Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

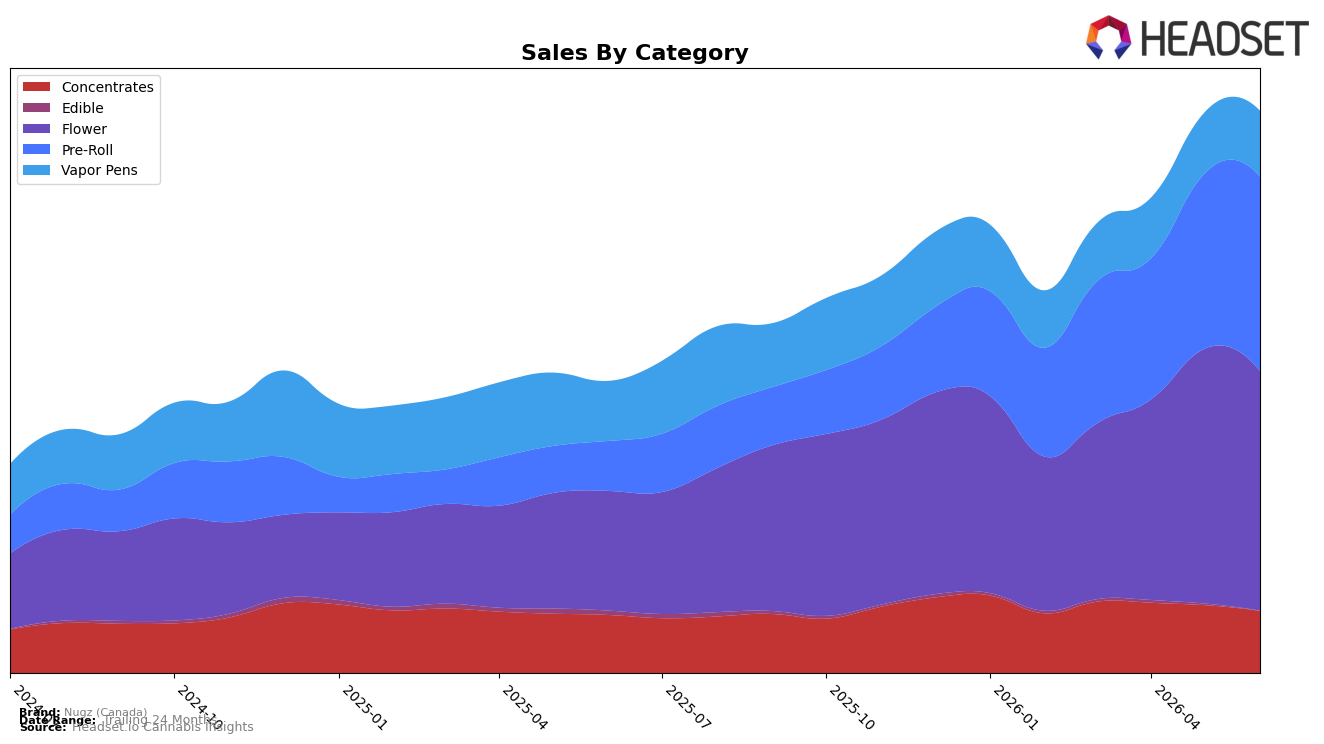

In June 2026, Nugz (Canada) concentrated 42.52% of sales in Flower with 99.87% year-over-year growth but a 6.00% month-over-month decline, while Pre-Roll expanded to 34.54% share with 288.10% year-over-year growth and a 10.88% month-over-month increase. Vapor Pens held 11.74% share with 9.69% year-over-year and 7.73% month-over-month growth, whereas Concentrates at 11.10% share grew 7.12% year-over-year but fell 8.29% month-over-month; Edible contracted to 0.09% share with year-over-year and month-over-month declines of 89.54% and 74.02%, respectively. With Flower anchoring assortment yet slipping sequentially and Pre-Roll accelerating, the mix implies a pivot toward combustibles variety; this tilt, alongside a 23.37% year-over-year rise in average price and a brand-wide 92.05% year-over-year sales increase, points to volume and pricing gains being pulled more by Pre-Roll and Vapor Pens in June 2026 than by Flower.

Nugz (Canada) ranked 7th in Flower in Ontario, indicating headroom to trade up share even as Flower’s month-over-month softness contrasts with Pre-Roll’s 10.88% sequential lift and Vapor Pens’ 7.73% increase. Given Pre-Roll’s surge to 34.54% mix alongside Flower’s 42.52% and Concentrates’ 8.29% month-over-month pullback, the portfolio is reallocating demand toward faster-turn inhalables that can sustain the 92.05% brand sales year-over-year growth; the positioning implication is to lean into Pre-Roll and Vapor Pens to stabilize rank pressure in Flower while the 23.37% higher average price supports margin without over-reliance on Concentrates or Edible.

Competitive Landscape

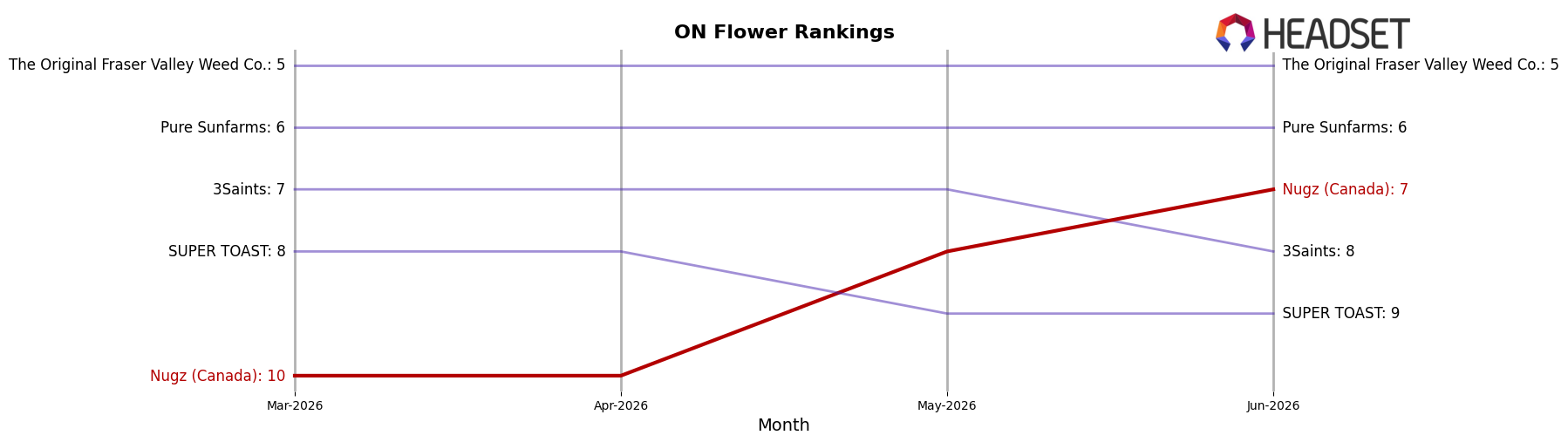

Nugz (Canada) sits at rank #7 in ON Flower in June 2026, improving 12 positions from #19 year over year and climbing 3 spots from #10 since March 2026, while also marking a peak rank of #7 in June 2026; meanwhile, Spinach is positioned at #1 after rising from #4 year over year with sales up 38.3%, and Back Forty / Back 40 Cannabis slipped from #1 to #4 with sales down 11.3%, indicating Nugz (Canada) is closing the competitive gap on fallen incumbents faster than on accelerating leaders, which implies a trajectory toward sustained mid-top-tier presence rather than imminent top-3 contention.

Notable Products

Florida Oranges (7g) posted the steepest decline in June 2026 at -36.3% MoM, sliding to rank 6, while Florida Oranges Pre-Roll 7-Pack (3.5g) fell -13.2% to rank 3; together these drops contrast with Flavour Bomb 40 - Fruit Blast Taster Pack Infused Pre-Roll 5-Pack (2.5g), which rose +22.2% and held rank 1. Four of the top ten are Pre-Roll SKUs, and the category’s consistency at ranks 1–4 against Flower softening at ranks 6–9 implies mix is tilting toward infused and format-driven convenience rather than larger-size flower value.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.