May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

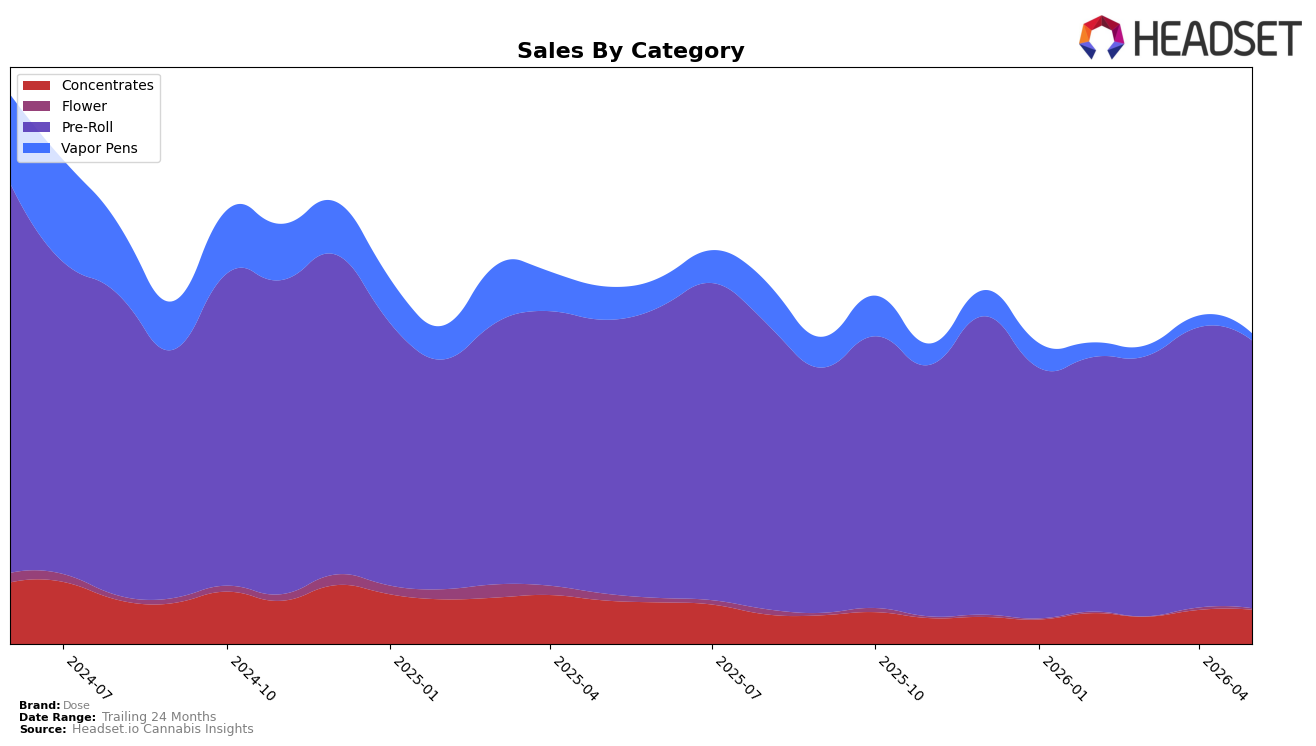

In May 2026, Dose concentrated 83.98% of sales in Pre-Roll with a year-over-year decline of 2.13% and a month-over-month drop of 4.39%, while Concentrates held 11.63% share with a 19.99% YoY decline but a 0.57% MoM uptick. Vapor Pens contracted to 3.07% share with a 72.64% YoY decrease and a 31.58% MoM pullback, and Flower sat at 1.32% share with a 55.93% YoY and 17.67% MoM decline. Average price fell 8.00% YoY to $7.85, and within Pre-Roll the average price was $7.46, indicating pricing pressure alongside category retrenchment. The pattern implies Dose is consolidating around value-leaning Pre-Rolls in Washington while higher-ticket categories like Vapor Pens and Flower recede, setting a trajectory where small gains in Concentrates must offset broad mix contraction.

Positioning-wise, a 27th rank in Pre-Roll in Washington places Dose mid-pack, and the 4.39% MoM decline in its core category alongside an 8.00% YoY average price decrease signals price-led defense rather than distribution expansion. With brand sales down 12.72% YoY and 43.46% over 24 months, and Vapor Pens shedding 31.58% MoM while Concentrates grew 0.57% MoM, the mix shift implies reliance on Pre-Roll volume elasticity and selective Concentrates stability rather than premium diversification. This points to a positioning anchored in affordable Pre-Rolls with limited cross-category pull, where incremental share recovery likely depends on improving Pre-Roll velocity more than reviving smaller, faster-declining formats.

Competitive Landscape

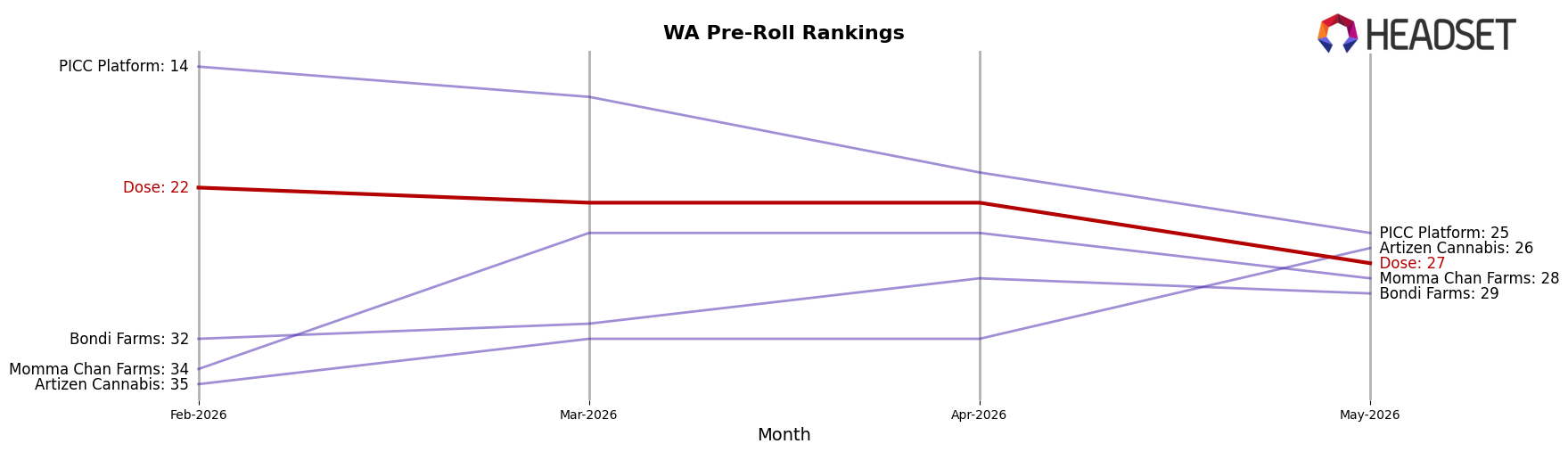

Dose sits at rank #27 in WA Pre-Roll for May 2026, unchanged year over year from rank #27, while sliding 5 positions from #22 three months ago and remaining 7 spots off its peak of #20 from May 2024; in contrast, Ooowee improved from #2 to #1 with a 55.2% YoY sales increase and Phat Panda moved down from #1 to #2 with a 3.7% YoY sales decline, indicating competitor momentum is concentrated at the top as Dose’s mid-pack rank stability masks recent quarter-on-quarter slippage, implying the brand is ceding relative position without immediate YoY deterioration.

Notable Products

Sour Diesel Infused Pre-Roll (1g) delivered the headline move in May 2026 with a +105.1% month-over-month jump to rank 2, while Sour Pebbles Infused Palm Blunt (1g) slipped -10.6% at rank 9, indicating volatility clustered at the edges of the leaderboard. Blueberry Muffins Infused Pre-Roll (1g) held rank 1 with an 11.0% gain, and Northern Light Infused Pre-Roll (1g) was effectively flat at rank 3 with a 0.0% change, concentrating momentum in just one breakout SKU rather than a broad lift. Eight of the top ten SKUs are Pre-Roll variants, suggesting category concentration that favors flavor-led infused formats over form-factor experiments; this mix points to Dose prioritizing depth in infused Pre-Rolls, using a few high-velocity flavors to pull the portfolio rather than spreading bets across new subtypes.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.