Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Society C is stocked at 425 licensed dispensaries across Michigan, with the deepest coverage in New Buffalo, Detroit, Grand Rapids, Monroe, and Kalamazoo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

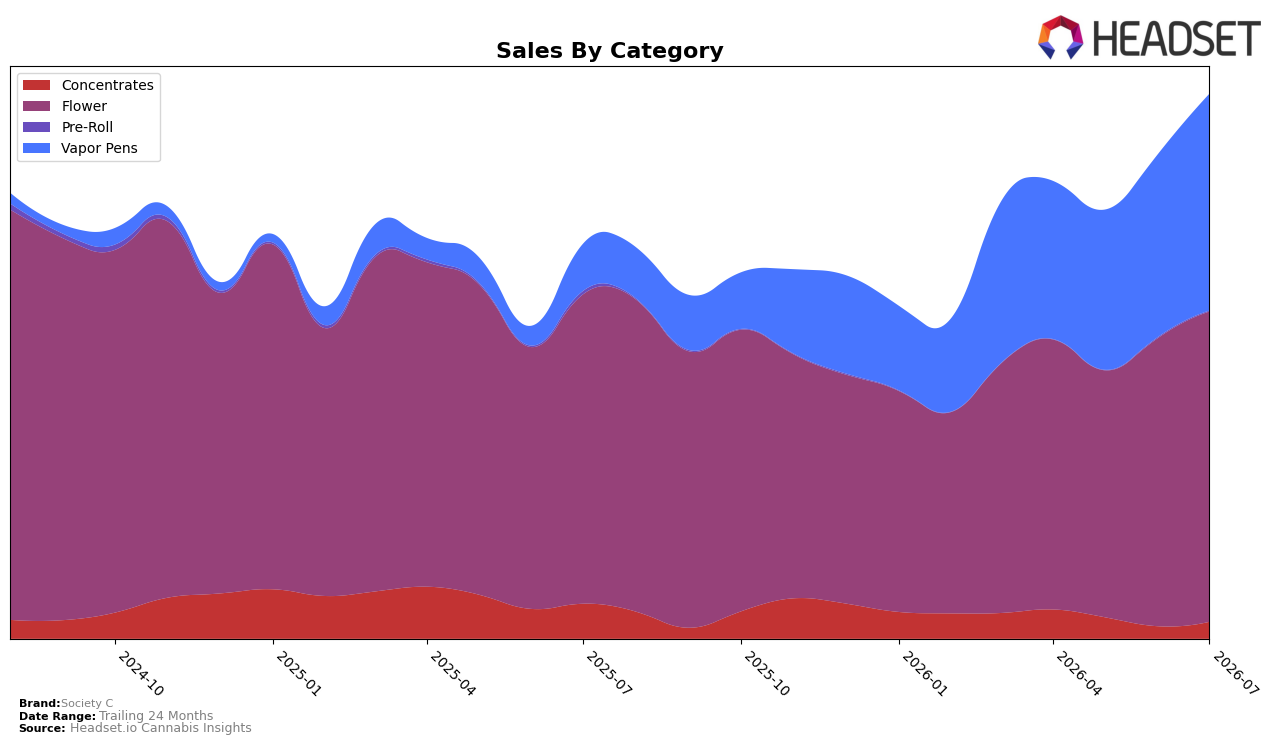

In July 2026, Society C’s mix is anchored by Flower at 56.98% share with 0.28% year-over-year growth and 7.68% month-over-month, while Vapor Pens command 39.81% share with 360.76% year-over-year and 18.58% month-over-month gains; together they constitute a two-category core that expanded faster month-over-month than the brand’s 12.50% average price increase year-over-year. In contrast, Concentrates hold 3.08% share with a 51.89% year-over-year decline despite a 35.84% month-over-month rebound, and Pre-Roll sits at 0.12% share with year-over-year down 79.02% and month-over-month down 16.32%; the pattern implies Society C is consolidating around Flower and Vapor Pens while exiting breadth plays in smaller formats, especially in Michigan where Society C ranks 2 in Flower.

The pivot toward Vapor Pens at 39.81% share alongside Flower’s 56.98% share, combined with ranking 2 in Michigan Flower, suggests a hedged positioning that reduces reliance on a single category while leveraging price elasticity reflected in a 12.50% brand-wide average price increase year-over-year and a 7.68% month-over-month lift in Flower. The simultaneous 35.84% month-over-month recovery in Concentrates amid a 51.89% year-over-year contraction, together with Pre-Roll’s 79.02% year-over-year decline and 16.32% month-over-month drop, implies selective pruning of low-yield formats to protect velocity in higher-penetration channels, pointing to a strategy that trades depth in lagging segments for sustained share capture in Flower and accelerated penetration in Vapor Pens.

Competitive Landscape

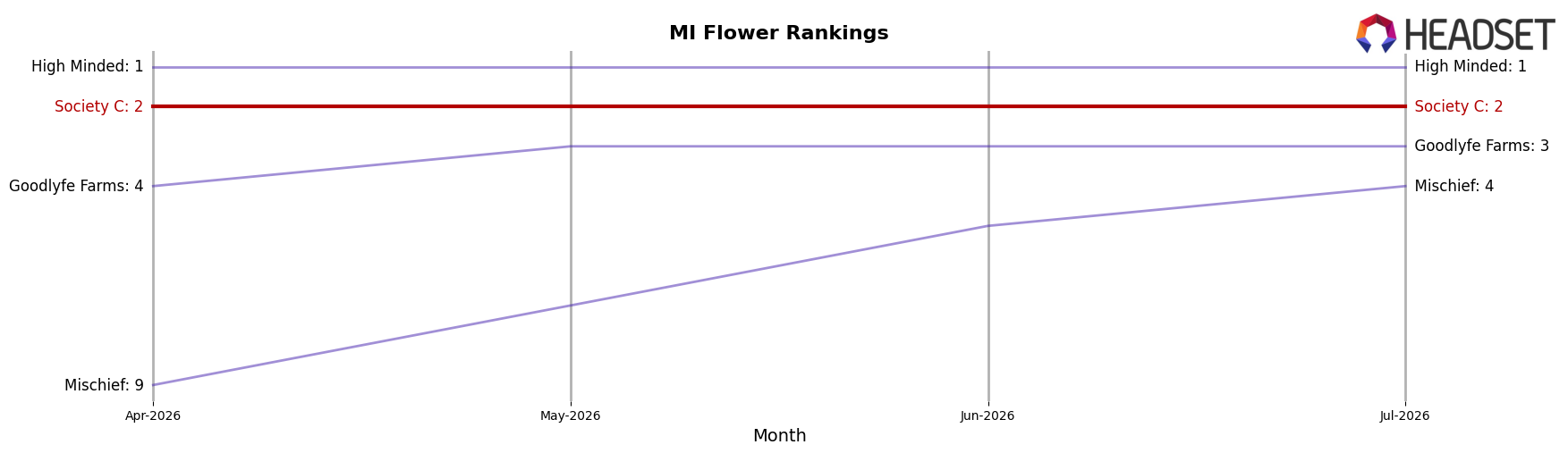

Society C sits at rank #2 in MI Flower for July 2026, unchanged YoY from #2, with a prior peak at #1 in January 2025 and stability at #2 over the last three months, while High Minded holds #1 both currently and YoY as its sales fell 12.46% year over year and Goodlyfe Farms climbed from #5 YoY to #3 with 36.83% sales growth. The competitive gap is tightening below the top spot as Mischief rose from #10 YoY to #4 on 59.39% growth, while Pro Gro slipped from #3 YoY to #5 amid a 12.04% decline, indicating that Society C’s flat #2 YoY and three-month hold at #2 position it as the primary challenger, but the accelerating upward pressure from #3–#4 implies that maintaining #2 without renewed momentum risks ceding ground even if #1 softens.

Notable Products

Omega Runtz (3.5g) posted the standout move in July 2026 with a +55.5% month-over-month surge, jumping into rank 7 while Gastro Pop (3.5g) rose +45.1% to consolidate rank 1. In contrast, The Runtz (3.5g) slipped -7.1% at rank 4 as Blue Nerdz (3.5g) edged up +10.2% at rank 3. Eight of the top ten are Flower SKUs, and Fruity Pebbles Live Resin Disposable (2g) held rank 10 with +0.5% on $155,148, indicating Society C’s momentum is anchored in Flower where gains are concentrating at both the top and mid-pack.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.