Where to Buy

The Solid is stocked at 122 licensed dispensaries across Ohio, Missouri, and Utah, 61 of them in Ohio, with the deepest coverage in Columbus, Cincinnati, Akron, Athens, and Lorain. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

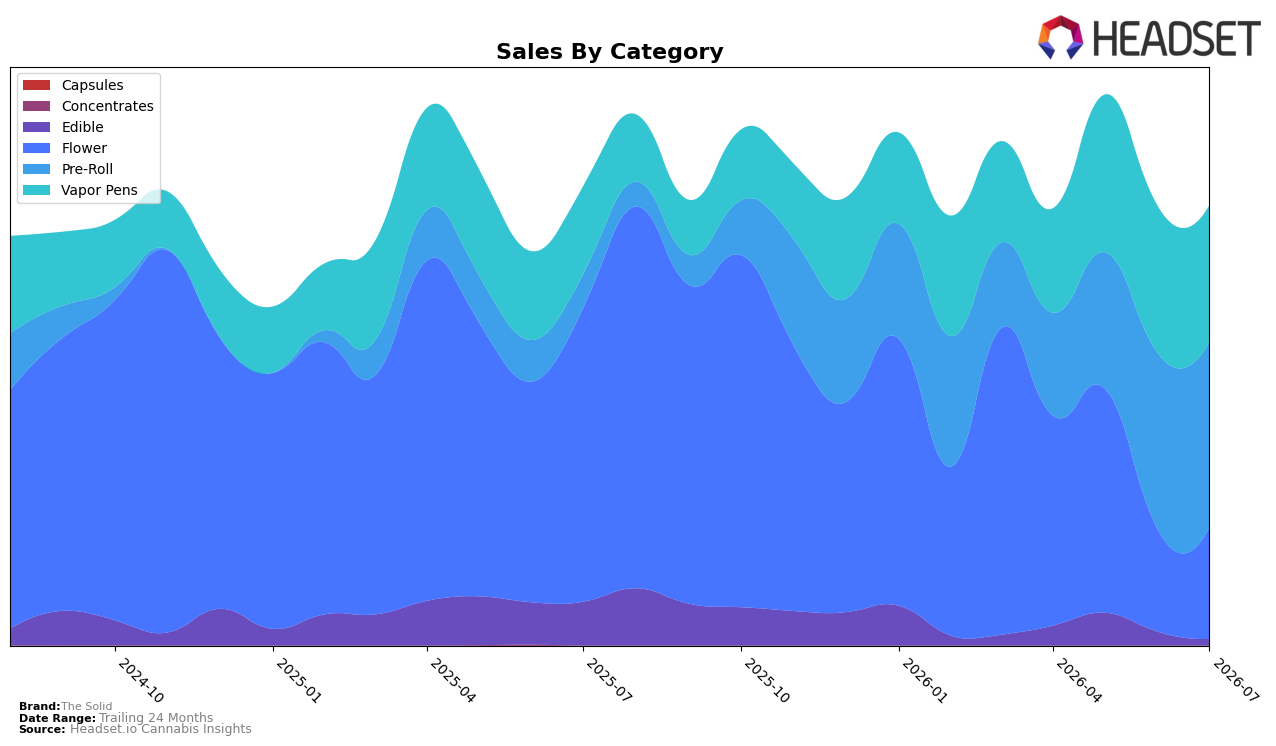

In July 2026, The Solid’s category mix pivoted toward Pre-Roll, which held 42.12% share with year-over-year growth of 452.79% and month-over-month growth of 4.98%, while Vapor Pens at 31.06% share grew 55.50% YoY but declined 6.98% MoM; Flower at 25.39% share fell 62.01% YoY yet rose 9.81% MoM, and Edible contracted to 1.44% share with an 85.50% YoY decline and a 53.08% MoM drop. Despite overall brand sales down 4.14% YoY and average price down 39.59% YoY to $15.80, the Pre-Roll surge and Vapor Pens pullback suggest a reallocation toward lower-priced, higher-velocity formats, implying a deliberate shift to volume-driven mix that offsets category contractions elsewhere.

The concentration in Pre-Roll, paired with a 6th-place rank in Pre-Roll in Ohio and opposite movements in Vapor Pens (-6.98% MoM) and Flower (+9.81% MoM), indicates a positioning anchored in accessible entry points while using Flower as an upsell corridor when price elasticity allows. With Pre-Roll up 452.79% YoY and Edible down 85.50% YoY, the mix favors categories where price compression can convert to share, implying that The Solid is competing on basket frequency and trial rather than premium ticket, with Pre-Roll acting as the acquisition engine and Vapor Pens and Flower serving as retention and trade-up paths as monthly swings normalize.

Competitive Landscape

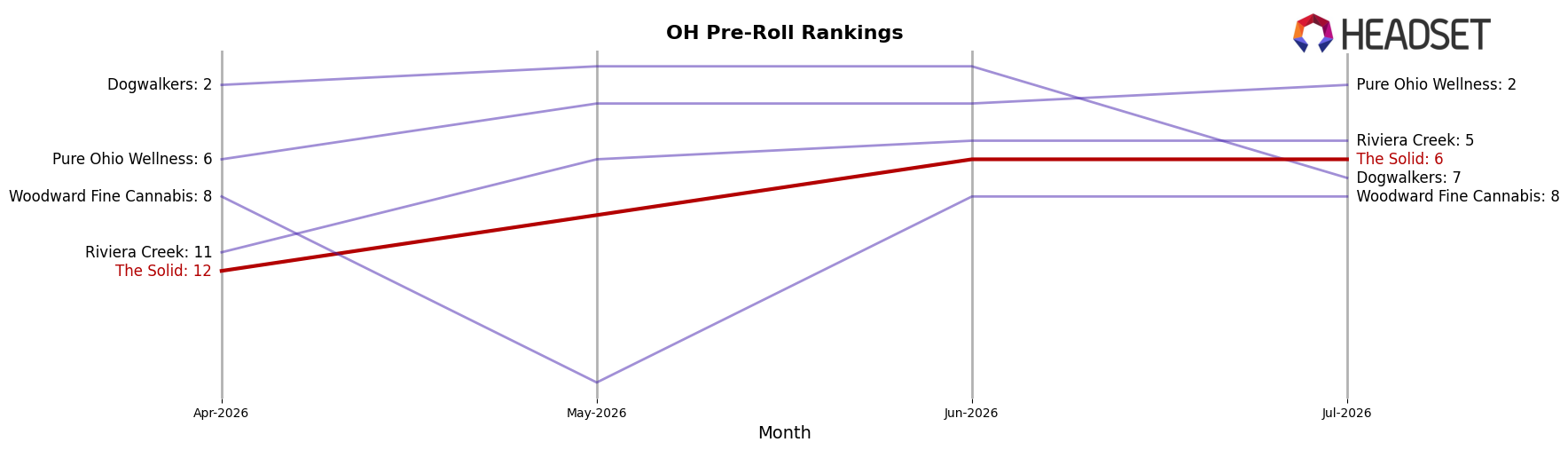

Ranked #6 in July 2026 with no year-over-year rank reported, The Solid climbed 6 positions since April 2026 when it sat at #12, reaching a new peak rank of #6 in July 2026. Against the competitive set, Buckeye Relief holds #1 while Riviera Creek sits at #5 after a +1 YoY rank change and a 996.1% YoY sales increase, indicating The Solid’s 6-place quarter-over-quarter rise still trails the velocity of a rapidly advancing rival. The pattern implies momentum concentrated in the last quarter rather than sustained annual gains, suggesting The Solid’s rank trajectory depends on converting its 6-rank three-month surge into durable share that can close the 1-position gap to the top five.

Notable Products

Cruise Control Infused Pre-Roll (1g) posted the steepest move in July 2026 with a -52.0% month-over-month decline while sliding to rank 6, contrasting with Good Vibes Only Infused Pre-Roll (1g) at rank 2 on +27.1% MoM and Midnight Melt Infused Pre-Roll (1g) at rank 1 with $73,131 in sales. Mind Fiesta Pre-Roll (1g) also contracted by -27.7% MoM at rank 8, and four of the top ten are Pre-Roll SKUs that cluster between ranks 1 and 9, indicating concentration risk alongside uneven velocity shifts. The juxtaposition of a double-digit gain at rank 2 and two double-digit declines at ranks 6 and 8 implies a portfolio pivot is needed to reinforce proven Pre-Roll winners while pruning or repositioning laggards.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.