Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

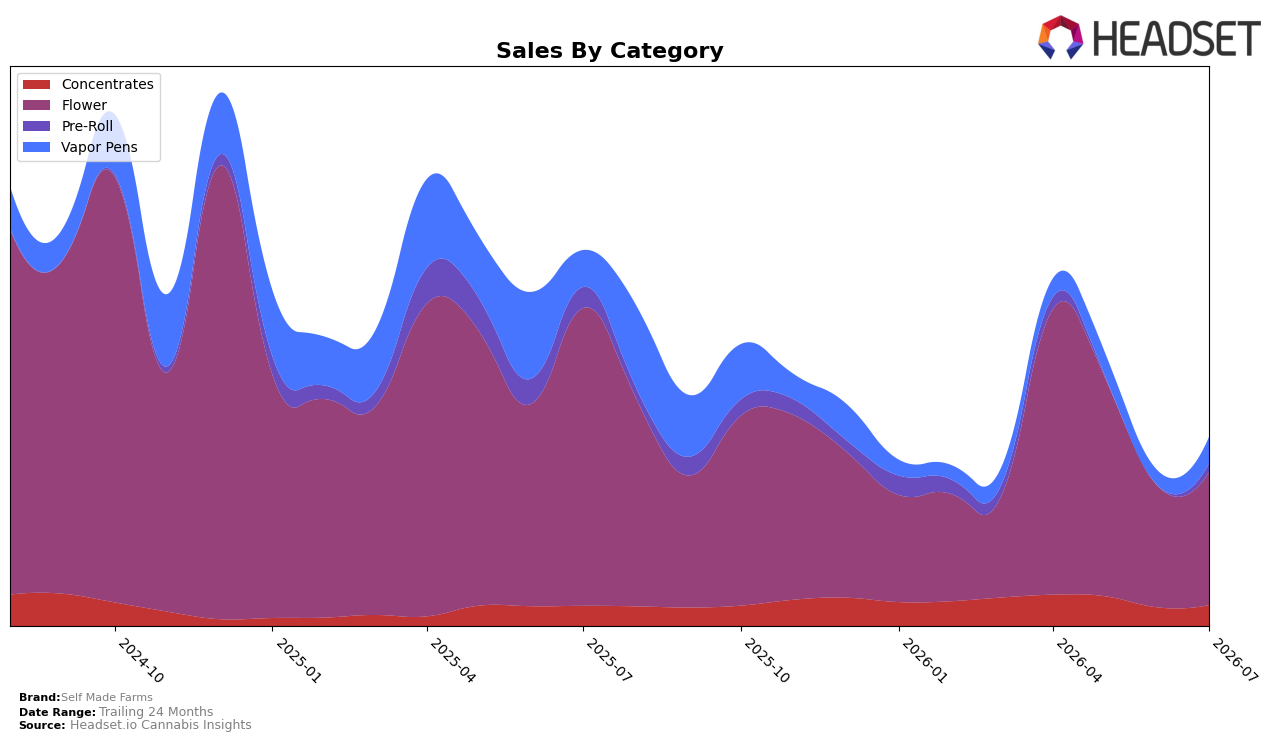

In July 2026, Self Made Farms concentrated 69.24% of sales in Flower, where year-over-year change was -55.14% but month-over-month was +9.49%, while Vapor Pens held 14.21% share with -27.68% YoY and +70.79% MoM. Concentrates accounted for 11.40% share with +3.43% YoY and +11.61% MoM, and Pre-Roll sat at 5.15% share with -55.00% YoY alongside a +545.00% MoM spike. With overall brand sales down 49.10% YoY but average price up 12.59% YoY, the pattern indicates a pivot from a contracting Flower base toward faster-recovering formats, particularly Vapor Pens and Pre-Roll, suggesting short-term mix-driven volume repair despite ongoing annual drag.

These shifts imply Self Made Farms is leaning into quick-rebound formats to stabilize visibility while managing a lower annual baseline: Vapor Pens’ +70.79% MoM and Pre-Roll’s +545.00% MoM lift, against their -27.68% and -55.00% YoY declines respectively, point to tactical shelf reacquisition rather than durable demand gains, whereas Concentrates’ +3.43% YoY and +11.61% MoM provide a steadier foothold. Given a Flower-heavy mix at 69.24% and a category rank of 52 in Flower in Oregon, the implication is that deeper diversification toward Concentrates and measured expansion of Vapor Pens/Pre-Roll could ease dependence on a lagging anchor category while price discipline ($9.996 avg item price) must balance margin with regaining rank.

Competitive Landscape

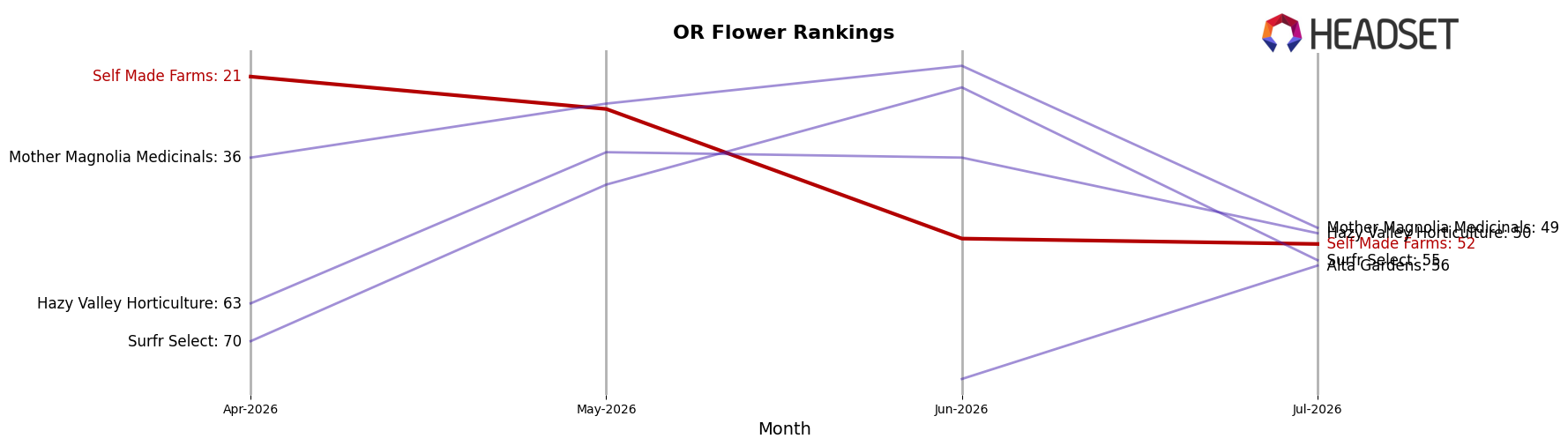

Self Made Farms sits at rank #52 in OR Flower for July 2026, down 36 positions year over year from #16, and 31 spots lower than the April 2026 level of #21; the brand is also 46 positions off its peak of #6 from December 2024, indicating a sustained share retreat. In contrast, PRUF Cultivar / PRŪF Cultivar holds #1 with a +0 year-over-year rank change and a 50.7% sales YoY increase, while Otis Garden advanced to #4 from #12 alongside an 86.2% sales YoY rise, showing upward mobility where Self Made Farms lost 31 ranks since April 2026 and 46 since December 2024. The pattern implies Self Made Farms has transitioned from a top-10 contender to a mid-pack position as escalating gains at the top compress room for recovery unless rank losses reverse in the next two to three months.

Notable Products

Ice Cream Cake Pre-Roll (1g) posted the standout move in July 2026, surging 545% month over month to rank 1, while Rufios (28g) slid 11% to rank 5, indicating share is shifting toward ready-to-consume formats over bulk Flower. Cap Junky (3.5g) climbed 212% to rank 4 and Tyson (28g) rose 176% to rank 6, but Sour Jack (28g) dipped 3% at rank 3, and five of the top ten are Flower SKUs, which concentrates volume yet leaves the lineup exposed to volatility across eighths and ounces. Rufios (3.5g) entered at rank 2 with no comparable month and Blueberry Muffin Distillate Disposable (1g) grew 25% at rank 7, while Concentrates held at rank 10 with Chocolate Chunk Shatter (2g) and total Pre-Roll dollars reached $9,787, pointing to a more diversified upper tier. The pattern implies Self Made Farms is pivoting from a Flower-heavy core toward a mix that balances high-velocity Pre-Rolls with selective Flower winners to reduce reliance on large-format swings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.