Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

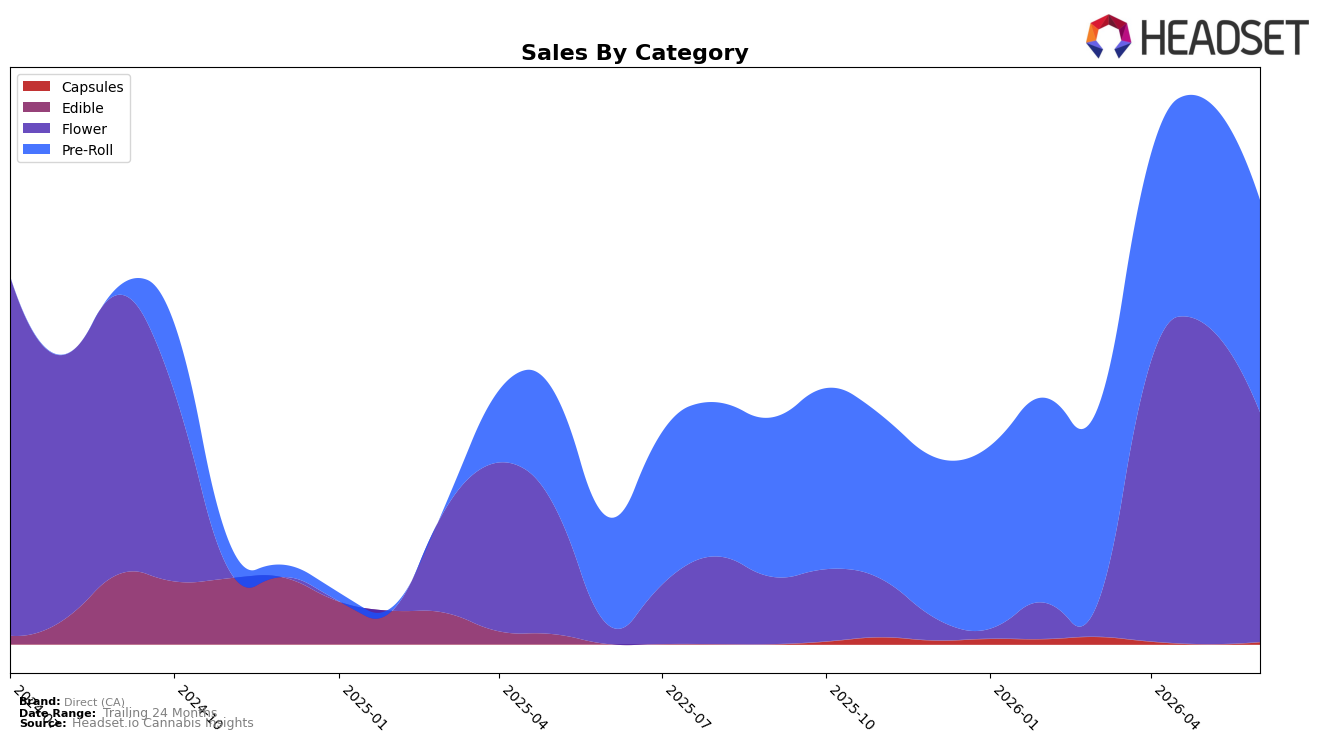

Direct (CA) concentrated almost entirely in Flower and Pre-Roll in June 2026, with Flower rising to 51.7% share on 1,122.4% year-over-year growth while dropping 28.3% month-over-month, and Pre-Roll holding 47.8% share on 97.0% year-over-year growth with a 5.6% month-over-month decline. Capsules remained a rounding error at 0.49% share with no observable year-over-year or month-over-month signal, and the brand’s average price fell 45.6% year-over-year to $6.28, contrasting with a Flower average of $12.38 and a Pre-Roll average of $4.08. The mix implies June 2026 was a volume-heavy month driven by aggressive pricing, where share leadership in Flower despite a double-digit month-over-month pullback suggests inventory or promotional timing shaped category balance more than demand erosion.

The widening gap between Flower’s triple-digit year-over-year surge at 1,122.4% and its 28.3% month-over-month contraction, versus Pre-Roll’s 97.0% year-over-year lift and 5.6% month-over-month dip, signals that Direct (CA)’s positioning leans into episodic Flower pushes while maintaining steadier Pre-Roll velocity. With California as the top market and Pre-Roll rank data unavailable, the brand’s near-even split between Flower at 51.7% share and Pre-Roll at 47.8% share indicates purposeful dual-category coverage, where lower average prices likely expand basket conversion while exposing monthly results to promo cadence swings; the implication is that sustaining share will require smoothing Flower’s promotional cycles to prevent recurring month-over-month troughs.

Competitive Landscape

Direct (CA) sits at rank #102 in CA Pre-Roll in June 2026, improving 35 positions year over year from #137, and edging up 3 spots since March 2026 while briefly peaking at #99 in May 2026; by contrast, CannaBiotix (CBX) advanced from #7 to #4 with a 39.09% YoY sales increase and Jeeter held #1 with 0.66% YoY growth. This relative movement implies Direct (CA)’s rank gains are coming from incremental, lower-tier share consolidation rather than head-to-head displacement of top leaders, suggesting a trajectory of slow climb that will require sharper differentiation to convert rank volatility near #100 into durable top-75 penetration.

Notable Products

Jack Herer Pre-Roll (1g) posted the steepest movement in June 2026 with a -25.4% month-over-month slide while dropping to rank 3, whereas Skywalker OG Pre-Roll (1g) held rank 1 despite a -9.0% decline and Lemon Haze Pre-Roll (1g) rose 19.3% at rank 2. Four of the top ten are Pre-Roll SKUs clustered at ranks 1–6, and Flower entries sit at ranks 7–10 with Astronaut Sugar Shake (14g) up 48.5% and Astronaut (3.5g) down 22.0%, indicating category bifurcation rather than uniform momentum. The presence of two new or reintroduced Flower placements at ranks 8 and 10 alongside a single raw revenue mark of $13,685 for Astronaut Sugar Shake (14g) points to value-driven Flower gaining shelf traction even as flagship Pre-Rolls consolidate share. The pattern implies Direct (CA) is leaning into a barbell mix: premium-named Pre-Rolls anchoring the top ranks while value-oriented Flower rebounds to capture budget-sensitive demand.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.