Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Eleven is stocked at 137 licensed dispensaries across Massachusetts and Pennsylvania, 78 of them in Massachusetts, with the deepest coverage in Boston, Springfield, Fall River, Worcester, and Brockton. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

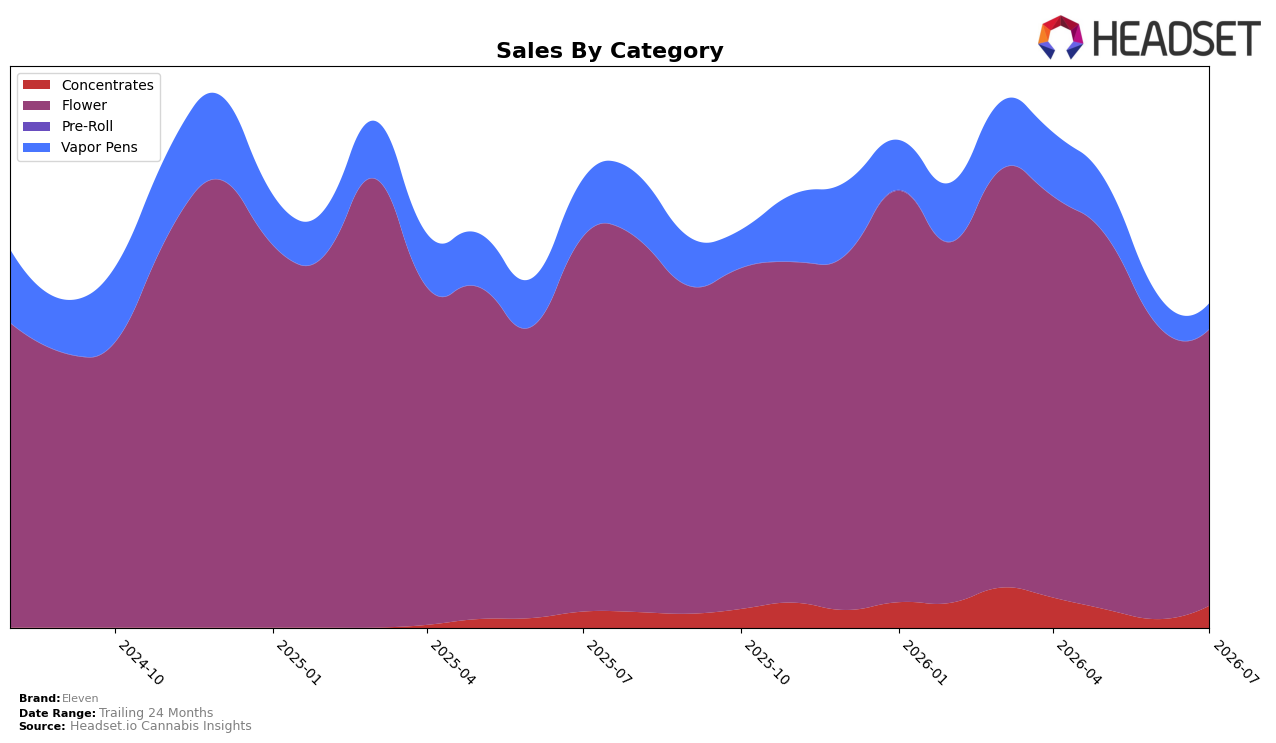

In July 2026, Eleven concentrated 85.31% of sales in Flower, where sales fell 26.36% year over year and 5.76% month over month, while Vapor Pens at 7.90% share declined 55.30% YoY and 14.99% MoM; in contrast, Concentrates at 6.80% share rose 36.89% YoY and surged 158.50% MoM. Average price rose 4.17% YoY to $29.20, with Flower averaging $31.02 and Vapor Pens at $21.76, indicating mix pressure despite price firmness. With Massachusetts anchored performance in Flower ranked 22nd, the pattern implies Eleven is over-indexed in a contracting core while a small but accelerating Concentrates line is the only near-term offset.

The mix shift implies a defensive posture: heavy reliance on Flower exposes Eleven to further share loss if the category slide continues, given a 26.36% YoY drop paired with a 5.76% MoM decline, while Vapor Pens’ 55.30% YoY contraction and 14.99% MoM slide limit cross-category cushioning. The outsized 158.50% MoM rebound in Concentrates off a 6.80% share base, alongside a 36.89% YoY gain, suggests an entry point to rebalance, but current scale means it cannot counteract an 85.31% Flower weight yet; the implication is to accelerate Concentrates penetration and price-pack architecture to stabilize rank 22 positioning in Flower without deepening exposure to its decline trajectory.

Competitive Landscape

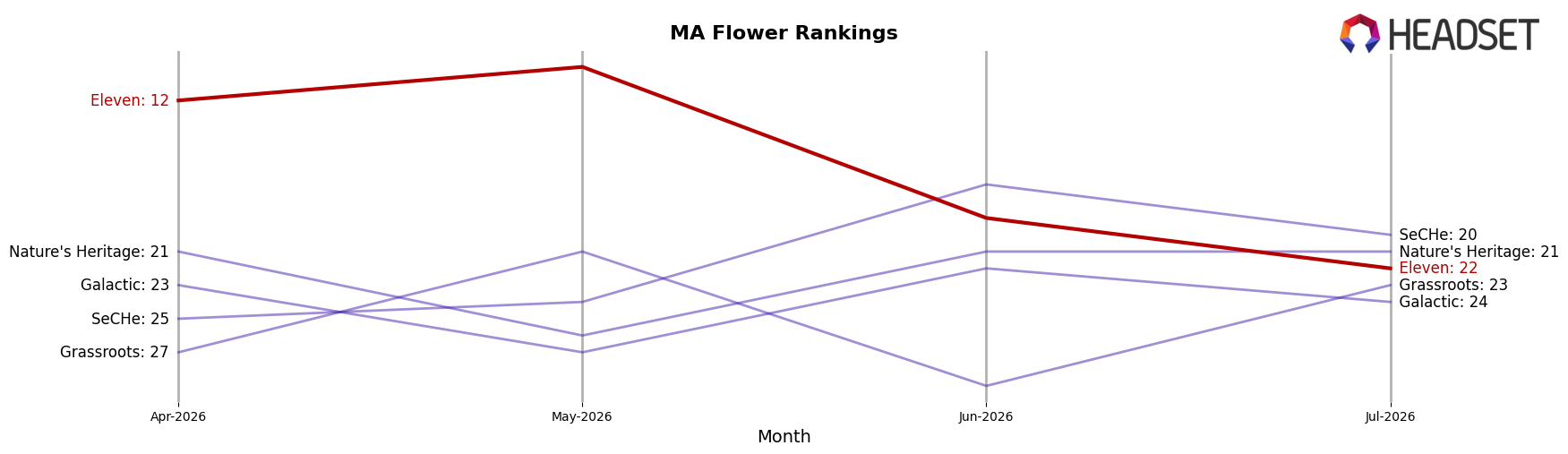

Eleven sits at rank #22 in Massachusetts Flower for July 2026, down 7 positions year over year from #15, after a 10-position slide from #12 three months ago; this contrasts with Farmer's Cut rising to #1 from #4 and posting 56.7% year-over-year sales growth, while Root & Bloom advanced to #5 from #10 with 118.9% sales growth. Against leaders holding ranks #1–#5, Eleven’s current #22 is 15 positions below its peak of #7 in March 2025 and 20 positions behind Perpetual Harvest at #3, signaling that share is consolidating among faster-rising competitors and that Eleven’s rank trajectory implies continued pressure unless mix or distribution shifts reverse the multi-quarter slippage.

Notable Products

Blue Runtz (7g) posted the steepest movement in July 2026 with a -39.3% month-over-month decline while holding rank 4, contrasting with Animal Mints (7g) at rank 1 and OGKB 2.1 (7g) at rank 2. Four of the top ten are Flower SKUs concentrated in ranks 1 through 5, with Crunch Berries (7g) tied at rank 3 and Cranberry Z (7g) also at rank 3, indicating category dominance ahead of Vapor Pens at ranks 6 and 9. The Gold Dahlia Distillate Cartridge (1g) reached rank 6 with $13,408 in July 2026 as Frozen Paloma Distillate Cartridge (1g) sat at rank 9, suggesting Vapor Pens remain secondary to Flower by rank position and share of top-tier spots. The pattern implies Eleven is leaning into larger-pack Flower as the commercial anchor while Vapor Pens act as complementary volume, with the Blue Runtz (7g) drop pointing to SKU-level volatility that may require price or distribution adjustments.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.