Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

High Tech is stocked at 16 licensed dispensaries across Oregon, Colorado, and Maine, 12 of them in Oregon, with the deepest coverage in Eugene, Salem, Astoria, Aurora, and Cottage Grove. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

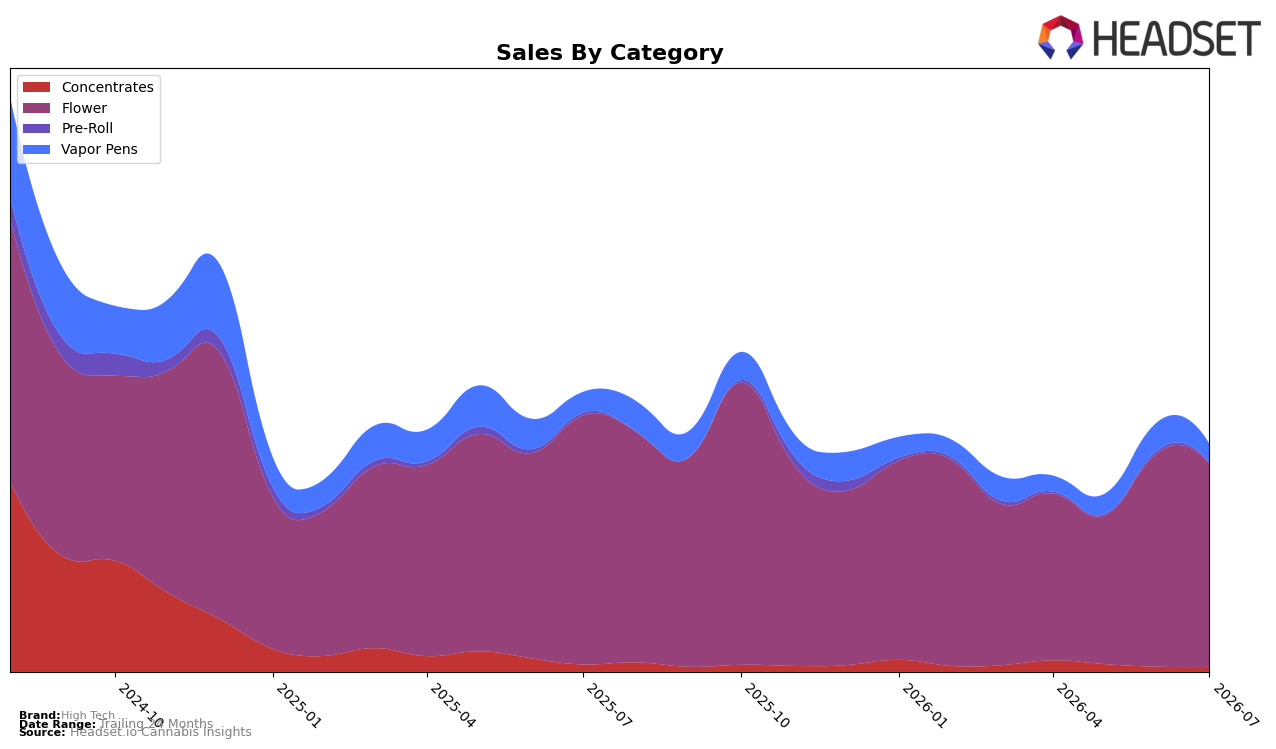

High Tech’s July 2026 mix concentrates in Flower at 89.26% share, with category sales down 18.51% year over year and 5.23% month over month, while Vapor Pens at 8.22% share fell 9.70% YoY and 33.53% MoM. Concentrates hold 2.12% share with a 33.45% YoY decline and a 1.97% MoM dip, and Pre-Roll sits at 0.40% share after a 61.68% YoY and 62.12% MoM contraction; average price rose 11.91% YoY even as total brand sales fell 18.61% YoY. With Flower ranked 11 in Oregon and the mix tilting further toward this single category while secondary formats retreat sharply, the pattern implies reliance on Flower breadth over multi-format balance.

The steep 33.53% MoM retreat in Vapor Pens alongside only a 5.23% MoM decline in Flower suggests consumer substitution into the core category rather than across formats, and the 11.91% YoY price increase paired with an 18.61% YoY sales decline indicates price elasticity weighing on non-Flower trial. With Flower at 89.26% share and rank 11 in Oregon, while Concentrates and Pre-Roll contract 33.45% and 61.68% YoY respectively, the positioning implication is a price-led, Flower-centric strategy that preserves rank stability in the core but narrows reach with heavier exposure to single-category volatility.

Competitive Landscape

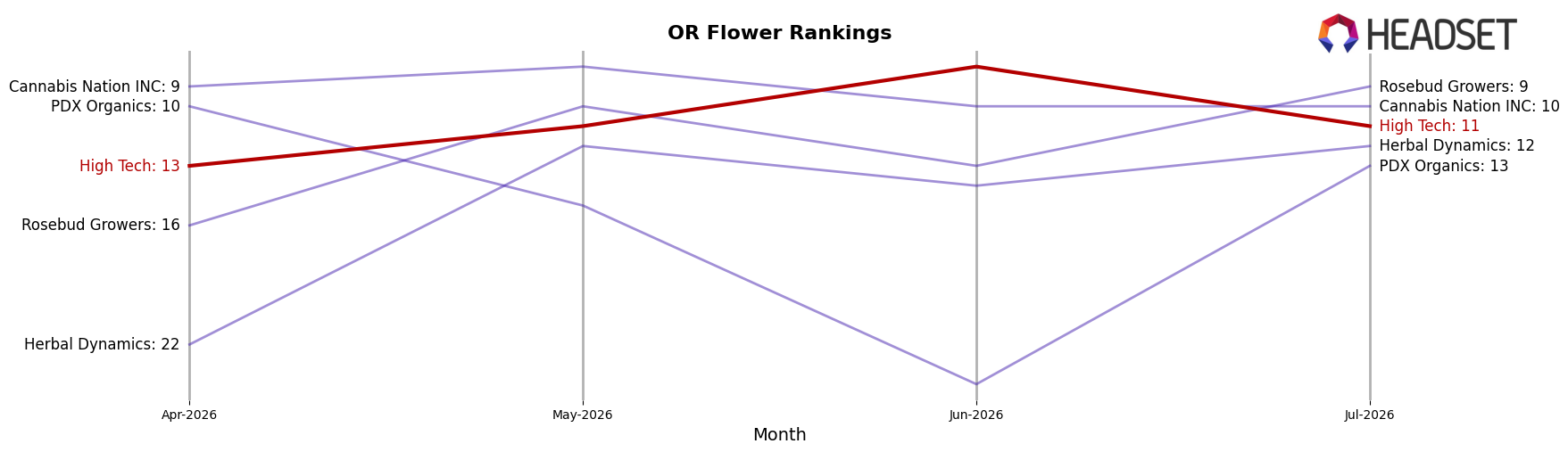

High Tech is ranked #11 in OR Flower in July 2026, down 5 positions year over year from #6, and 2 positions better than April 2026 when it sat at #13; its historical ceiling remains #3 from December 2024. In contrast, PRUF Cultivar / PRŪF Cultivar held #1 both this year and last (0-rank change) while reporting approximately 50.7% YoY sales growth, and Grown Rogue advanced from #3 to #2 alongside 53.5% YoY sales growth; meanwhile, Otis Garden surged from #12 to #4 with 86.2% YoY sales growth, outpacing Bald Peak, which slipped from #2 to #5 on a 15.5% YoY sales decline. The combination of a 5-place YoY slide to #11 and peers moving up 1–8 ranks implies High Tech’s trajectory is toward the middle of the pack unless it reclaims the velocity that previously pushed it to #3.

Notable Products

The steepest move in July 2026 was Gasper (3.5g) plunging 52.6% month over month to rank 6, while Pink Rozay (3.5g) fell 19.8% at rank 3, indicating demand is rotating away from certain eighths even as category leaders hold share. Countering the retreat, Blumosa (Bulk) jumped 32.6% to rank 1, and together with Blumosa (3.5g) at rank 3 this points to a tiered Blumosa ladder gaining traction as other Flower SKUs contract. With eight of the top ten products in Flower and only one Pre-Roll present, assortment is consolidating around larger Flower formats despite volatility in specific strains. The mix implies High Tech is leaning into a Blumosa-led Flower core and needs to rebalance underperforming eighths to sustain rank stability and margin, rather than chase breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.