Market Insights Snapshot

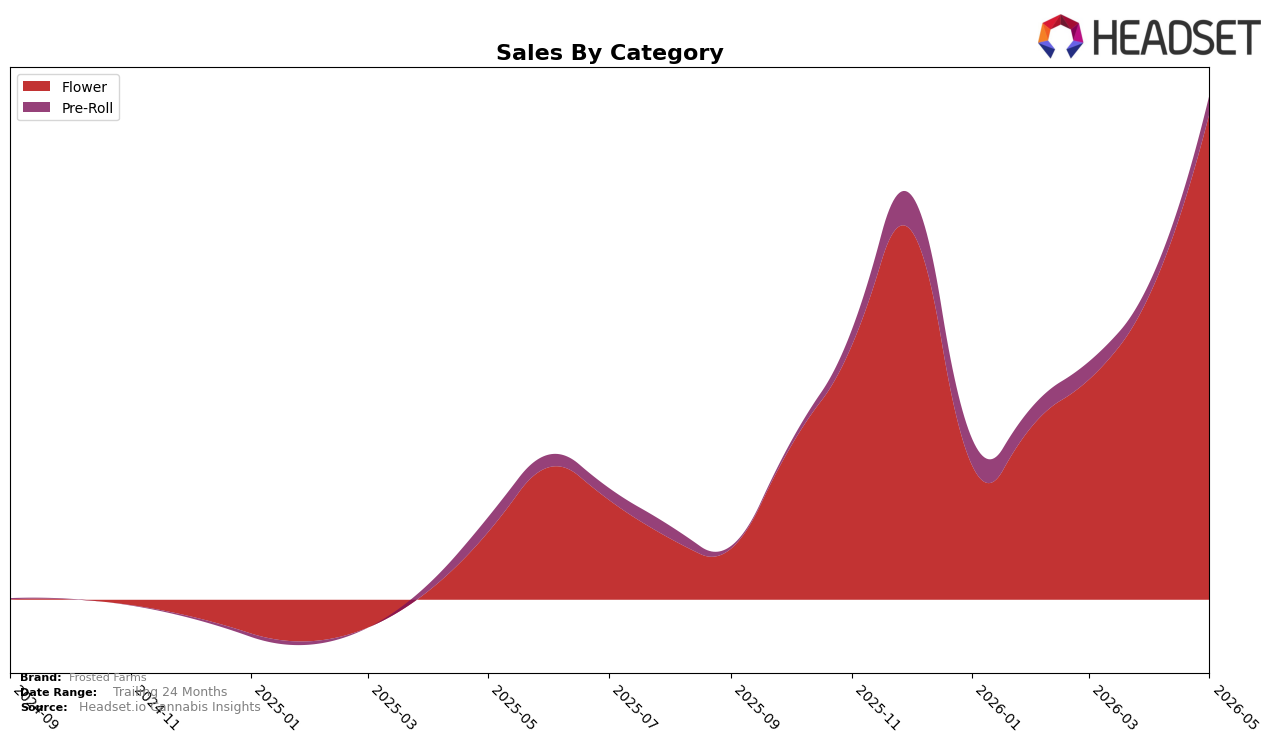

Frosted Farms concentrated 96.39% of May 2026 sales in Flower, with Pre-Roll at 3.61%, while Flower grew 622.14% year over year and 58.86% month over month versus Pre-Roll’s 24.83% year over year and 53.25% month over month; this tilt coincided with an average price drop of 39.93% year over year to $11.42 and a Flower average price of $11.76. The brand’s overall sales rose 515.84% year over year as Flower captured nearly all category share, implying the mix shift is being driven by volume expansion at lower price points and reinforcing dependence on a single category for growth.

With a 24th rank in Flower in Michigan and 96.39% of volume tied to Flower, the 58.86% month-over-month lift in that category against 53.25% in Pre-Roll suggests positioning as a price-competitive Flower specialist rather than a diversified portfolio. The combination of a 622.14% year-over-year Flower surge and a 39.93% decline in average price indicates a strategy anchored on accessible price tiers to gain share, which implies near-term rankings can improve through sustained Flower velocity but long-term resilience will depend on either maintaining low-price scale or gradually broadening mix beyond the current 3.61% in Pre-Roll.

Competitive Landscape

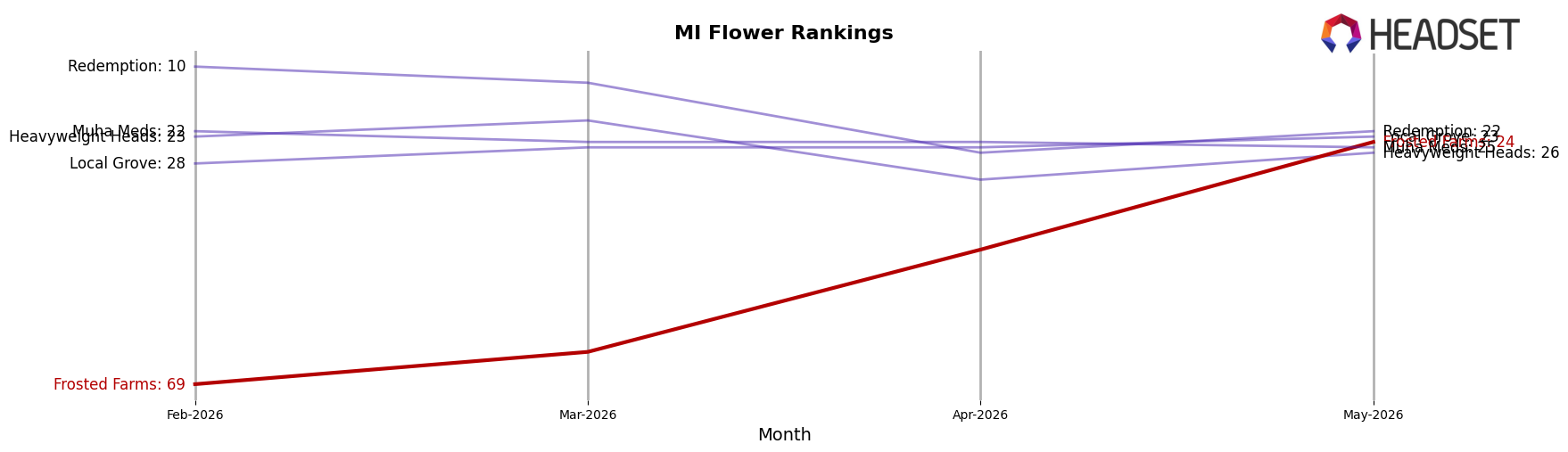

Frosted Farms sits at rank #24 in MI Flower in May 2026, improving 138 spots from #162 year over year while jumping 45 places from #69 three months ago; this new peak at #24 in May 2026 contrasts with Grown Rogue accelerating to #5 with a 245.9% YoY sales gain and High Minded holding #1 despite a -14.5% YoY sales decline. The spread between Frosted Farms at #24 and Goodlyfe Farms at #2 after rising from #7, alongside Society C easing from #2 to #3 with -17.6% YoY sales, indicates Frosted Farms’ rapid rank catch-up is timing into a reshuffling where some leaders are contracting while fast risers gain share; the trajectory implies Frosted Farms has moved from obscurity into the competitive mid-tier and is positioned to contest the teens if momentum from the last three months persists.

Notable Products

Sticky Ricky OG (28g) posted the largest month-over-month surge at +1,152.8% to rank 4, outpacing Afghani Supernova (1g) at +445.4% in rank 1 and Summertime (3.5g) at +474.3% in rank 2. In contrast, Sticky Ricky OG (Bulk) slipped -14.2% at rank 7 while Glue Cheese (Bulk) rose +53.5% at rank 3. The pattern implies velocity has shifted toward smaller package Flower that can jump ranks rapidly while bulk formats fragment demand within the same strain family.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.