May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

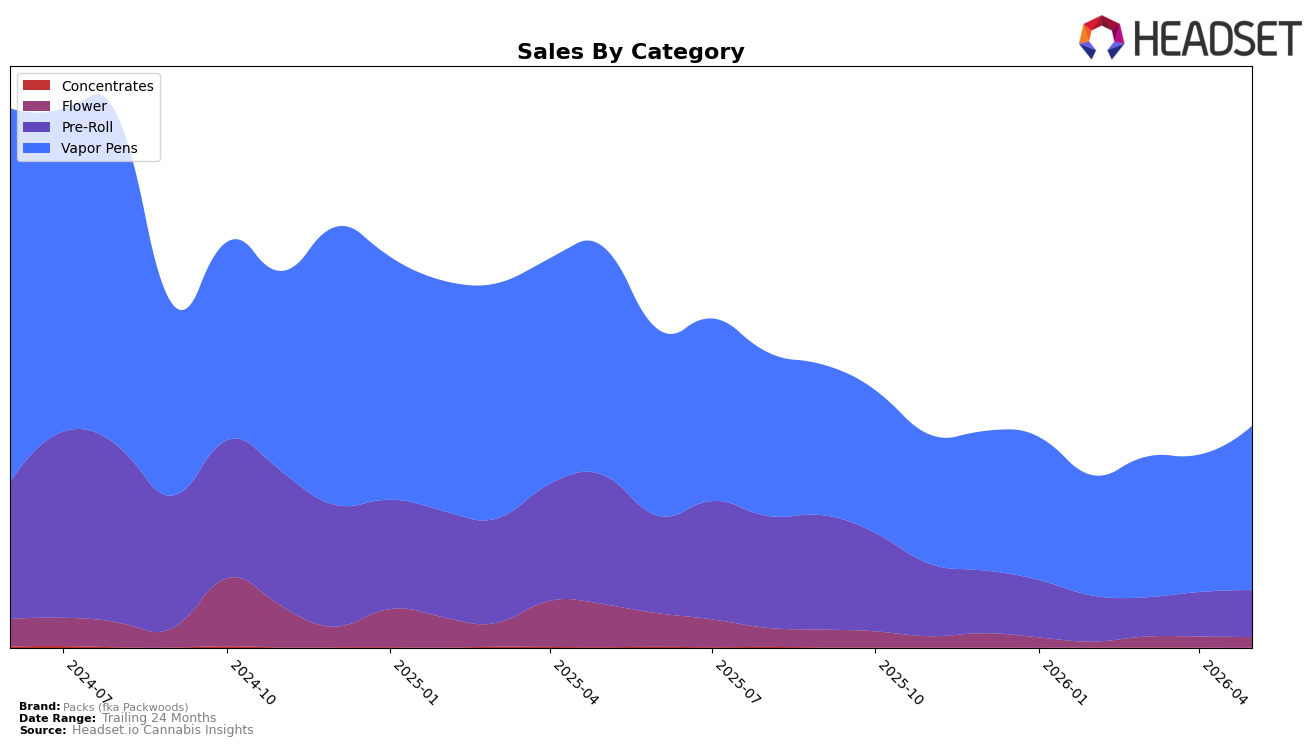

Packs (fka Packwoods) concentrated 74.25% of May-2026 sales in Vapor Pens, with Pre-Roll at 21.10% and Flower at 4.65%, indicating a heavier tilt toward inhalables as Vapor Pens grew 19.63% month over month while Pre-Roll rose 5.82% and Flower fell 4.99%. Year over year, the mix is under pressure across the board — Vapor Pens declined 28.06%, Pre-Roll dropped 63.73%, and Flower contracted 75.95% — while the brand’s average price fell 19.15%, implying a price-led defense that has not offset a total brand sales decline of 44.74% year over year; the pattern implies the brand is leaning into Vapor Pens momentum to stabilize volume even as legacy formats shrink.

With Vapor Pens ranked 11 in Colorado for May-2026 and commanding nearly three-quarters of brand sales, the tactical path is to defend and climb within that ranking while using the 19.63% month-over-month Vapor Pen growth to backfill the 63.73% Pre-Roll and 75.95% Flower annual drops. The 21.10% Pre-Roll share paired with a 5.82% month-over-month uptick suggests targeted SKU pruning rather than broad expansion, while the 4.65% Flower share and 4.99% month-over-month decline argue for exit-or-niche positioning; overall, the cross-category declines and 19.15% average price reset imply the brand’s near-term positioning is value-leaning within Vapor Pens to gain rank share, not breadth across categories.

Competitive Landscape

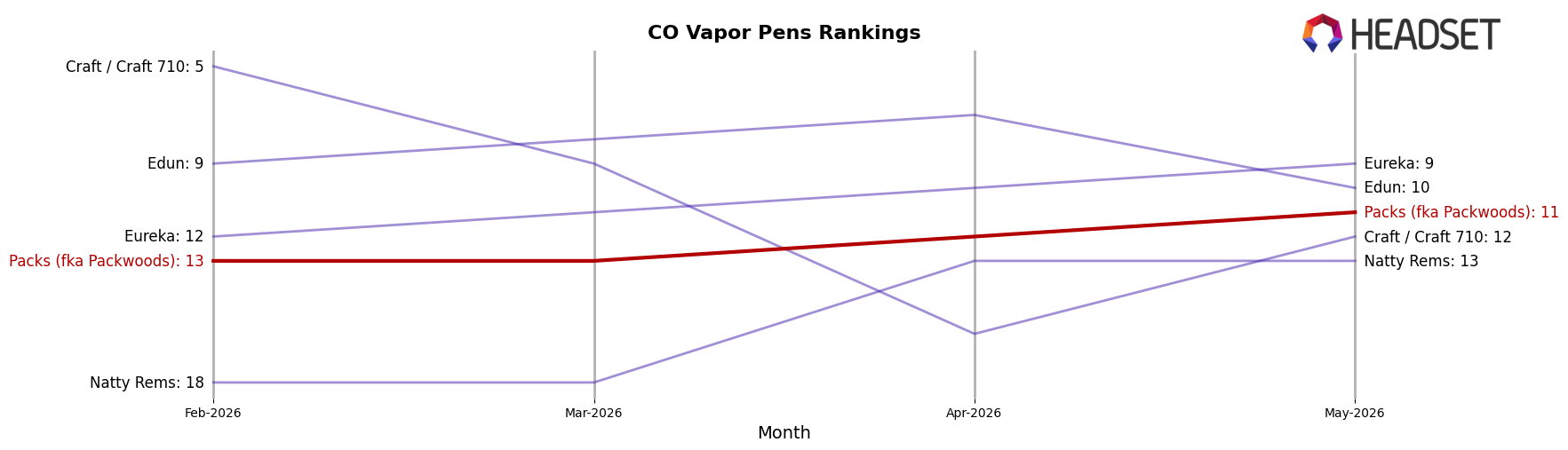

Packs (fka Packwoods) sits at rank #11 in CO Vapor Pens in May 2026, down 5 positions year over year from #6, while improving 2 spots versus February 2026 when it was #13; against a historical peak of #5 in July 2024, the brand is 6 ranks lower today. Competitively, Spherex held #1 year over year at #1 despite a -14.1% sales change, and PAX rose from #3 to #2 with +24.0% sales, indicating share consolidation above Packs, while Spectra jumped from #14 to #5 with +135.3% sales, widening the gap to the top 10. The pattern implies that despite a recent quarter-on-quarter rank lift, sustained displacement by faster-rising competitors reduces the likelihood of a near-term return to the July 2024 peak without a step-change in velocity.

Notable Products

Sour Gushers Live Resin Packspod Disposable (2g) posted the headline move in May 2026 with a 67.7% month-over-month surge to rank 3, while Blucifer Kush Live Resin Packspod Disposable (2g) followed with a 65.4% gain at rank 5, indicating demand is tilting toward higher-capacity 2g formats. Marshmallow Fluff Distillate Packspod Mini Disposable (1g) rose 21.1% to rank 1, yet the outsized gains clustered in the 2g line where three SKUs sit in the top 10 and one declined only 3.1% at rank 10, signaling share consolidation around larger carts. With eight of the top ten being Vapor Pens and multiple Live Resin variants rising 41.3% to 67.7%, the mix implies Packs (fka Packwoods) is migrating volume toward Live Resin-driven 2g SKUs while maintaining a flagship 1g anchor at the top.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.