Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

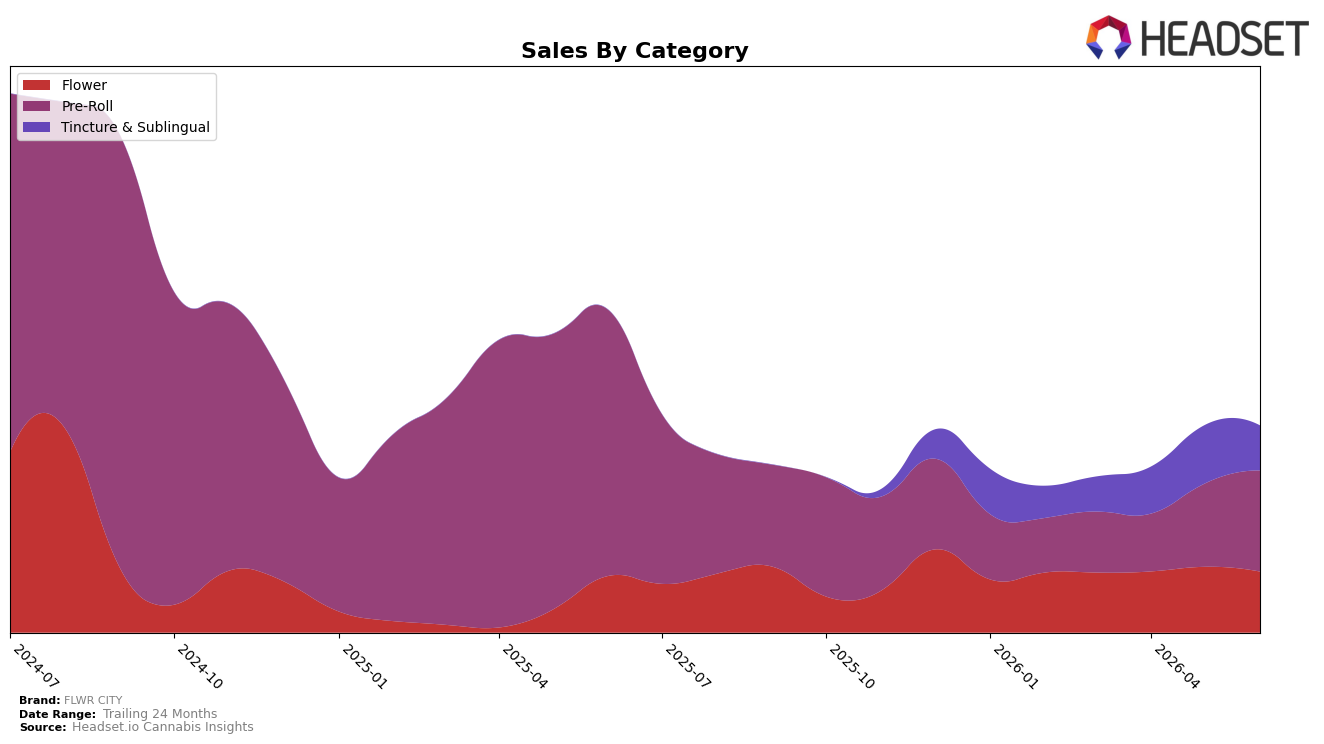

FLWR CITY’s mix in June 2026 is concentrated in Pre-Roll at 48.85% share with a 21.61% month-over-month lift, while the same category is down 62.11% year-over-year; Flower holds 29.46% share with a 7.79% year-over-year increase but a 7.27% month-over-month decline. Tincture & Sublingual accounts for 21.69% share with a 23.10% month-over-month drop and no year-over-year comp, yet the rank sits at 10 in New York, indicating niche traction despite a brand-level 36.00% year-over-year sales decline. The pattern implies a pivot toward Pre-Roll momentum on a short-cycle basis while Flower provides the only positive annual comparator, and the Tincture retreat in June 2026 risks diluting visibility in the very category where the brand holds a rank of 10.

Given a 3.06% year-over-year decrease in average price alongside a 21.61% Pre-Roll month-over-month rise and a 7.27% Flower month-over-month pullback, FLWR CITY is leaning on lower-priced, velocity-heavy formats to stabilize volumes as higher-ticket Tincture & Sublingual, with an average price of $50.56, contracts 23.10% month-over-month. With Flower up 7.79% year-over-year but Pre-Roll down 62.11% year-over-year, the brand’s medium-term positioning hinges on converting the recent Pre-Roll uptick into sustained share while defending its 10th-place standing in New York Tincture & Sublingual; the implication is that short-term mix gains are offsetting, not reversing, longer-horizon erosion, so pricing and assortment need to nudge demand toward categories with durable rank and annual growth.

Competitive Landscape

FLWR CITY sits at rank #10 in New York Tincture & Sublingual as of June 2026, edging up 1 position from #11 in March 2026 while remaining below its peak of #9 from January 2026; this places it behind Ayrloom, which held #1 both year over year and in June 2026, and behind Veterans Choice Creations (VCC), which moved up from #5 year over year to #4, indicating competitors are consolidating higher ranks as FLWR CITY hovers between #9 and #11. Compared with Head & Heal at #2 with a -16.3% sales change year over year and Mfny (Marijuana Farms New York) at #3 with a -22.8% sales change year over year, FLWR CITY’s stability at #10 alongside OMO - Open Minded Organics holding #5 with a near-flat 0.0% sales change suggests room to capture share if incumbents with negative momentum weaken; the thesis is that a modest rank recovery from #11 to #10 without reclaiming the #9 peak implies a plateau that requires a discrete trigger to break into the #8–#9 tier.

Notable Products

Top Gun (1g) posted the steepest decline in June 2026, down 79.0% MoM to rank 10, while Triangle Poison (1g) surged 121.4% MoM to rank 2, indicating a sharp redistribution of demand within Flower toward higher-velocity SKUs and away from tail items. Black Panther (1g) rose 19.7% MoM to hold rank 1 as Dogwalkers - Top Gun Pre-Roll 10-Pack (3.5g) fell 12.1% MoM to rank 6, and three of the top five ranks are Pre-Roll SKUs, signaling that Pre-Roll breadth still anchors placement even as individual Pre-Rolls soften. With two Flower SKUs in the top ten moving in opposite directions and Tincture & Sublingual entries down 16.8% and 29.0% MoM at ranks 8 and 9, the mix points to FLWR CITY leaning into a Flower-led core while trimming underperforming formats and strains.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.