Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

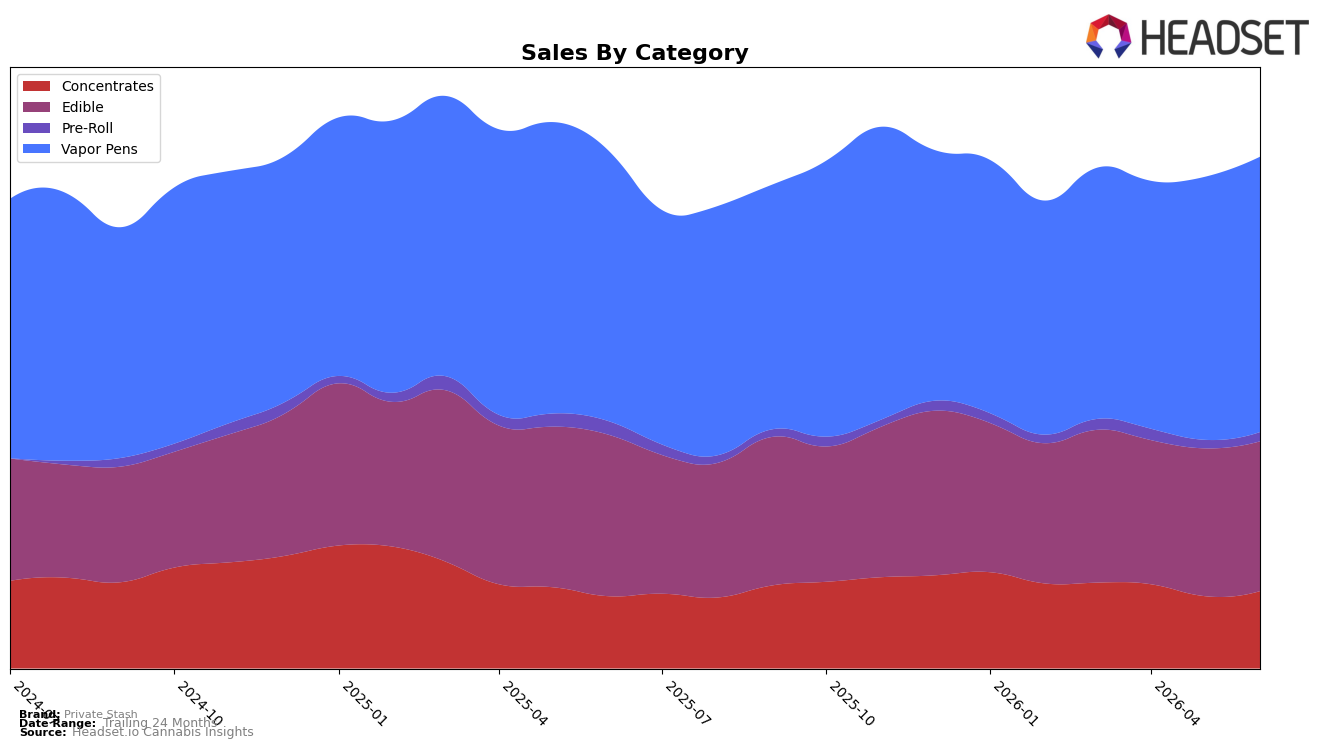

In June 2026, Private Stash concentrated 53.58% of sales in Vapor Pens with year-over-year growth of 1.70% and month-over-month growth of 4.69%, while Edible held 29.23% share but declined 7.23% YoY and inched up 1.33% MoM. Concentrates rose 6.89% YoY and 6.84% MoM to 15.20% share, and Pre-Roll, despite a 29.72% YoY drop, climbed 7.97% MoM at a 1.98% share; combined with an average price up 3.04% YoY and brand sales down 1.23% YoY, the mix points to margin-leaning categories offsetting softness in Edible. With Vapor Pens ranking 22 in Oregon within its category and MoM gains in three of four categories, the thesis is that Private Stash is pivoting toward higher-ticket inhalables to stabilize revenue while digesting Edible contraction.

The category shifts imply a positioning that leans into inhalable differentiation: Concentrates’ 6.89% YoY and 6.84% MoM growth alongside Vapor Pens’ 1.70% YoY and 4.69% MoM suggest portfolio emphasis where trial and repeat are responsive to pricing, whereas Edible’s 7.23% YoY decline and only 1.33% MoM lift indicate price-sensitive or saturated segments. Given the 22 rank in Oregon for Vapor Pens and a 3.04% YoY average price increase, the implication is that Private Stash can trade up within inhalables to improve unit economics, but must either reposition Edible or let share migrate toward Concentrates to prevent the 1.23% YoY brand sales dip from persisting.

Competitive Landscape

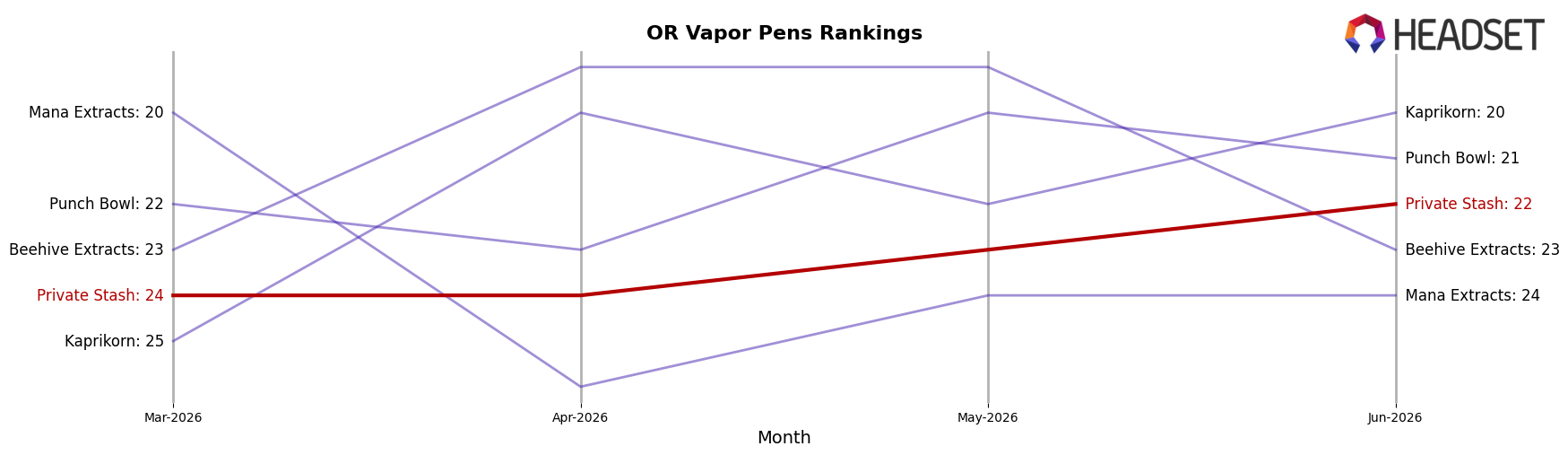

Private Stash sits at rank 22 in Oregon Vapor Pens in June 2026, unchanged year over year at rank 22, after a modest climb from rank 24 three months ago and below its peak rank 19 in November 2025; meanwhile, Buddies holds rank 1 after improving from rank 2 year over year while growing sales 16.9%, and FRESHY advanced from rank 5 to rank 2 on 81.5% YoY sales growth, indicating faster upward mobility among leaders than Private Stash’s flat YoY position. With Entourage Cannabis / CBDiscovery sliding from rank 1 to rank 3 on a 38.9% YoY sales decline and Oregrown rising from rank 11 to rank 5 on 57.4% YoY growth, the mix around the top compressed while Private Stash’s static rank and retreat from a peak at rank 19 imply it is treading water as category momentum concentrates among movers.

Notable Products

Hybrid Pink Lemonade Full Spectrum Fruit Chew Blast (100mg) set the tone in June 2026 with a -11.1% month-over-month decline while still holding rank 1, a juxtaposition to Bohemian Blue Razzberry Fruit Chew Blast (100mg) at rank 2 with +12.3% and Hybrid Berry Blackberry Fruit Chew Blast Fruit Chew 2-Pack (100mg) at rank 3 with +28.3%. Eight of the top ten SKUs posted positive MoM ranging from +2.0% to +28.3%, and the top three ranks are all Edibles with ranks 1–3, implying the category is consolidating share even as the lead SKU softens. The pattern suggests Private Stash is leaning into breadth within a single format, using mid-pack growth to offset a contracting flagship.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.