Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

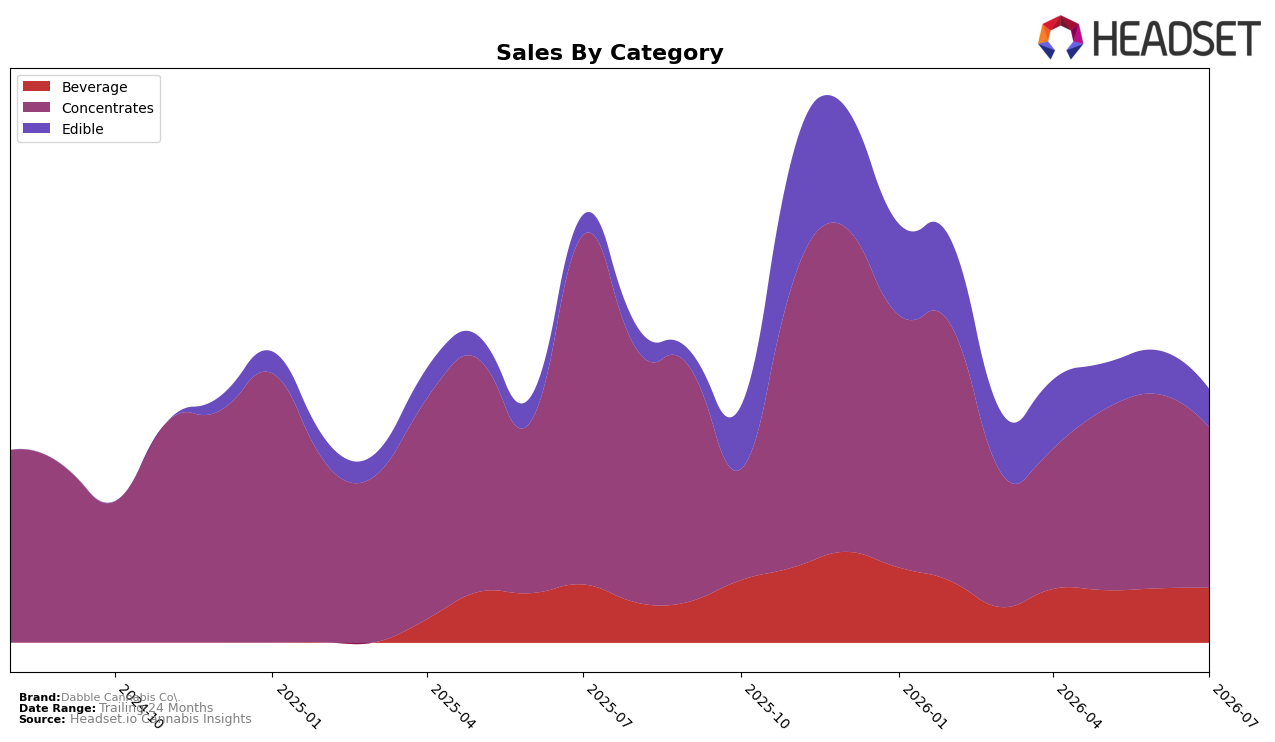

Dabble Cannabis Co. concentrated 63.26% of July 2026 sales in Concentrates, down 17.37% month over month and 54.10% year over year, while Beverage held 21.63% share with a 1.11% MoM increase and a 5.67% YoY decline; Edible reached 15.11% share after a 12.22% MoM pullback despite a 91.04% YoY surge. The brand’s average price fell 27.36% YoY to $21.25 as category-level averages ranged from $49.61 in Concentrates to $10.14 in Beverage, indicating mix and pricing pressure that helps explain the 40.70% YoY sales decline even as the brand maintained rank 7 in Concentrates in British Columbia; the pattern implies reliance on a contracting flagship category while lower-priced formats provide only partial volume offset.

The shift toward a larger Beverage and Edible footprint at 36.74% combined share alongside a 63.26% Concentrates core positions Dabble Cannabis Co. as a value-leaning multi-format player rather than a pure premium extract specialist, given the 27.36% YoY average price decrease and the 91.04% YoY Edible growth counterbalanced by a 54.10% YoY Concentrates decline. Holding rank 7 in British Columbia Concentrates while Concentrates fell 17.37% MoM and Edible fell 12.22% MoM suggests short-term share defense in the flagship lane but limited category-level insulation; the implication is that sustaining position will likely require either reclaiming Concentrates velocity at higher price points or accelerating Beverage and Edible mix gains where price bands near $10–$12 can drive unit throughput without further compressing margin.

Competitive Landscape

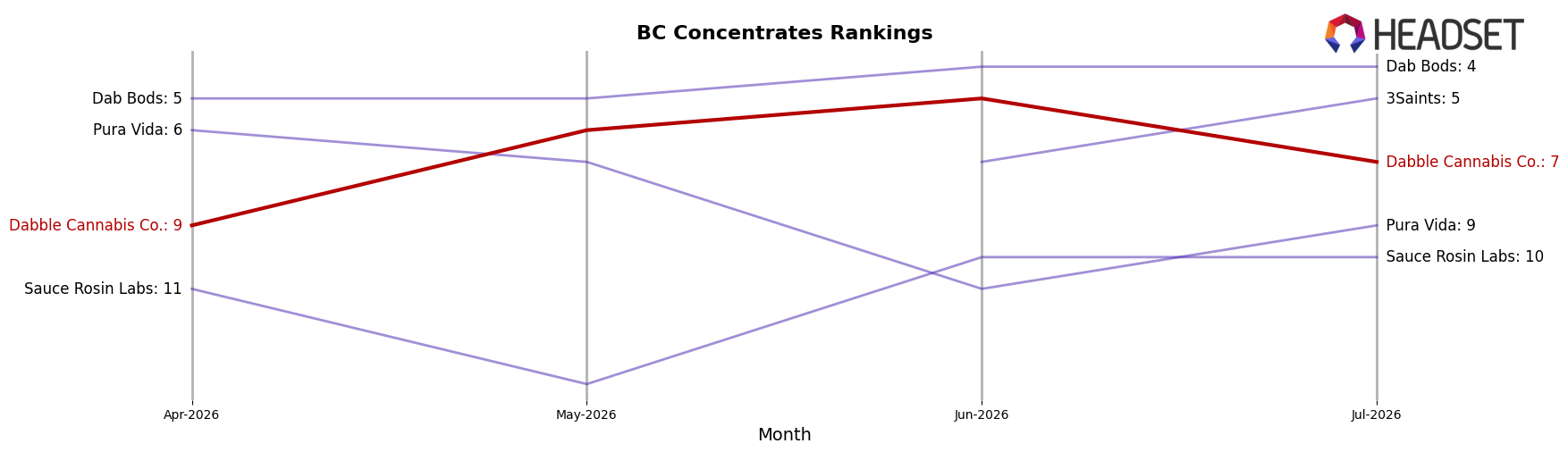

Dabble Cannabis Co. sits at rank #7 in BC Concentrates in July 2026, up 3 positions year over year and 2 spots from April 2026, after peaking at #3 in February 2026; meanwhile, BoxHot climbed from #8 to #3 with 98.8% YoY sales growth and Endgame held #1 while contracting 9.4% YoY, indicating Dabble’s mid-pack rise is occurring amid both aggressive upward mobility and top-tier softening. Compared with 3Saints jumping from #13 to #5 on 86.8% YoY growth and Vortex Cannabis Inc. staying at #2 despite a 27.4% YoY decline, the mix of rank gains against shrinking leaders and surging challengers implies Dabble’s trajectory toward #7 is sustainable only if it converts its February 2026 peak into steadier share capture rather than episodic spikes, especially as Dab Bods at #4 posts 17.8% YoY growth.

Notable Products

Strawberry Jam Raspberry Sparkling Lemonade (10mg THC, 355ml) posted the largest move in July 2026, up 55.7% month over month to rank 1, while Blackberry Sparkling Lemonade (10mg THC, 12oz, 355ml) fell 33.4% and slid to rank 2; that divergence inside Beverages implies a flavor-led reordering of the lineup rather than a category-wide lift. In Concentrates, Strawberry Jam Live Rosin (1g) rose 34.2% to rank 4, whereas Dabbleberry Live Rosin (1g) dropped 42.8% and Mexicola Live Hash Rosin (1g) declined 17.7%, placing ranks 5 and 6 respectively; the mixed results within three top-10 Concentrates suggest strain-specific momentum is displacing legacy SKUs. Four of the top ten are Concentrates and three are Edibles, but Edibles skew negative with Strawberry Jam Gummies 10-Pack (100mg) down 16.0% and Strawberry Jam Gummies 2-Pack (10mg) down 35.7% while DabbleBerry Gummies 2-Pack (10mg) rose 19.8%, indicating portfolio energy is consolidating around a few hero flavors rather than broad category strength; the $41,397 haul for Strawberry Jam Live Rosin (1g) reinforces the tilt toward premium inputs. Overall, the product mix points to Dabble Cannabis Co. leaning into Strawberry Jam-branded extensions and high-THC rosin formats, reallocating attention away from underperforming Edibles and select legacy Concentrates.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.