Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

EZ Vape is stocked at 117 licensed dispensaries across Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Bellevue, and Bellingham. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

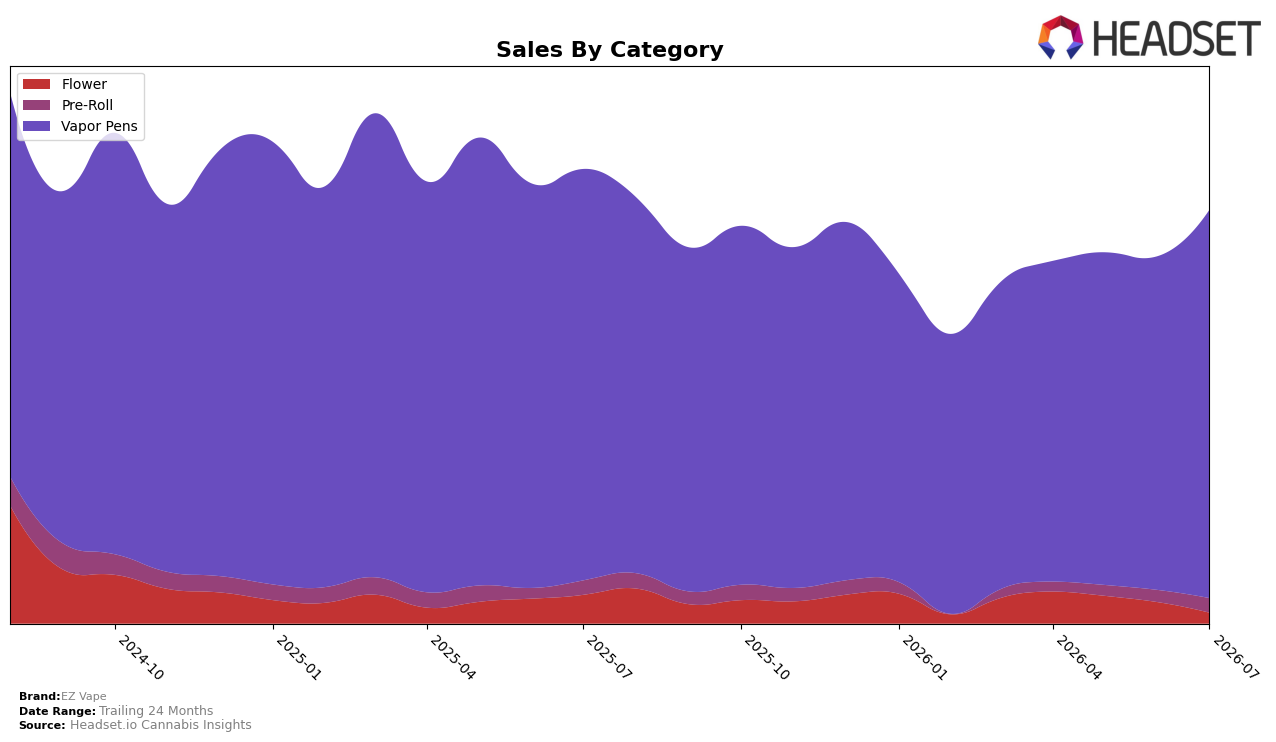

EZ Vape concentrated 91.94% of July 2026 sales in Vapor Pens while Pre-Roll held 4.45% and Flower 3.61%, indicating a category skew that tightened as Vapor Pens rose 16.07% month over month despite a 5.57% year-over-year decline. Pre-Roll advanced 14.49% month over month alongside a 0.86% year-over-year increase, whereas Flower contracted 40.55% month over month and 53.65% year over year, with the latter’s retreat helping lift overall mix toward Vapor Pens even as brand-level sales fell 8.73% year over year. With an average price down 0.38% year over year and Vapor Pens priced at $14.31, the mix shift suggests EZ Vape is leaning into higher-velocity pen units to offset Flower’s pullback, which implies near-term stability is tied to sustaining month-over-month pen demand rather than recovering legacy Flower volume in Washington.

In Vapor Pens, EZ Vape sits at rank 12 in Washington, and the 16.07% month-over-month lift alongside a 5.57% year-over-year decline implies transactional momentum is recent rather than structural, especially as the brand’s total sales declined 8.73% year over year while 24-month sales are down 17.52%. Pre-Roll’s 14.49% month-over-month growth on a 4.45% share and Flower’s 40.55% month-over-month contraction on a 3.61% share point to a barbell: reliance on a single lead category for volume and a shrinking long-tail that reduces basket diversity. The pattern implies EZ Vape’s positioning is increasingly defined by pen-led penetration at mid-teen price points, and that maintaining or improving the rank 12 footing will depend on converting July 2026’s month-over-month pen gains into sustained multi-month share capture while capping further erosion in Flower to avoid overconcentration risk.

Competitive Landscape

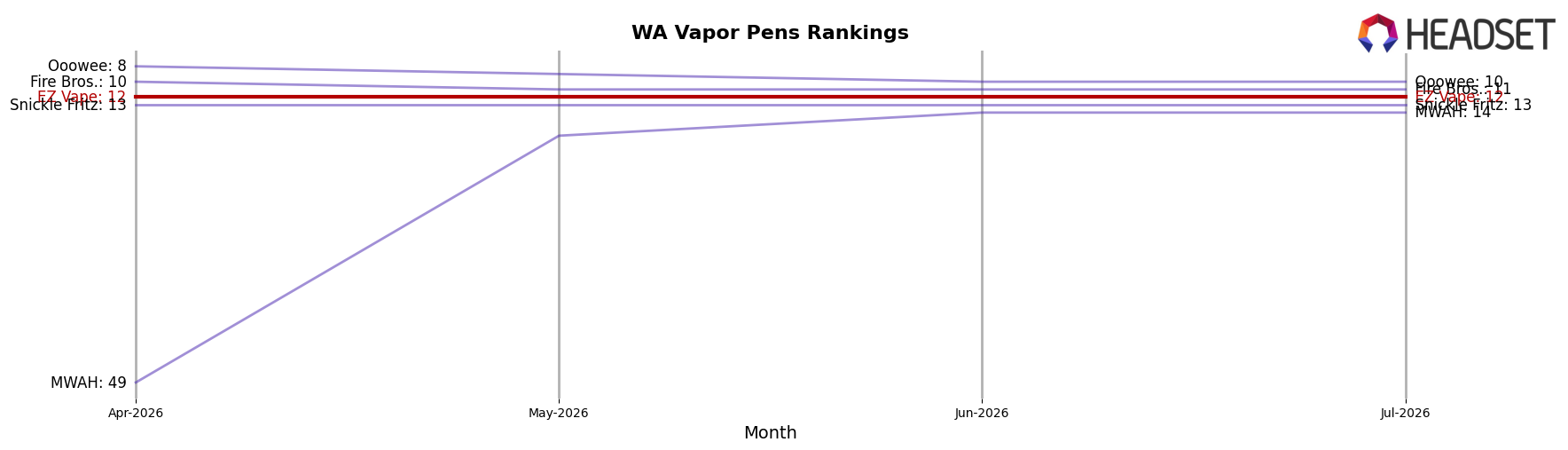

EZ Vape sits at rank #12 in WA Vapor Pens in July 2026, sliding 3 spots year over year from #9 while holding flat versus April 2026 at #12, indicating a loss of relative position despite short-term stability. Against that backdrop, Crystal Clear moved up from #2 to #1 with a 12.6% YoY sales increase, while Mfused fell from #1 to #2 amid a 26.1% YoY sales decline, and Full Spec climbed from #6 to #3 with 12.9% YoY growth, pointing to a shake-up concentrated at the top ranks. EZ Vape’s current #12, compared with a peak of #7 in May 2025 and a 3-rank YoY drop, implies a drift toward the category’s middle tier as faster-moving leaders expand share and underperformers cede ground above it.

Notable Products

Skywalker OG Cured Resin Disposable (1g) posted the standout move in July 2026 with a 77.7% month-over-month surge to rank 1, outpacing the next-best MoM climbers like Zkittlez Distillate Disposable (1g) at 36.1% in rank 7 and Huckleberry Distillate Disposable (1g) at 28.1% in rank 8. Lemon Cake Cured Resin Disposable (1g) rose 12.8% to rank 2 while Do-Si-Dos Distillate Disposable (1g) gained 13.2% to rank 3, and Trainwreck Distillate Cartridge (1g) advanced 24.9% at rank 9. Eight of the top ten are Vapor Pens, with only one Pre-Roll entrant at rank 6 and no SKUs showing double-digit decline, indicating a consolidated tilt toward inhalable oil formats. The pattern implies EZ Vape is concentrating variety and momentum in Vapor Pens while resin-led SKUs at the top signal a shift from distillate-only reliance toward higher-terp appeal that can support premium pricing.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.