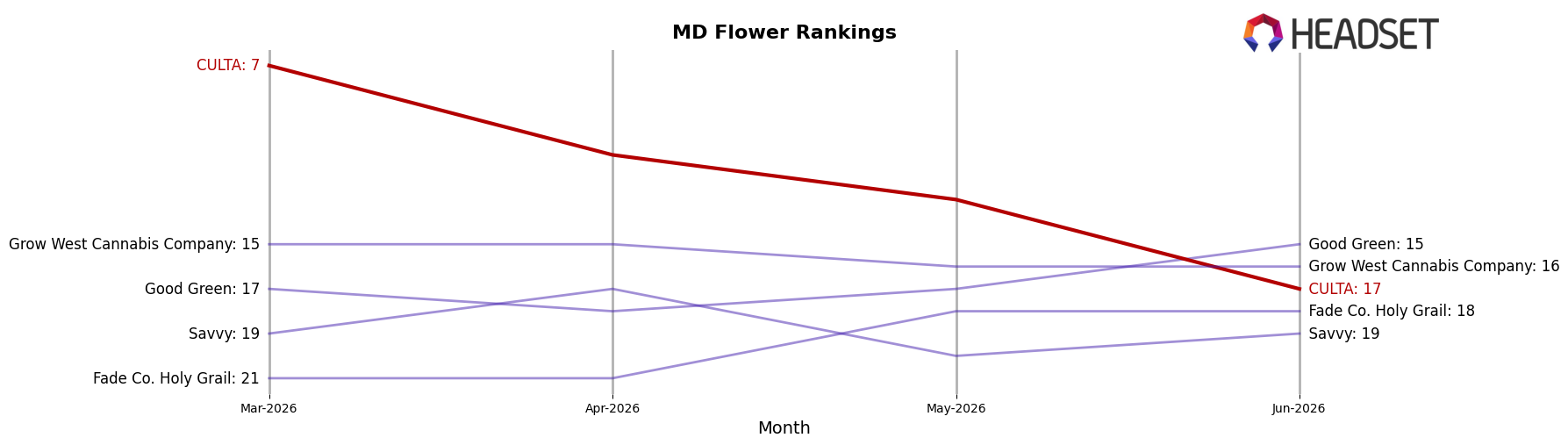

CULTA sits at rank #17 in June 2026, unchanged YoY from rank #17, but down 10 positions from rank #7 in March 2026, while SunMed held at #1 YoY (from #1 to #1) and RYTHM climbed from #3 to #2 with 42.7% YoY sales growth; by contrast, CULTA’s trajectory from a peak of #7 in March 2026 to #17 by June 2026 implies share leakage to higher-momentum leaders as Strane advanced from #7 to #4 on 58.8% YoY growth, and Fade Co. eased from #2 to #3 despite 23.7% YoY growth, signaling that CULTA’s stall at #17 amid competitors’ rank gains points to a mix issue or distribution pressure rather than category contraction.

Notable Products

Apollo 22 Pre-Roll 2-Pack (1g) jumped 144.9% month over month to rank 1 in June 2026, while Amnesia OG Pre-Roll 5-Pack (2.5g) plunged 72.8% to rank 10, indicating volatility concentrated at the edges of the lineup. Amnesia OG (3.5g) fell 33.0% but still held rank 2, and Lava Lamp (3.5g) declined 41.5% at rank 8, whereas Zest Bomb (14g) in Flower grew 6.9% at rank 9, pointing to mixed momentum within Flower even as Pre-Roll produces the top slot. Four of the top ten are Pre-Roll SKUs spanning ranks 1, 3, 5, and 10, and the Poonesia Pre-Roll 7-Pack (3.5g) sits at rank 7 with $54,353, suggesting multi-pack Pre-Rolls are anchoring traffic despite uneven performance across formats.

The pattern implies CULTA is leaning into Pre-Roll variety and value-pack formats to capture share at the top of the chart, while core Flower faces sharper rank-risk from double-digit declines and depends on larger-size offerings to stabilize demand.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.