Market Insights Snapshot

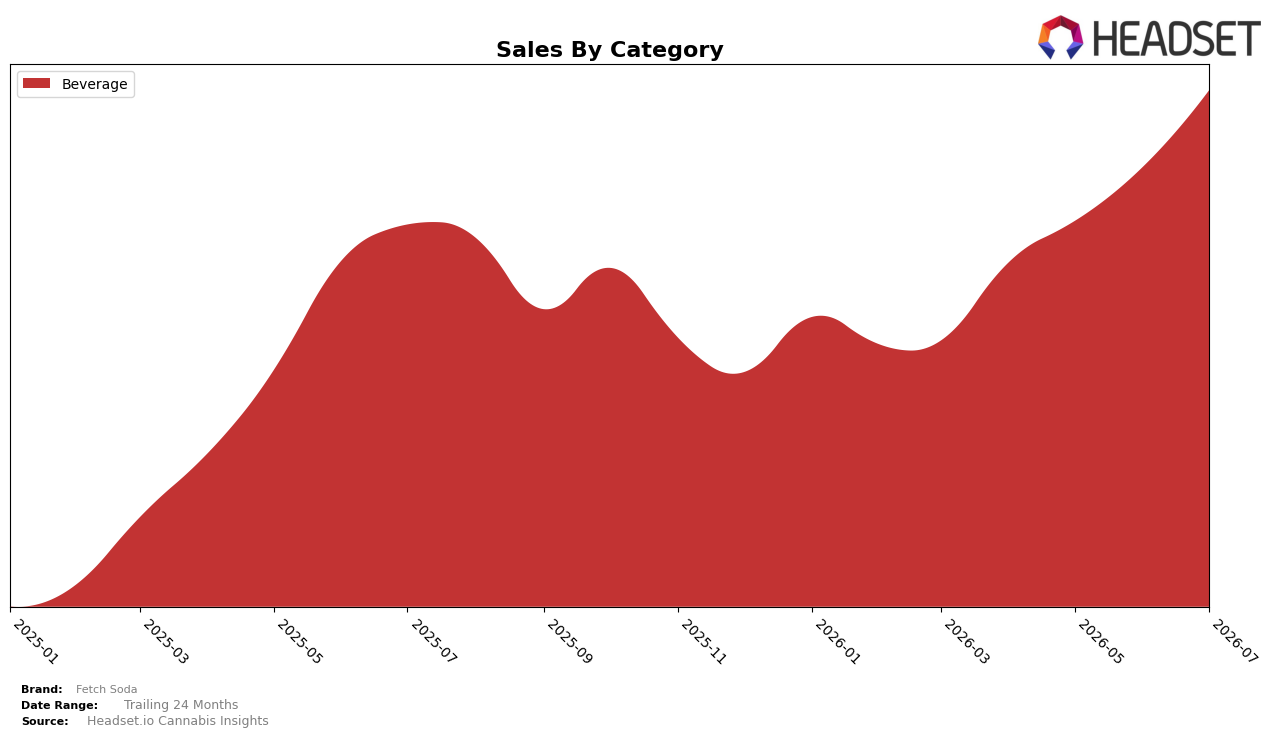

In July 2026, Fetch Soda operated as a single-category brand with Beverage at 100.0% of mix, pairing 35.07% year-over-year sales growth with a 17.30% month-over-month gain. Average price rose 2.88% YoY to $6.58, while rank in Beverage within Alberta sat at 14, indicating volume expansion outpacing pricing. The pattern implies demand is concentrated and scalable within Beverage, where incremental volume growth and a modest price lift are moving the brand up the consideration set without price-driven drag.

The concentration in Beverage at 100.0% alongside a 17.30% MoM surge and a 35.07% YoY uplift suggests Fetch Soda is winning on repeat and distribution rather than breadth, positioning it as a depth-first player in its core aisle. With rank at 14 in Alberta and price only 2.88% higher YoY, the brand’s competitive posture hinges on scaling facings and pack mix to convert volume momentum into rank gains, implying priority on velocity levers over category expansion in the near term.

Competitive Landscape

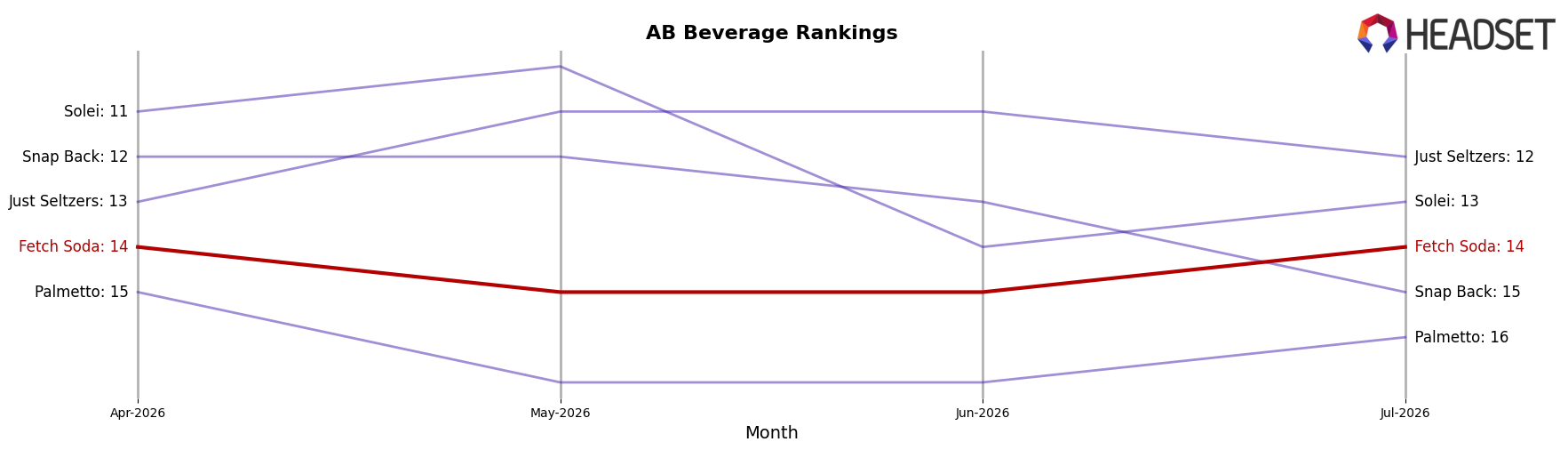

Fetch Soda is #14 in AB Beverage in July 2026, up 7 ranks from #21 year over year, with its peak rank of #14 matching its current position and no movement from April 2026 to July 2026 on the 3‑month view; meanwhile, Mary Jones climbed from #6 to #2 with 198.23% YoY sales growth and Sweet Justice slipped from #2 to #5 with -27.59% YoY sales change, indicating Fetch Soda’s YoY ascent is occurring alongside both accelerating and contracting leaders, which implies the brand is stabilizing at mid‑tier with upside dependent on converting the recent 7‑rank YoY climb into sustained gains beyond #14.

Notable Products

Cream Soda (10mg THC, 12oz, 355ml) posted the standout move in July 2026 with a 63.37% month-over-month jump into rank 3, while Cream Soda (600mg THC, 12oz, 355ml) fell 21.62% to rank 4, marking a divergence within the same flavor family. Zero Lemon Lime Soda (10mg THC, 12oz, 355ml) held rank 1 with an 11.36% lift as Zero Classic Cola (10mg THC, 12oz, 355ml) advanced 33.34% at rank 2, and all four top-10 slots are Beverage SKUs, signaling format concentration. The mix indicates Fetch Soda is consolidating around 10mg formulations where velocity is accelerating, while higher-dosage variants are losing momentum and may warrant price, pack, or placement tests even at a current-month revenue peak of $23,256 for the leader.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.