May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

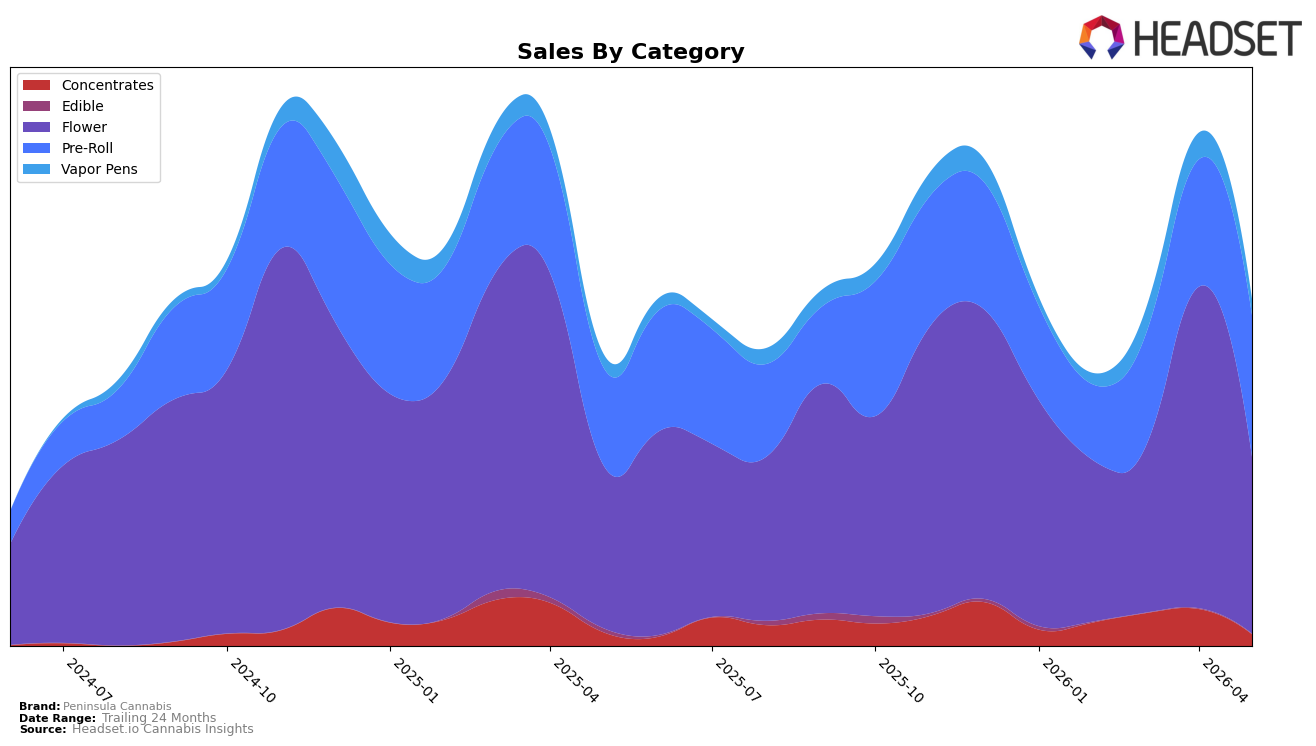

Peninsula Cannabis concentrated over half of May 2026 revenue in Flower at 51.03% share, yet Flower fell 45.06% month over month even as it rose 8.43% year over year, while Pre-Roll climbed to 40.91% share with 11.35% MoM growth and 45.10% YoY expansion. Smaller lines swung sharply: Vapor Pens held 4.59% share with an 18.54% YoY lift but a 40.14% MoM decline, and Concentrates at 3.39% share contracted 14.53% YoY and 68.27% MoM; Edible was 0.07% share with a 93.18% YoY drop and 49.05% MoM decline. With average price up 10.41% YoY alongside brand sales up 18.81% YoY, the mix shift toward Pre-Roll and away from Flower and Concentrates implies near-term reliance on a lower-priced volume engine while the largest category resets seasonally.

Positioning is tilting from a Flower-led anchor to a dual-track strategy where Pre-Roll growth offsets volatility in Flower, evidenced by Pre-Roll’s 11.35% MoM rise against Flower’s 45.06% MoM decline and Vapor Pens’ 40.14% MoM decline. Given a 53 rank in Flower in Michigan and Pre-Roll’s 45.10% YoY growth, the brand’s competitive footing hinges on defending Flower scale while exploiting Pre-Roll momentum; sustaining the 18.81% YoY brand sales increase with a 10.41% YoY price gain suggests pricing power is acceptable if mix keeps expanding in Pre-Roll and stabilizing in Vapor Pens.

Competitive Landscape

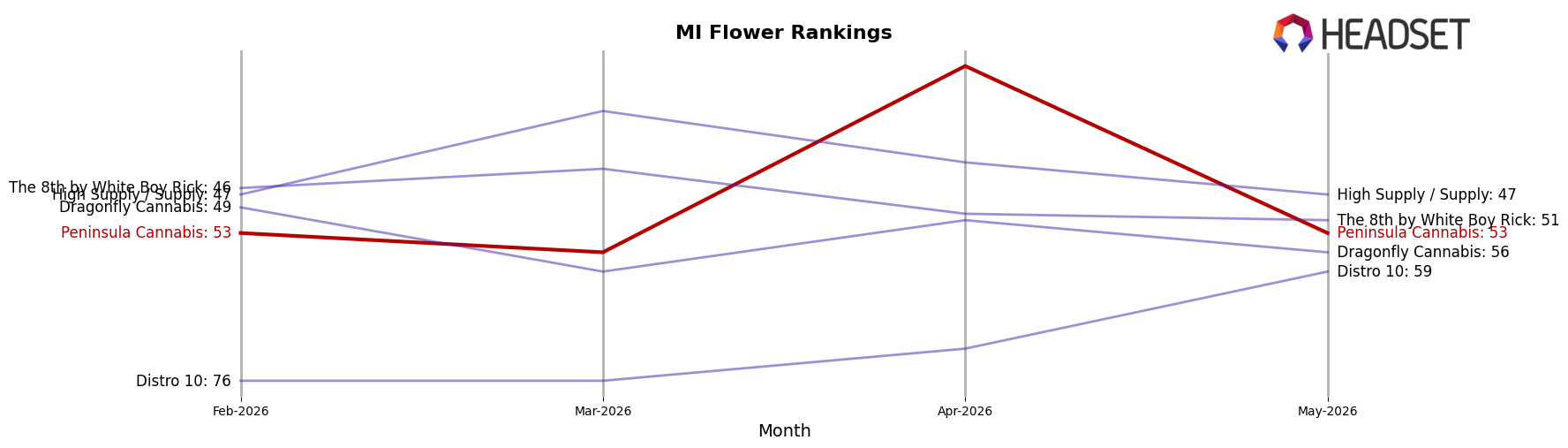

Peninsula Cannabis sits at rank 53 in May 2026, improving 8 positions from rank 61 year over year, while holding flat versus February 2026 at rank 53; this contrasts with top-tier volatility where Grown Rogue vaulted from rank 29 to rank 5 and Goodlyfe Farms advanced from rank 7 to rank 2. Despite a historical peak at rank 24 in November 2024, Peninsula Cannabis remains outside the top 50 at rank 53 as of May 2026, whereas High Minded held rank 1 both this year and last year even while posting a -14.5% year-over-year sales change, and Society C stayed near the top from rank 2 to rank 3 with a -17.6% year-over-year sales change. The pattern implies incremental recovery from rank 61 to 53 but a stalled climb relative to faster-moving competitors surging into the top 10.

Notable Products

Electric Peanutbutter Cookie Pre-Roll (1g) posted the steepest decline in May 2026 at -28.0% MoM while sliding to rank 3, as Sherb Pie (3.5g) fell -31.3% MoM at rank 10, pointing to pressure on legacy Flower and certain Pre-Roll SKUs. In contrast, Party Poppers Pre-Roll (1g) surged 58.7% MoM to rank 2 and Runtz Pre-Roll (1g) rose 1.8% MoM at rank 1, with at least six of the top ten coming from the Pre-Roll category, indicating assortment gravity is consolidating around Pre-Rolls. Runtz (7g) dropped -29.2% MoM at rank 4 even while generating $238,332, reinforcing that unit velocity rather than ticket size is carrying the leaderboard.

The mix shift implies Peninsula Cannabis is tilting toward smaller-format, momentum Pre-Rolls over larger Flower packs, which can lift share through frequency even as high-dollar Flower SKUs face rank and MoM headwinds.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.