Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

True North Collective is stocked at 344 licensed dispensaries across Michigan, with the deepest coverage in New Buffalo, Detroit, Grand Rapids, Monroe, and Kalamazoo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

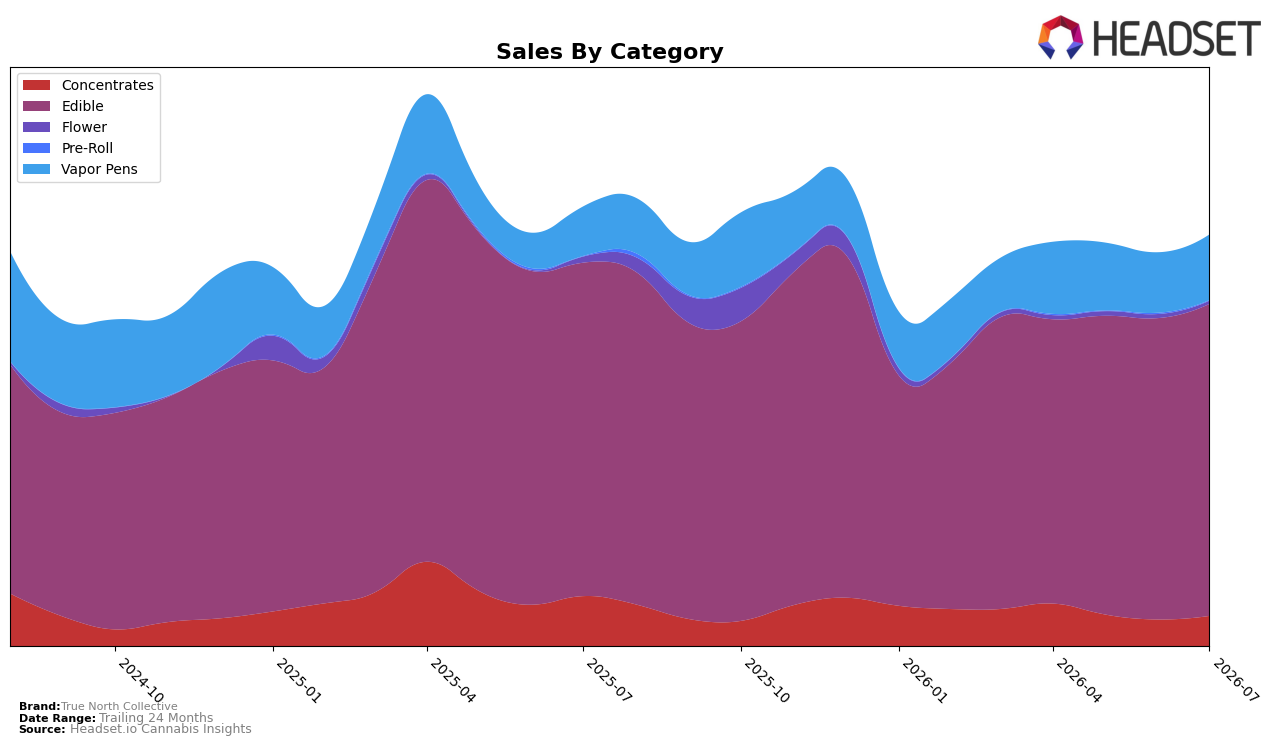

In July 2026, True North Collective concentrated 76.00% of sales in Edible, where sales were down 6.43% year over year but up 3.54% month over month, while Vapor Pens expanded to a 15.92% share with 32.86% YoY growth and 8.63% MoM growth. Concentrates held 7.32% share with a 39.74% YoY decline but a 13.46% MoM lift, and Flower slid to 0.69% share with a 50.43% YoY drop and a 23.57% MoM decline. Pre-Roll contracted to 0.05% share with an 8.90% YoY decrease and a 75.12% MoM fall, and the brand’s average price rose 14.20% YoY to $4.996 while total brand sales fell 6.39% YoY, placing Edible at the center of performance risk and Vapor Pens as the offsetting growth lever.

The category tilt implies a defensive posture anchored in Edible, where the brand sits at rank 8 in Michigan, but future upside depends on reallocating toward Vapor Pens, which outgrew Edible by 39.29 percentage points YoY and 5.09 points MoM. The divergence between a 7.98% 24‑month sales gain and a 6.39% YoY decline points to mix drag from Concentrates and Flower, whose combined share of 8.01% carries steep YoY contractions of 39.74% and 50.43%, respectively; shifting 2–3 share points from these declining areas into Vapor Pens could neutralize the YoY shortfall and reinforce Edible’s July 2026 MoM recovery of 3.54% without overexposing the portfolio to single-category volatility.

Competitive Landscape

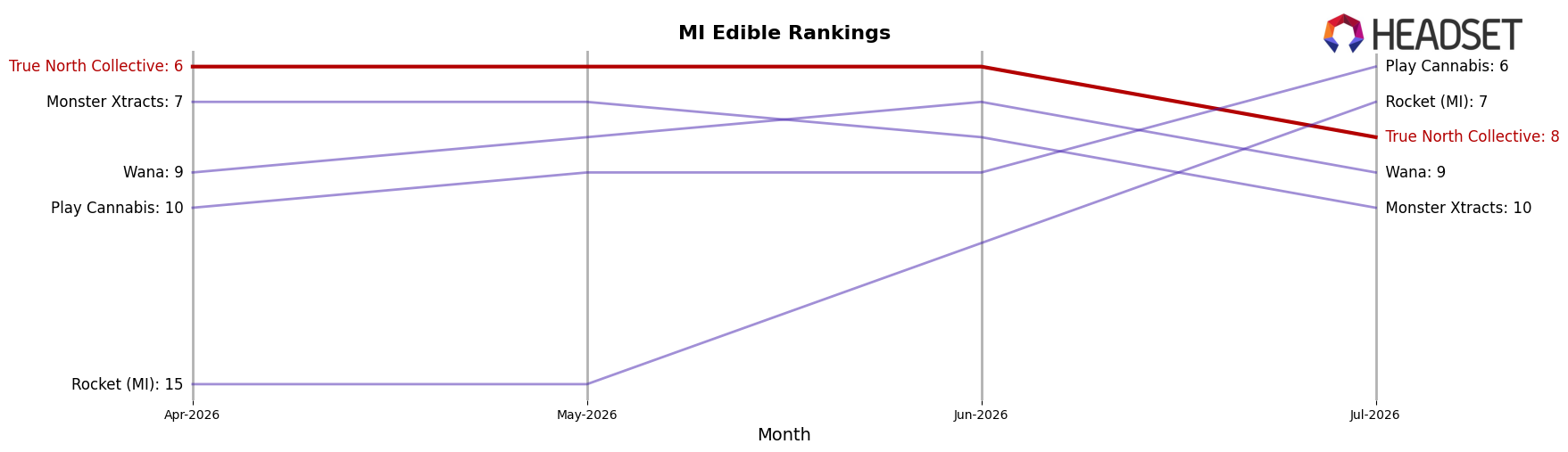

True North Collective sits at rank #8 in MI Edible for July 2026, unchanged year over year at #8 while sliding 2 positions from #6 in April 2026 to #8 in July 2026; that three-month decline contrasts with a peak at #6 in June 2026 and indicates share pressure within the top 10. Meanwhile, Wyld held #1 year over year but did so amid a -23.3% YoY sales change, and Camino climbed from #4 to #3 with +12.9% YoY sales, signaling that gains at the top are uneven and openings exist when leaders contract. With MKX Oil Company slipping from #3 to #4 despite a +4.6% YoY lift and Good Tide fixed at #5 amid a -25.3% YoY decline, True North Collective’s flat YoY rank alongside a recent 2-position drop implies a stalled trajectory that risks ceding mid-tier ground unless short-term execution recaptures the June 2026 peak.

Notable Products

One Hitter - Tutti Frutti Gummy (200mg) set the tone in July 2026 with a -21.9% month-over-month slide while holding rank 4, contrasting sharply with One Hitter - Cherry Limeade Gummy (200mg) at rank 3 on a +31.1% surge. One Hitter - Blueberry Lemon Haze Gummy (200mg) led the board at rank 1 with +20.6% MoM and $52,733 in sales, while One Hitter - Orange Dreamsicle Gummy (200mg) fell -19.5% at rank 5, creating a spread where gains are concentrated in a few SKUs despite adjacent flavors retreating. With all top ten items in Edible and seven carrying the One Hitter sub-line, the mix points to flavor-level volatility inside a single format, implying True North Collective is doubling down on gummy breadth while pruning underperforming variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.