Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

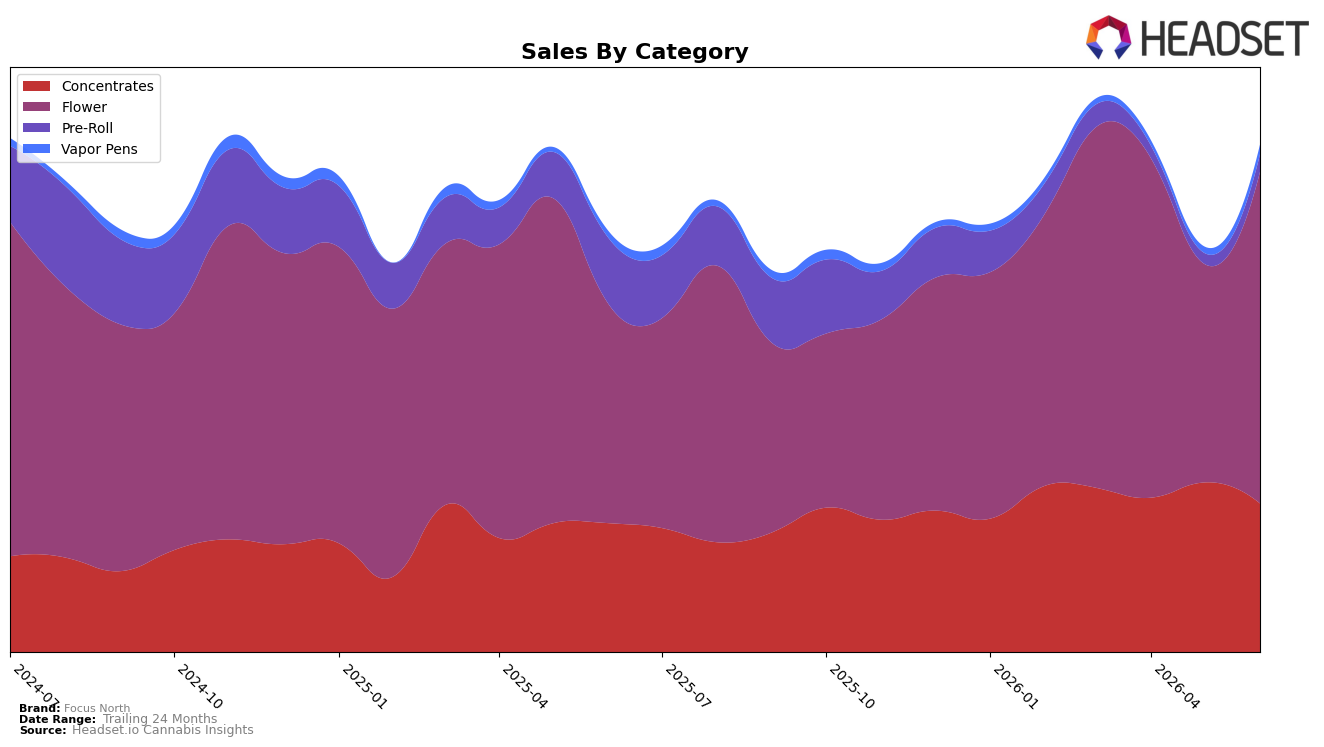

In June 2026, Focus North’s mix tilted further toward Flower, which reached 63.04% share after a 50.11% month‑over‑month gain and a 49.36% year‑over‑year increase, while Concentrates fell 11.86% MoM despite a 14.41% YoY rise, landing at 29.06% share. Pre‑Roll remained a small 4.70% of sales with a 36.26% MoM bump but a 65.65% YoY decline, and Vapor Pens held 3.21% share with 22.58% MoM and 18.72% YoY growth. Against a 19.07% brand‑level YoY sales increase and a 13.89% YoY rise in average price to $32.55, the mix shift implies that June 2026 growth is being driven disproportionately by Flower volume and price, while Concentrates’ MoM slide is ceding share to faster‑moving inhalable formats.

Positioning-wise, anchoring 63.04% of sales in Flower while holding rank 13 in Flower in Oregon suggests a scale play where incremental rank gains can move total brand results more than smaller categories can, given Pre‑Roll’s 4.70% share and Vapor Pens’ 3.21% share. With Concentrates declining 11.86% MoM as Flower surged 50.11% MoM, the brand is effectively concentrating exposure in a single category, which increases sensitivity to Flower price and competitive dynamics; the 13.89% YoY price increase alongside a 49.36% YoY Flower lift indicates room to trade up in Flower while using Pre‑Roll’s 36.26% MoM rebound as a low‑price entry funnel.

Competitive Landscape

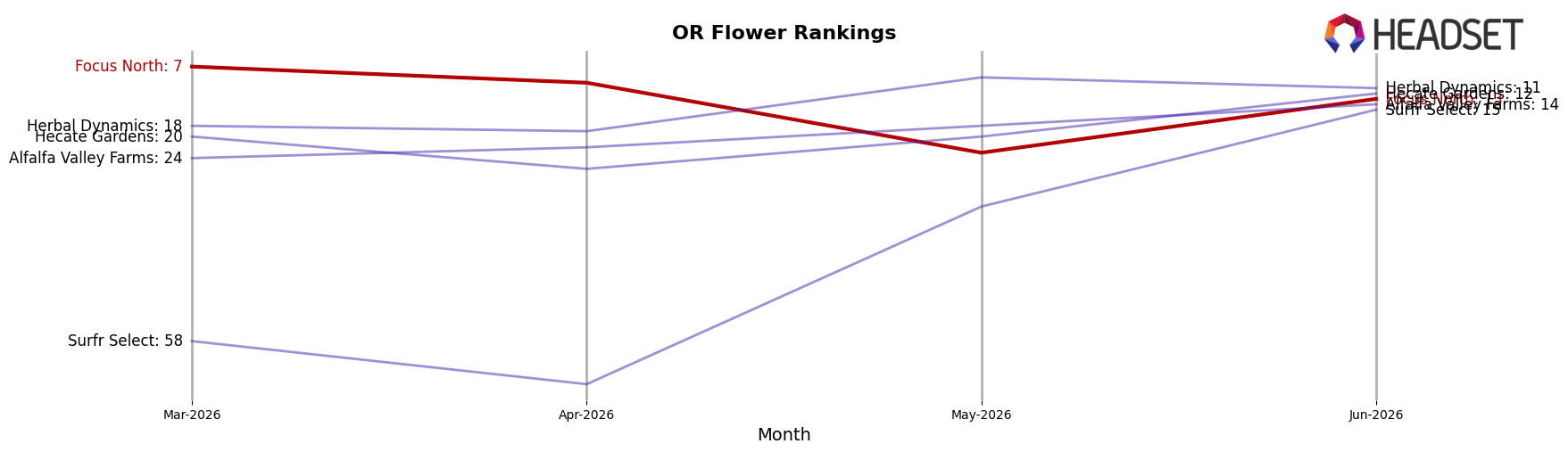

Focus North is ranked #13 in OR Flower in June 2026, improving 9 positions year over year from #22 but falling 6 spots from March 2026’s peak of #7; this places it below PRUF Cultivar / PRŪF Cultivar holding steady at #1 (flat YoY at #1) and behind Grown Rogue which climbed from #6 to #2, while Urban Canna advanced from #12 to #5 as Focus North slid 6 ranks since March 2026; the juxtaposition of a 9-rank YoY gain with a quarter-to-date drop from #7 to #13 implies momentum recovered versus last year but is being outpaced recently by faster risers.

Notable Products

El Chivo (Bulk) posted the steepest move in June 2026 with an -80.4% month-over-month decline as it slid to rank 5, whereas Bomb Sauce (1g) rose +49.5% to rank 6 but stayed just below the +50% breakout threshold. Fatso Pre-Roll 8 Pack (4g) fell -27.0% at rank 7 while Flower SKUs occupied nine of the top ten, concentrating the table around a single category and limiting diversification despite Colorado Sunshine (Bulk) anchoring rank 1 with $126,135 in sales. The pattern implies Focus North is consolidating around bulk Flower strength while phasing or reallocating away from underperforming lines, tightening the portfolio toward high-volume Flower momentum rather than breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.