Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

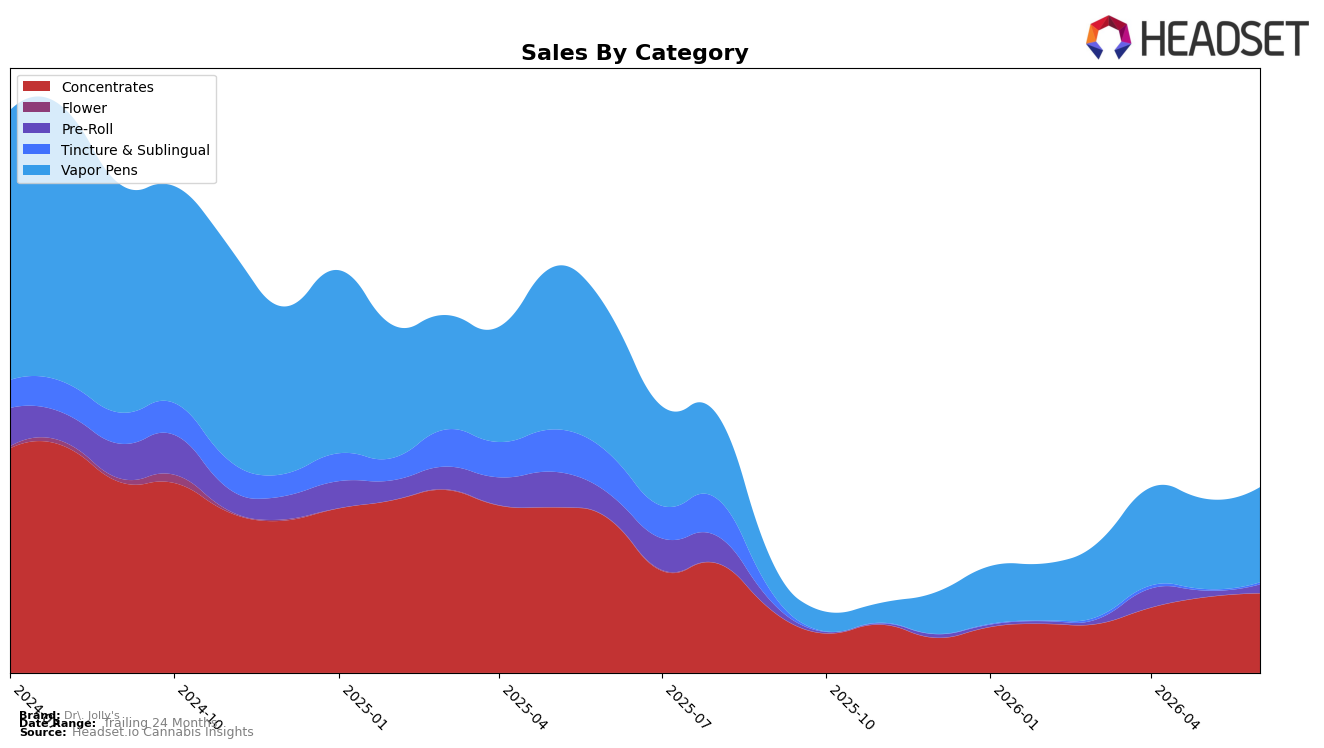

In June 2026, Dr. Jolly's leaned heavily on Vapor Pens at 51.46% share while Concentrates held 42.94%, yet the two pillars moved in different ways: Vapor Pens declined 33.11% year over year but rose 5.39% month over month, whereas Concentrates fell 48.57% year over year with a 5.34% month-over-month lift. Smaller lines showed sharper volatility, with Pre-Roll down 65.67% year over year but up 33.62% month over month, and Tincture & Sublingual down 95.45% year over year yet up 39.92% month over month. Coupled with a 31.52% year-over-year drop in average price and a 48.89% brand-level sales decline, the mix implies the brand is leaning on price-adjusted recovery in its two core categories while using tactical, low-base rebounds in Pre-Roll and Tincture & Sublingual to absorb seasonality without materially shifting the portfolio’s center of gravity.

The category shifts position Dr. Jolly's as a value-tilted Vapor Pen and Concentrates player in Oregon, where a 36th-place Vapor Pens rank and a 31.52% price compression signal a trade-down environment that favors accessible price tiers over premium depth. With Vapor Pens gaining 5.39% month over month and Concentrates up 5.34% month over month while holding a combined 94.40% share, the brand’s path to stabilization likely hinges on defending mid-pack visibility in Vapor Pens and using concentrated promos to convert month-over-month upticks into repeat velocity, rather than overextending into Pre-Roll or Tincture & Sublingual where outsized month-over-month swings ride on sub-5% share and risk diluting focus.

Competitive Landscape

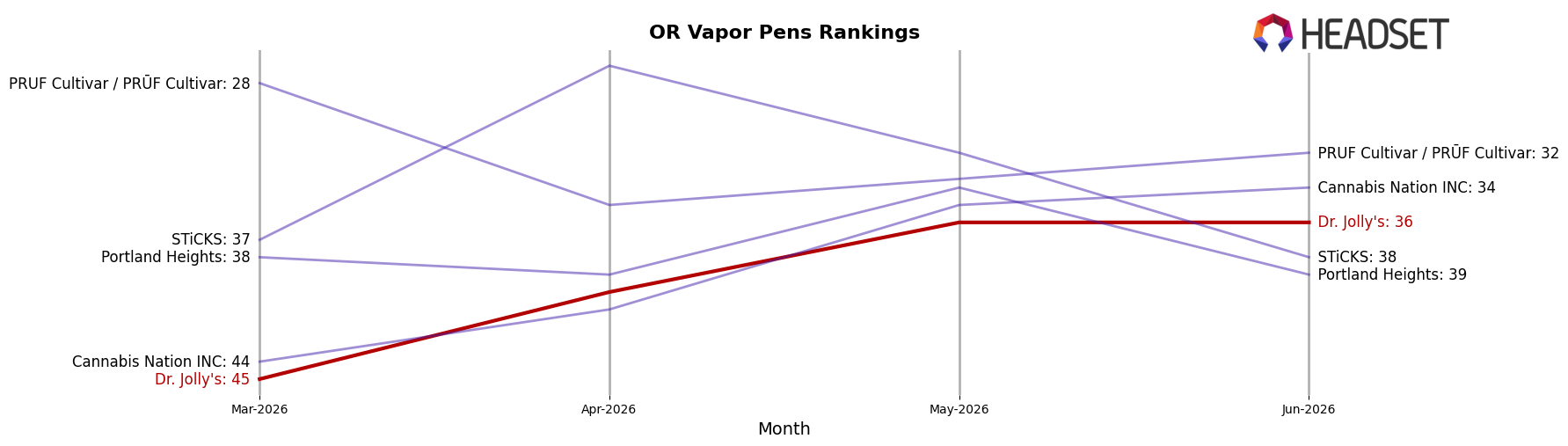

Dr. Jolly's sits at rank #36 in OR Vapor Pens in June 2026, down 5 positions year over year from #31, yet up 9 spots from March 2026’s #45, while its peak of #20 in July 2024 underscores how far the brand has slipped in rank; by contrast, Buddies advanced from #2 to #1 with 16.9% year-over-year sales growth and FRESHY climbed from #5 to #2 on 81.5% growth, whereas Entourage Cannabis / CBDiscovery fell from #1 to #3 amid a 38.9% decline—this divergence implies Dr. Jolly's recent quarter-on-quarter recovery has not translated into category share capture, and the current trajectory points to stabilization rather than a return to top-20 competitiveness without a catalyst.

Notable Products

Columbian Kush Live Resin (1g) delivered the standout move in June 2026 with a 120.7% month-over-month gain and a rise into rank 5, while Turquoise Living Wax (1g) advanced 71.9% to hold rank 1. Sour Fantasy Nug Run Wax (1g) climbed 73.4% to rank 2, and Papaya Breeze Live Resin (1g) and Shady Apples Live Resin (1g) each exceeded 55% growth as the category concentrated with eight of the top ten SKUs in Concentrates. With rank positions 1 through 8 dominated by Concentrates and only one Pre-Roll entering at rank 9 despite a 22.7% lift and $3,200 in sales, the mix points to Dr. Jolly's leaning further into extract-led velocity and depth rather than breadth across form factors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.