Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

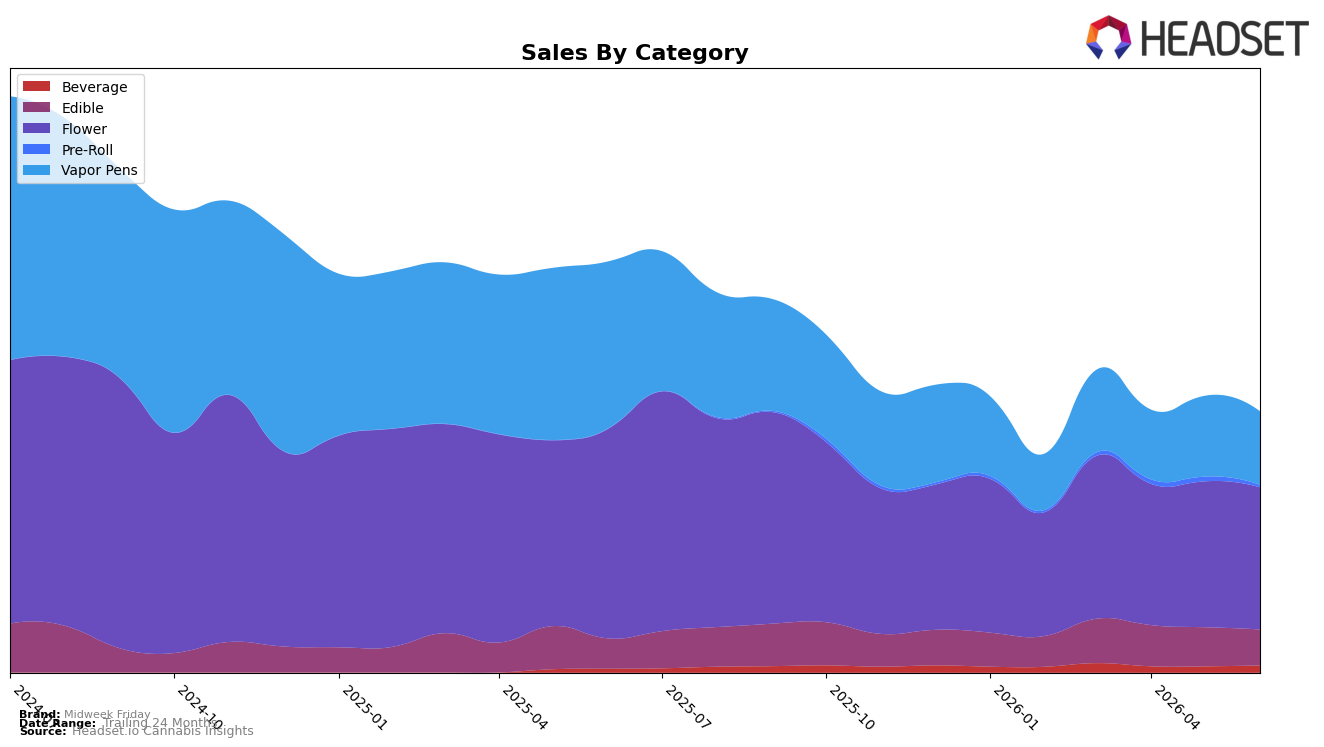

Midweek Friday’s mix in June 2026 concentrated 54.52% of sales in Flower with a year-over-year decline of 32.24% and a month-over-month dip of 2.56%, while Vapor Pens held 28.15% share but contracted faster at 56.04% YoY and 9.07% MoM, shifting the portfolio toward lower-volatility categories. Edible rose 19.07% YoY despite a 7.91% MoM pullback to 13.75% share, and Beverage expanded 83.81% YoY with a 13.96% MoM gain to 2.71% share; meanwhile, Pre-Roll spiked 1224.60% YoY but fell 49.35% MoM, indicating promotional or distribution volatility rather than stable demand. The pattern implies Midweek Friday is re-weighting from Vapor Pens to Flower and Edible as near-term volume anchors, with Beverage serving as a small but accelerating contributor that counterbalances double-digit declines elsewhere.

Positionally, the 15th rank in Flower in Illinois coupled with a 32.24% YoY decline versus Vapor Pens’ 56.04% YoY drop suggests defending Flower share is the primary route to visibility, while Edible’s 19.07% YoY growth offers a secondary lane to diversify away from price-sensitive inhalables. The 13.96% MoM gain in Beverage alongside a 2.56% MoM slide in Flower and a 9.07% MoM slide in Vapor Pens indicates incremental wins are accruing in emerging formats, but the 49.35% MoM contraction in Pre-Roll warns against leaning on that segment for sustained placement. The implication is to anchor assortment and pricing around Flower and Edible to stabilize rank while using Beverage’s momentum for incremental distribution, avoiding overexposure to categories exhibiting double-digit MoM volatility.

Competitive Landscape

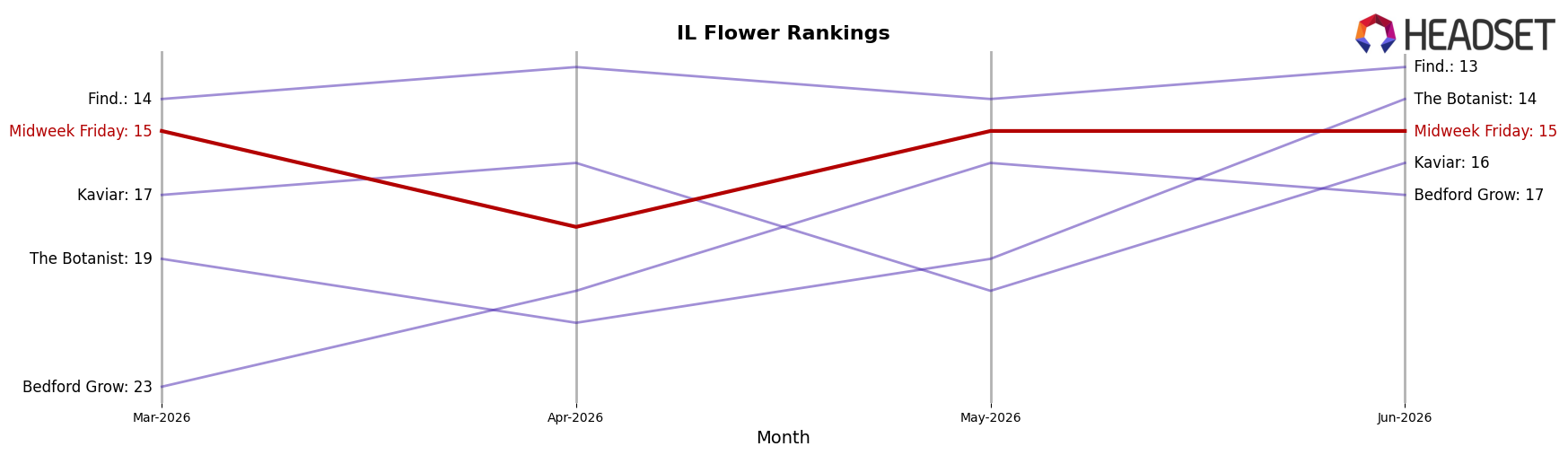

Midweek Friday sits at rank #15 in IL Flower with a year-over-year slide from #12, a 3-position drop that also leaves it flat versus March 2026 at #15; this contrasts with High Supply / Supply holding #1 both this year and last while expanding sales by 32.1%, and RYTHM staying at #2 despite a 5.2% sales decline. The brand’s current #15 is six spots below its peak of #9 in September 2025, while Good Green climbed from #4 to #3 on 30.9% growth and &Shine jumped from #10 to #5 with a 5-rank gain. The pattern implies Midweek Friday is ceding relative shelf position as faster-rising rivals consolidate share at the top, and absent a reversal the brand’s rank is more likely to drift toward the high teens than to reapproach the #9 peak.

Notable Products

Tangerine Energize Gummies 10-Pack (100mg) led with a -21.1% MoM drop while holding rank 1, and Strawberry Doze Gummies 10-Pack (100mg) slipped -8.7% at rank 2; with three Edibles in the top three and Beverage entries rising 30.5% at rank 8 and 11.6% at rank 4, the product mix is tilting away from a single-flavor Edible anchor toward a more diversified set of formats. Strawberry Milkshake Distillate Cartridge (1g) climbed 23.6% into rank 10 while Lemon Vibe Pectin Gummies 10-Pack (100mg) eased -2.6% at rank 3, and Flower newcomers entered at ranks 6 and 9 with a combined $100,227, indicating basket broadening despite Edible softness. The concentration of three Edibles in the top three alongside two Beverages in the top eight implies a pivot toward cross-category hedging to stabilize volume against flavor-specific volatility in July 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.