May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

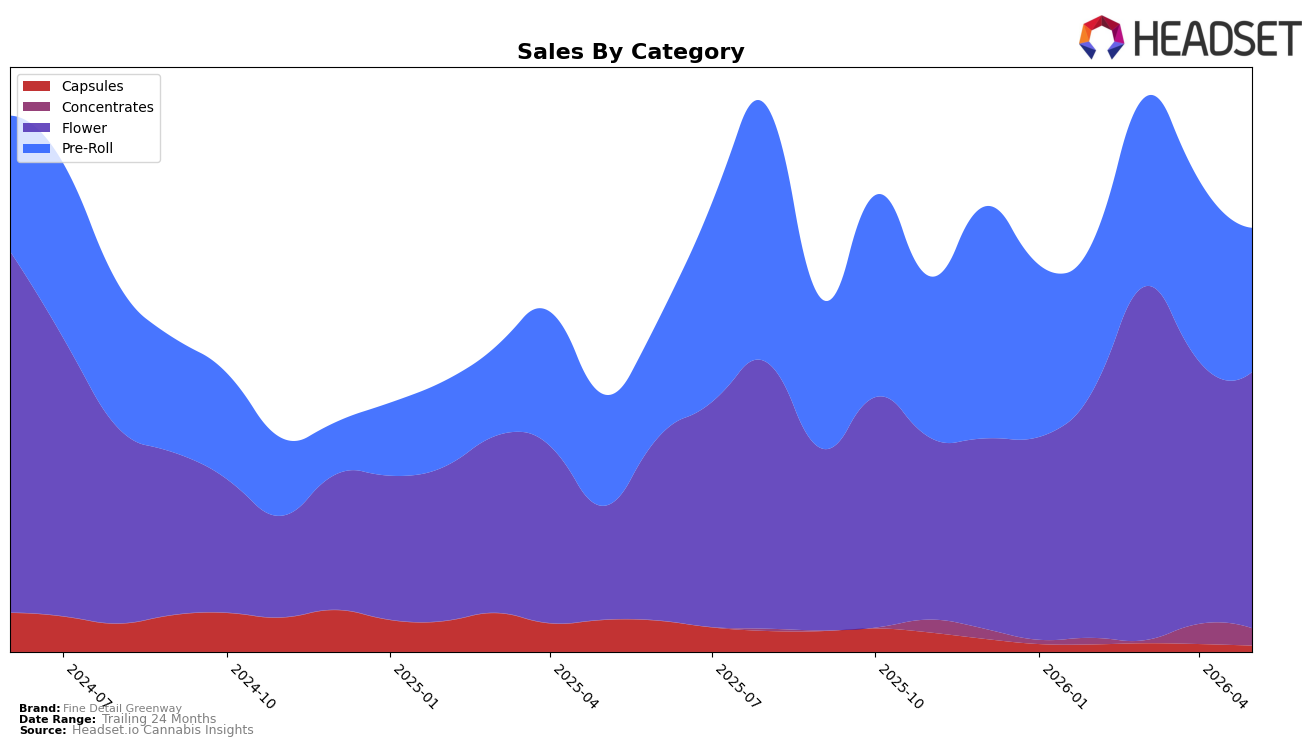

In May 2026, Fine Detail Greenway’s mix tilted toward Flower at 60.50% share, up on a 125.35% year-over-year sales increase but easing month-over-month by 2.63%; meanwhile, Pre-Roll held 34.04% share with 29.33% year-over-year growth yet fell 20.49% month-over-month. Smaller lines contracted, as Concentrates slipped 13.61% month-over-month to 4.04% share and Capsules dropped 80.96% year-over-year and 20.62% month-over-month to 1.42% share. With brand-level sales up 64.93% year-over-year against a 61.54% rise in average price and a 24.29% two-year decline, the mix shift implies consolidation around higher-priced Flower while Pre-Roll volatility weighs on near-term momentum; the pattern indicates the brand is trading into categories that support pricing while pruning lower-share segments.

The pivot toward Flower, where the average price is $18.93 and materially above the brand’s $13.23 blended average, coupled with a 125.35% year-over-year lift and only a 2.63% month-over-month dip, positions Fine Detail Greenway to lean on premium-weighted volume even as Pre-Roll’s 20.49% month-over-month decline drags mix. The sharp contractions in Capsules (down 80.96% year-over-year) and Concentrates (down 13.61% month-over-month) reduce assortment complexity and concentrate demand in two core pillars, suggesting a positioning that prioritizes price-realization and category leadership in Flower over breadth; the implication is that sustaining May 2026 growth depends on stabilizing Pre-Roll while preserving Flower’s year-over-year outperformance relative to brand-level 64.93% growth.

Competitive Landscape

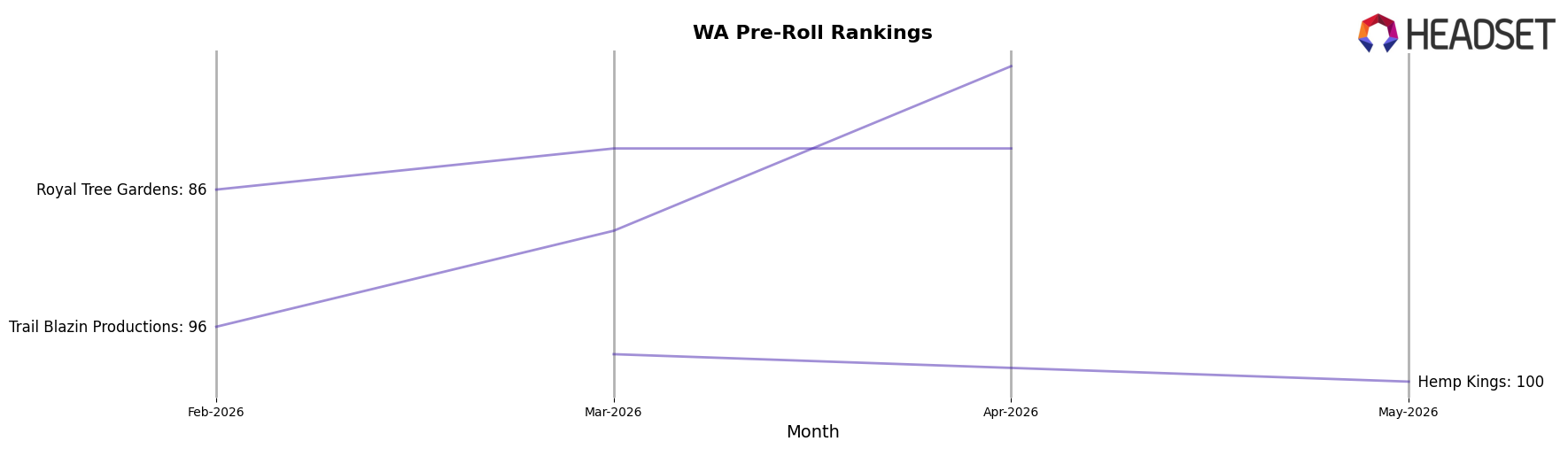

Fine Detail Greenway sits at rank #125 in WA Pre-Roll for May 2026, improving 39 positions from #164 year over year, but slipping 7 spots from #118 in February 2026 and down from a peak rank of #99 in March 2026. At the top end, Ooowee climbed from #2 to #1 with 55.2% year-over-year sales growth, while Phat Panda fell from #1 to #2 as its sales declined 3.7% year over year, indicating that leadership is reshuffling even as Fine Detail Greenway edges upward from the long tail. The pattern of a 39-rank YoY gain paired with a 26-rank gap from March 2026’s peak to today implies Fine Detail Greenway is in recovery but has not stabilized its trajectory, suggesting intermittent share capture rather than sustained momentum.

Notable Products

Satsuma Haze Pre-Roll 2-Pack (1g) posted the steepest move in May 2026 with a -58.8% month-over-month drop as the SKU fell to rank 6, while Cherry Pie OG (3.5g) slid -60.8% to rank 8, together signaling acute softness in the tail of the lineup. Blue Dream (3.5g) countered with a +48.3% month-over-month rise to rank 1 and generated $8,847, indicating that one flagship is offsetting declines rather than broad-based momentum. Six of the top ten are Pre-Roll SKUs, yet two within the top six declined more than -50% and another at rank 3 fell -27.4%, implying category weight without stability. The pattern implies Fine Detail Greenway is leaning on a single Flower leader while a concentrated Pre-Roll slate is dragging overall velocity, pointing to a need for SKU pruning and reallocation toward resilient Flower formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.