Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

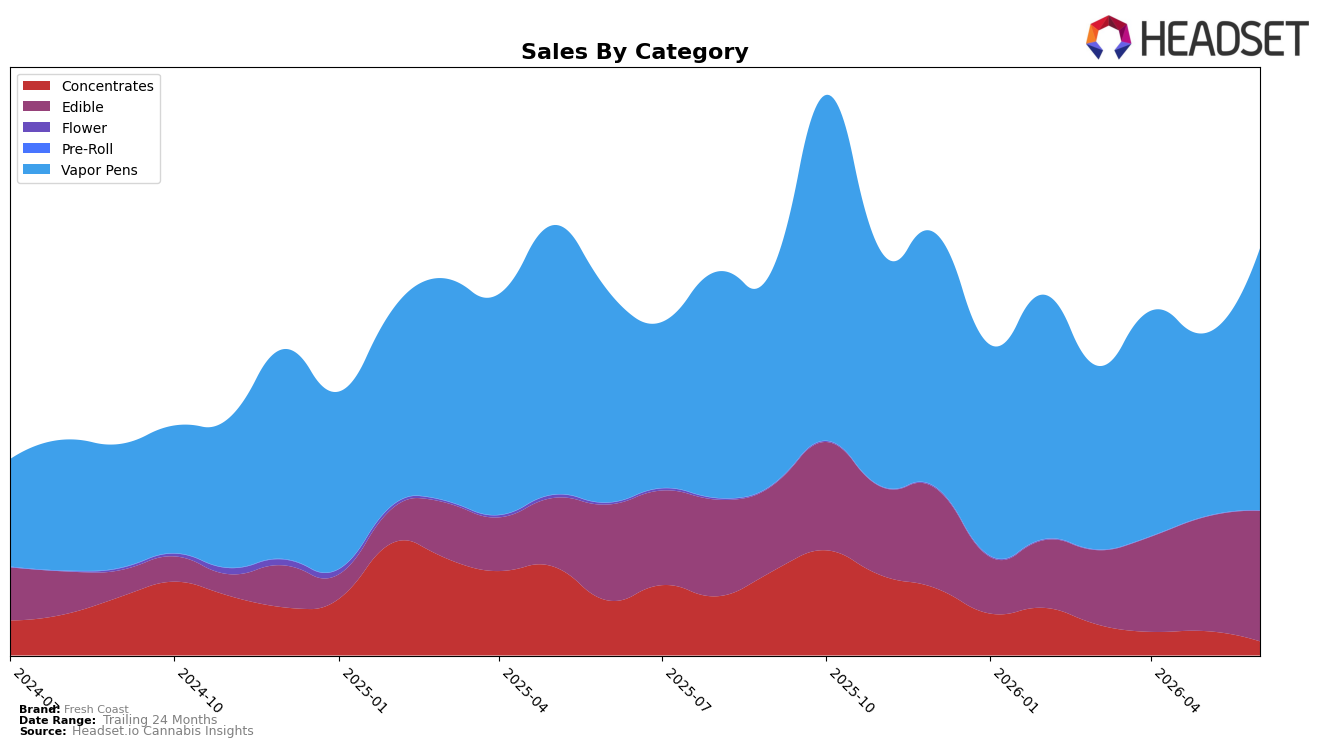

Fresh Coast concentrated 64.50% of June 2026 sales in Vapor Pens with year-over-year growth of 24.02% and month-over-month expansion of 42.93%, while Edible held 32.10% share with 36.09% YoY and 14.67% MoM, and Concentrates fell to 3.40% share with -74.76% YoY and -42.79% MoM. The brand’s average price declined 1.66% YoY alongside total brand sales growth of 11.80% YoY, indicating volume-led gains; within the leading market of Michigan, Vapor Pens ranked 16th, implying mid-pack placement even as category share consolidated. The mix shift toward Vapor Pens (+42.93% MoM vs Edible’s +14.67% MoM) and away from Concentrates (-42.79% MoM) implies Fresh Coast is leaning into higher-velocity SKUs at moderated price points to drive scale.

Given Vapor Pens’ 64.50% share and a 24-month brand sales increase of 120.77%, the 16th rank in Michigan Vapor Pens suggests headroom: outpacing Edible by 32.39 percentage points of mix yet not translating into a top-10 rank. The combination of a 1.66% YoY price decrease and 42.93% MoM Vapor Pen growth implies price-positioning is unlocking trial and repeat, while a -74.76% YoY collapse in Concentrates signals deliberate pruning of underperforming sublines; together these shifts position Fresh Coast as a value-accessible Vapor Pens and Edible player prioritizing velocity over breadth.

Competitive Landscape

Fresh Coast sits at rank #16 in MI Vapor Pens in June 2026, down 1 position year over year from #15, but up 5 places versus March 2026 when it was #21; the brand also trails its category peak of #10 set in October 2025 by 6 ranks. Competitive movement has been volatile: MKX Oil Company advanced from #3 to #1 while growing sales 68.3% year over year, and Society C surged from #29 to #4 with a 756.2% sales increase, whereas Mitten Extracts slipped from #1 to #2 alongside a 20.1% sales decline. The combination of a 1-rank YoY drop and a 5-rank rebound in the last three months signals Fresh Coast is stabilizing mid-pack but ceding ground to faster-climbing rivals, implying near-term share pressure unless the upward quarterly momentum converts into sustained rank gains.

Notable Products

Ritual - Pink Lemonade Jellies 10-Pack (200mg) posted the largest month-over-month gain at +38.7% and rose to rank 2 in June 2026, while Splash - CBN/THC 1:2 Mixed Berry Live Resin Gummies 10-Pack (100mg CBN, 200mg THC) slipped -9.0% at rank 6, and Splash - THC/CBN 2:1 Blueberry Live Resin Gummies 10-Pack (200mg THC, 100mg CBN) held rank 1 with +13.2%. Five of the top ten are Ritual Jellies SKUs, and all ten products are Edibles, indicating a concentrated portfolio where flavor-led jellies are accelerating faster than cannabinoid-complex SKUs; this mix implies Fresh Coast is leaning into scalable, flavor-driven Edibles for share capture over June 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.