Market Insights Snapshot

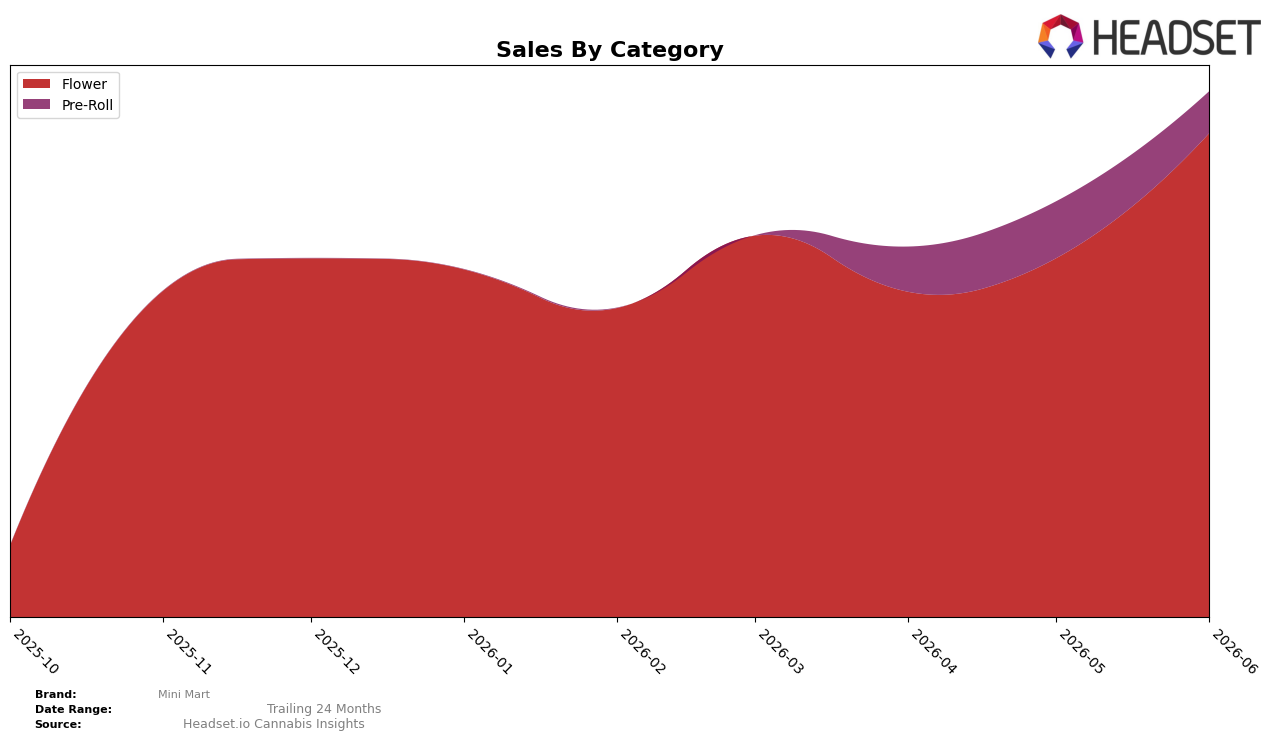

Mini Mart concentrated 92.09% of June 2026 sales in Flower while Pre-Roll accounted for 7.91%, with Flower up 34.88% month over month and Pre-Roll down 26.50% month over month. Within Flower, the brand held rank 12 in New York, and the category’s average price of $23.46 sat above the brand-level average price of $23.10, implying a mix tilt toward higher-priced Flower even as Pre-Roll’s $19.61 average price could not offset share loss; the pattern implies Mini Mart is leaning into higher-velocity Flower while deprioritizing Pre-Roll.

The shift toward a 34.88% month-over-month lift in Flower alongside a 26.50% month-over-month contraction in Pre-Roll raises category concentration risk as share consolidates at 92.09% in a single category and limits cross-category traffic from value-oriented Pre-Roll at 7.91% share. Holding rank 12 in New York Flower with a category price of $23.46 versus a $23.10 brand average suggests the brand’s pricing power is anchored in Flower rather than in Pre-Roll, implying positioning as a Flower-first player where incremental gains will likely come from assortment depth and price-pack architecture in Flower rather than breadth expansion.

Competitive Landscape

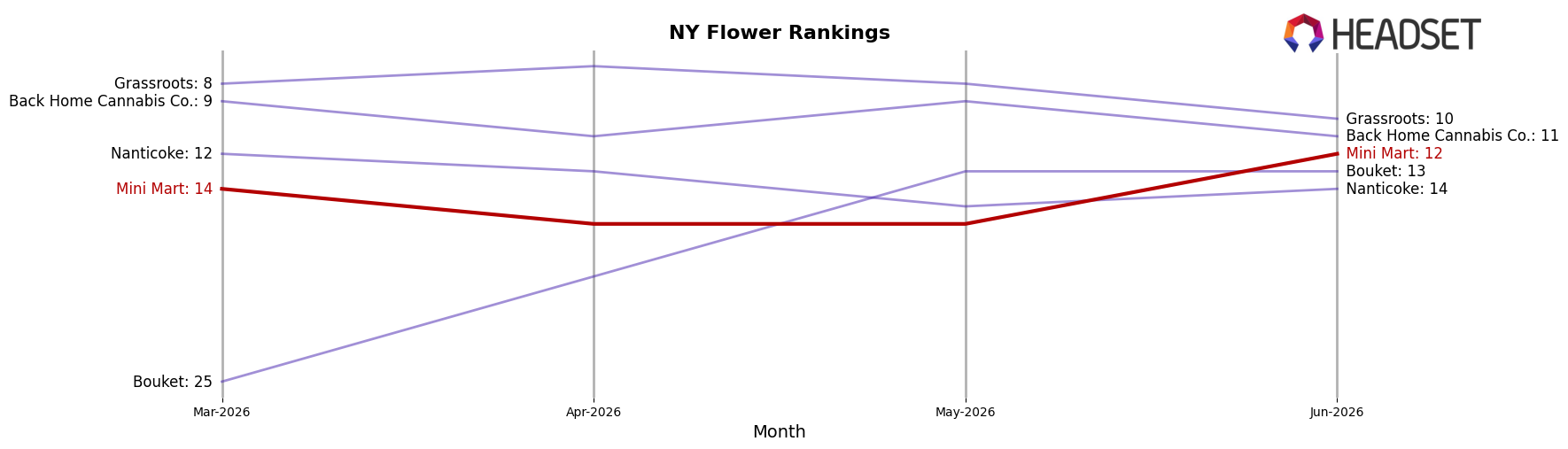

Mini Mart is currently ranked #12 in NY Flower in June 2026, up 2 positions from #14 in March 2026, while hitting a peak rank of #12 in June 2026; in contrast, Find. sits at #1 after a year-over-year climb of 3 spots with sales up 35.6%, and RYTHM advanced to #5 with a 10-rank YoY gain and 40.6% sales growth. Meanwhile, Dank. By Definition holds #3 despite a 1-rank YoY dip and a 50.7% sales decline, and Rolling Green Cannabis is #4 with a 2-rank YoY improvement but a 7.1% sales contraction; against this backdrop, Mini Mart’s 2-rank quarter-over-quarter rise into its best-ever #12 suggests a move from peripheral to contestable mid-tier positioning if it can convert incremental rank gains into sustained share capture.

Notable Products

Blue Dream (3.5g) posted the largest movement in June 2026 with a +52.0% month-over-month surge while holding rank 1, and Double Dream (3.5g) climbed +46.6% to remain in the top 10 at rank 10; nine of the top ten are Flower SKUs, concentrating the mix in a single category. Banana Bread (3.5g) sat at rank 2 with $139,956 in sales and no reported month-over-month rate, and Jack Herer (3.5g) held rank 3 with no month-over-month figure provided, indicating stability at the top while growth is concentrated at the category’s edges. The pattern implies Mini Mart is leaning into a Flower-led strategy where a single breakout like Blue Dream drives share gains, suggesting portfolio risk unless additional SKUs add diversified momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.