Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

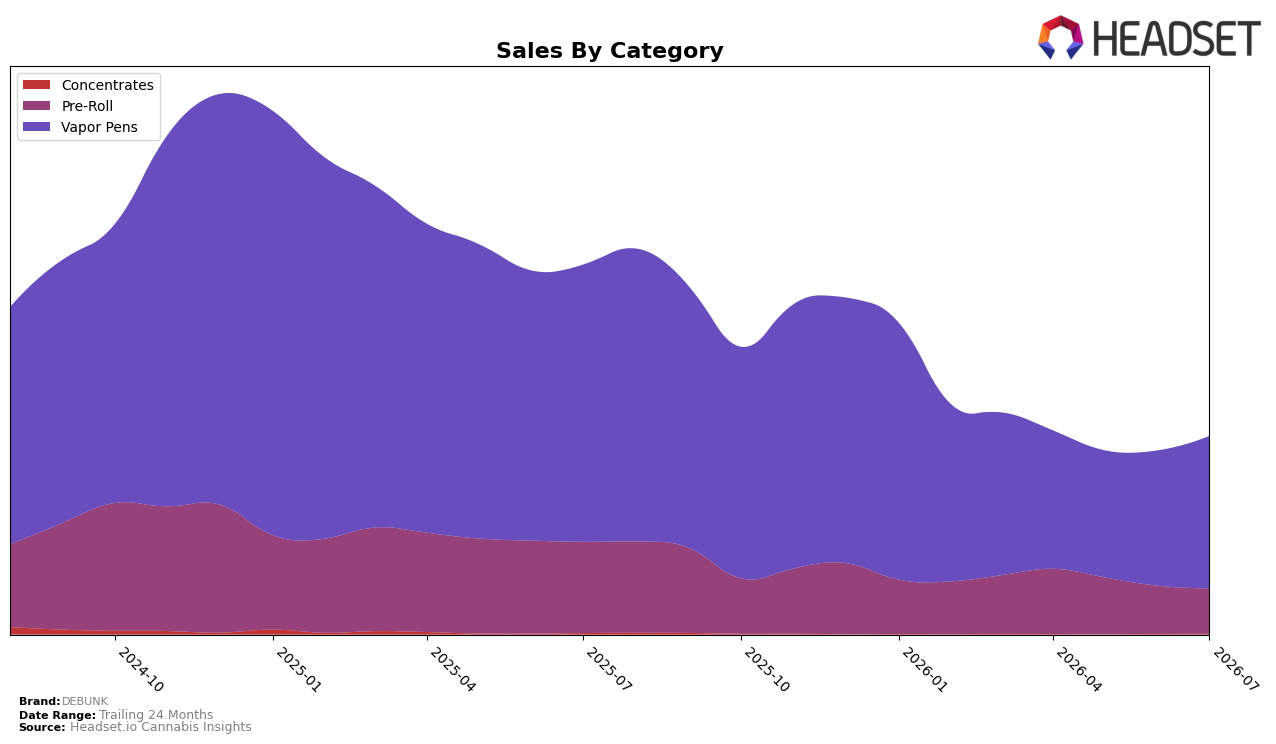

In July 2026, DEBUNK concentrated 76.74% of sales in Vapor Pens with a month-over-month rise of 12.51% but a year-over-year decline of 45.10%, while Pre-Roll held 22.93% share with a 5.52% MoM drop and a 50.09% YoY contraction. Concentrates remained marginal at 0.32% share despite a 23.91% MoM uptick and a 55.41% YoY decline, and the brand’s average price fell 3.38% YoY to $33.54. The pattern implies a portfolio leaning harder into Vapor Pens for near-term volume recovery while Pre-Roll retrenches, with small-bet experimentation in Concentrates not yet moving mix.

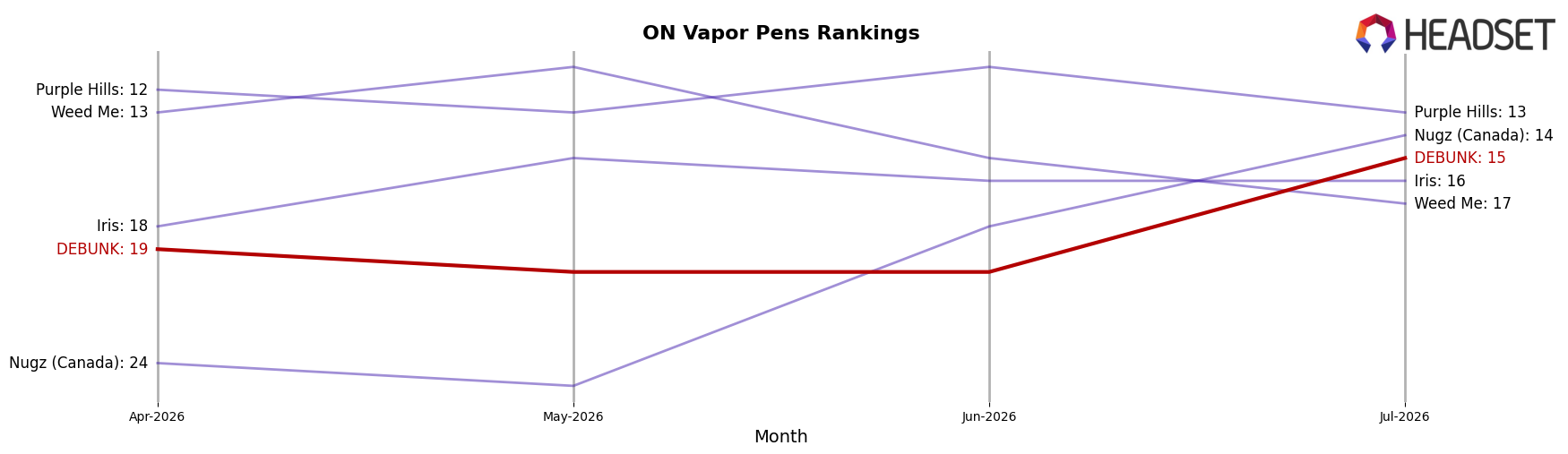

Within Vapor Pens, DEBUNK’s rank at 15 in Ontario signals mid-pack placement even as the category mix skews 76.74% toward this format and Pre-Roll sits at 22.93%. The juxtaposition of a 12.51% MoM lift in Vapor Pens alongside a 5.52% MoM pullback in Pre-Roll suggests positioning anchored to pen-centric buyers, while the 3.38% YoY price reduction paired with a 45.10% YoY decline in Vapor Pens indicates the current price architecture is not yet translating to share gains; the implication is that DEBUNK’s competitive footing depends on refining Vapor Pen differentiation rather than broadening into low-share niches.

Competitive Landscape

DEBUNK is ranked #15 in ON Vapor Pens in July 2026, down 6 positions from #9 in July 2025, and 4 spots better than #19 in April 2026, while its peak of #4 in January 2025 underscores how far the brand has retreated in placement; in contrast, Spinach climbed to #1 from #4 year over year with 144.7% sales growth, and Back Forty / Back 40 Cannabis holds #2 after improving from #1 with 9.3% YoY growth, indicating DEBUNK’s trajectory is drifting away from the category’s leaders rather than converging back toward its former top-5 position.

Notable Products

Peach Crescendo Liquid Diamonds Disposable (1g) posted the standout move with an 81.5% month-over-month surge to rank 3 in July 2026, while Darts - Sour ZKZ Bubble Hash Infused Pre-Roll 5-Pack (2.5g) sank 38.6% to rank 10, marking a bifurcation between fast-rising disposables and pressured infused pre-rolls. ICE - Moon Drops Liquid Diamonds Cartridge (1g) held rank 1 despite a 4.2% decline, and ICE - Melonade Liquid Diamond Cartridge (1g) slipped 3.3% at rank 7, while Vapor Pens accounted for seven of the top ten slots, indicating concentrated momentum in inhalables over traditional pre-rolls. The pattern implies DEBUNK’s commercial direction is pivoting toward disposable and cartridge formats where mix and velocity can offset softness in select infused pre-rolls.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.