Where to Buy

Farmaceutical Rx (Frx) is stocked at 90 licensed dispensaries across Ohio and Pennsylvania, 53 of them in Ohio, with the deepest coverage in Cincinnati, Columbus, Cleveland, Oxford, and Athens. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

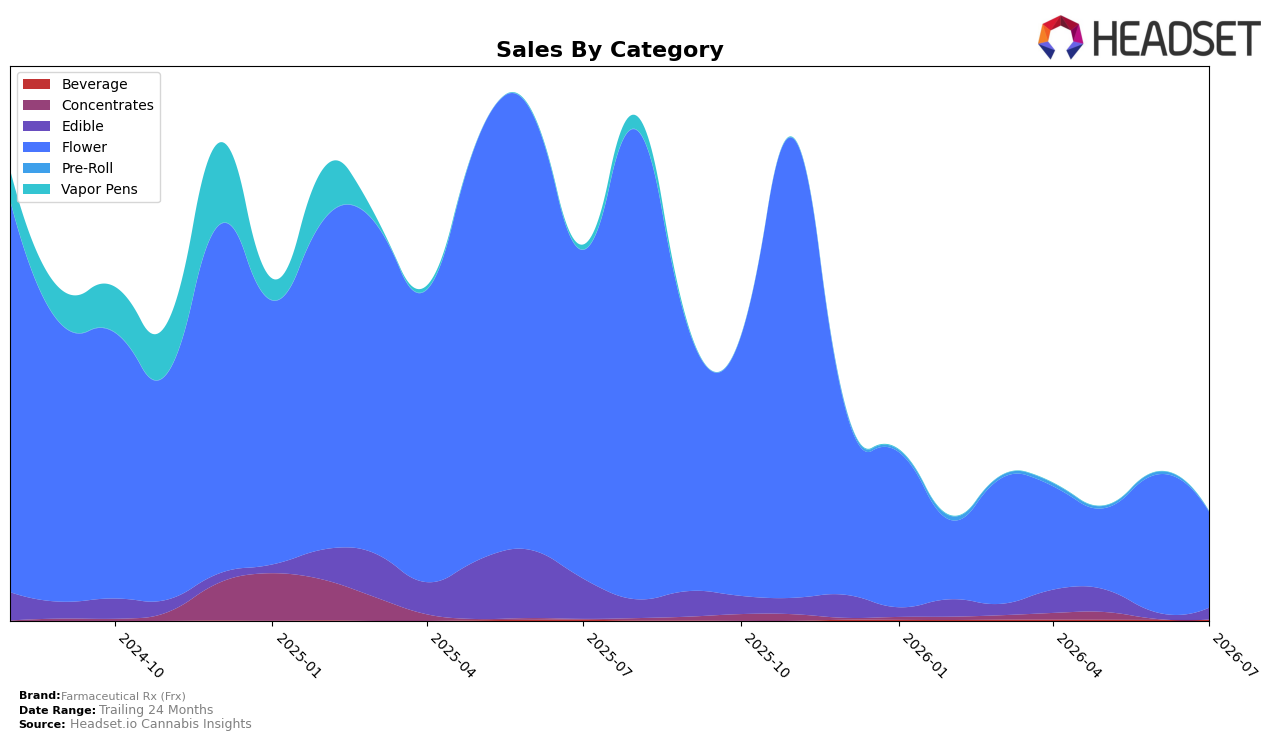

Farmaceutical Rx (Frx) concentrated 88.56% of July 2026 revenue in Flower, where sales fell 70.88% year over year and 30.65% month over month, while Edible expanded to a 10.50% share on a 90.45% month-over-month surge despite a 71.66% year-over-year decline; Beverage remained marginal at 0.94% share with a 15.57% year-over-year drop and a 2.66% month-over-month slip. With the brand’s average price down 11.89% year over year to $31.49 and Flower ranked 50th in Ohio, the mix shift signals reliance on a shrinking Flower base alongside opportunistic Edible rebounds that are too small to offset category concentration.

The combination of a 30.65% month-over-month contraction in Flower and a 90.45% month-over-month jump in Edible implies the brand is repositioning toward value-seeking consumers via lower price points in core Flower and selective trial in Edibles, yet the 71.16% brand-level year-over-year sales decline and a 50 rank in Ohio indicate insufficient scale to change share trajectory. The pattern suggests Farmaceutical Rx (Frx) must either diversify beyond an 88.56% Flower dependency or tighten Flower assortment, because a 10.50% Edible share and a 0.94% Beverage foothold are not large enough to counter multi-quarter declines of 70.88% in Flower and 71.66% in Edibles.

Competitive Landscape

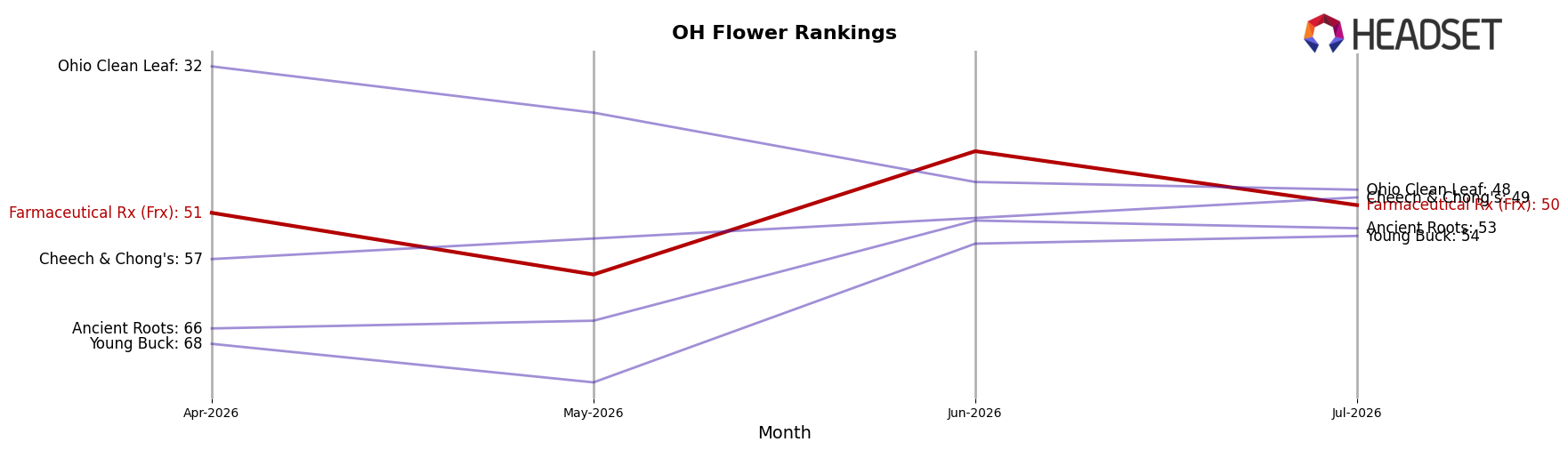

Farmaceutical Rx (Frx) sits at rank #50 in July 2026, down 24 positions year over year from #26, while slipping 1 spot from April 2026’s #51 to July 2026’s #50; this contrasts with RYTHM advancing from #6 to #1 and Klutch Cannabis jumping from #21 to #3 alongside a 403.0% YoY sales gain. The brand’s trajectory also diverges from Certified (Certified Cultivators), which climbed from #14 to #5 with a 92.8% YoY increase, and from Riviera Creek, which held near the top at #2 despite a -16.0% YoY sales change; Farmaceutical Rx (Frx) is far below its peak #13 in July 2024, indicating that without a reversal in relative velocity versus rising leaders, the brand is settling into a lower-tier position.

Notable Products

Spicy Slap (2.83g) posted the largest month-over-month jump at +75.3% and climbed to rank 3, while GMO Minis (5.66g) fell -53.3% yet still held rank 1, indicating volatility concentrated at the very top of the lineup. Animal Face (2.83g) declined -40.5% and slid to rank 10, contrasting with Spicy Slap’s surge and suggesting share is rotating within Flower rather than expanding overall. Eight of the top ten are Flower SKUs, with multiple Minis and Smalls formats in the top seven, pointing to consumer trade-down or value-seeking even as one core eighth gains momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.