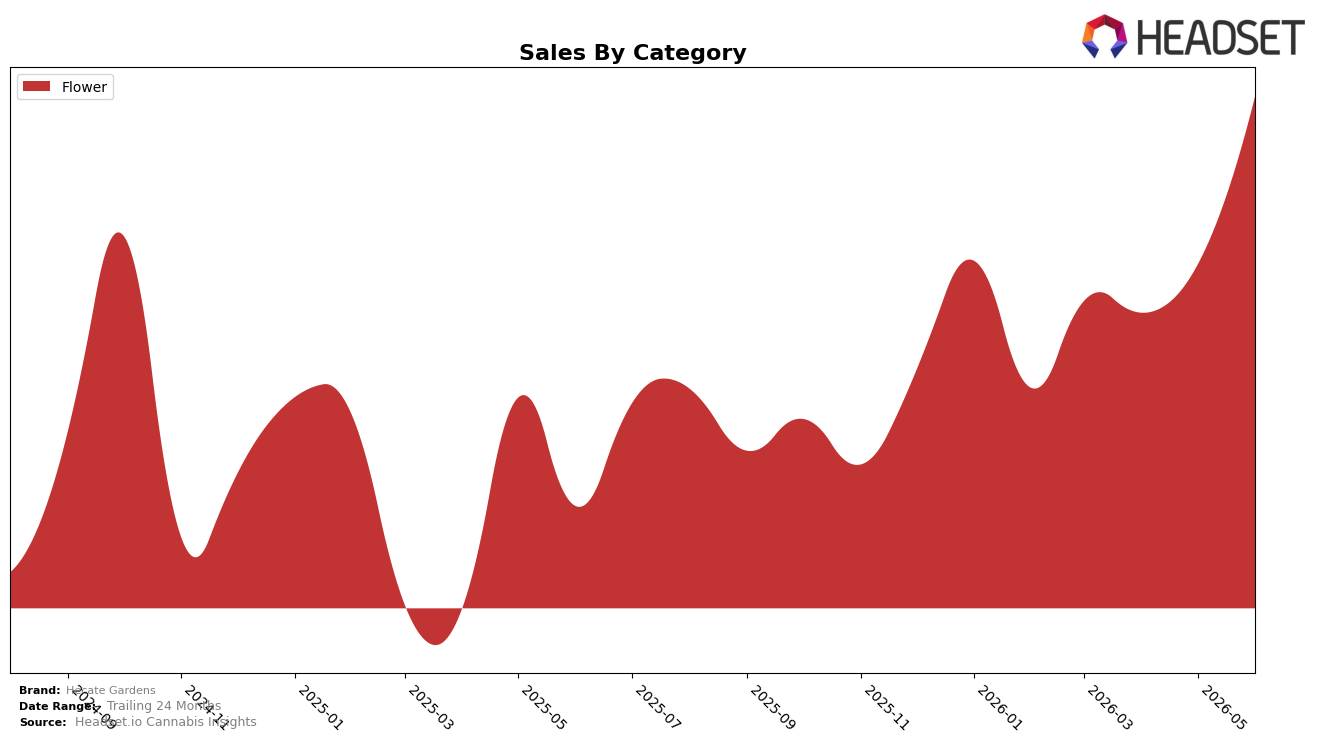

Market Insights Snapshot

In June 2026, Hecate Gardens concentrated 100.0% of sales in Flower, with category sales up 227.1% year over year and 40.1% month over month, while the average price fell 13.6% versus last year. Within Oregon Flower, the brand sat at rank 12 for June 2026, indicating volume gains outpacing price contraction and lifting share despite a lower ticket. The pattern implies a volume-led expansion strategy in a single-category footprint, where accelerated month-over-month velocity alongside a double‑digit price decline supports unit growth but concentrates exposure to Flower cycles.

The single-category stance positions Hecate Gardens to compete on unit throughput rather than mix optimization, as 100.0% Flower share anchors the brand in a price-elastic segment while a 227.1% year-over-year sales surge and a 40.1% month-over-month bump signal reliance on promotional or value tiers. Holding rank 12 in Oregon suggests headroom to trade up within Flower; the 13.6% average price decline creates a value moat but may cap premium positioning unless pricing stabilizes. The implication is a defensible share play built on volume density that will require either gradual price normalization or a second-category entry to reduce margin sensitivity.

Competitive Landscape

Hecate Gardens is ranked #12 in OR Flower in June 2026, improving 37 positions year over year from #49 and rising 8 spots since March 2026 when it was #20; this move coincides with a climb to its peak rank of #12 in June 2026 while top rivals held or advanced at the very top. In the same period, PRUF Cultivar / PRŪF Cultivar held #1 with a year-over-year rank of #1 as well, and Grown Rogue moved from #6 to #2 with 123.97% year-over-year sales growth, indicating the leaders are consolidating share even as Hecate Gardens accelerates its ascent. The pattern implies Hecate Gardens’ rapid rank compression toward the top 10 is driven by momentum faster than the category median, but future gains may require displacing incumbents with entrenched top-5 positions.

Notable Products

Classic Kush (1g) posted the sharpest movement in June 2026 with a +143% month-over-month surge and climbed to rank 6, while Sun Kissed Orange (1g) fell -12% MoM and slipped to rank 8. Low Tide (Bulk) also accelerated by +92% MoM to take rank 1, whereas Marshmellow OG (1g) rose a modest +7% MoM yet stayed at rank 3. With nine of the top ten SKUs in Flower and two bulk entries inside the top four, the mix points to a pivot toward volume-oriented Flower that can scale velocity faster than single-gram items.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.