Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

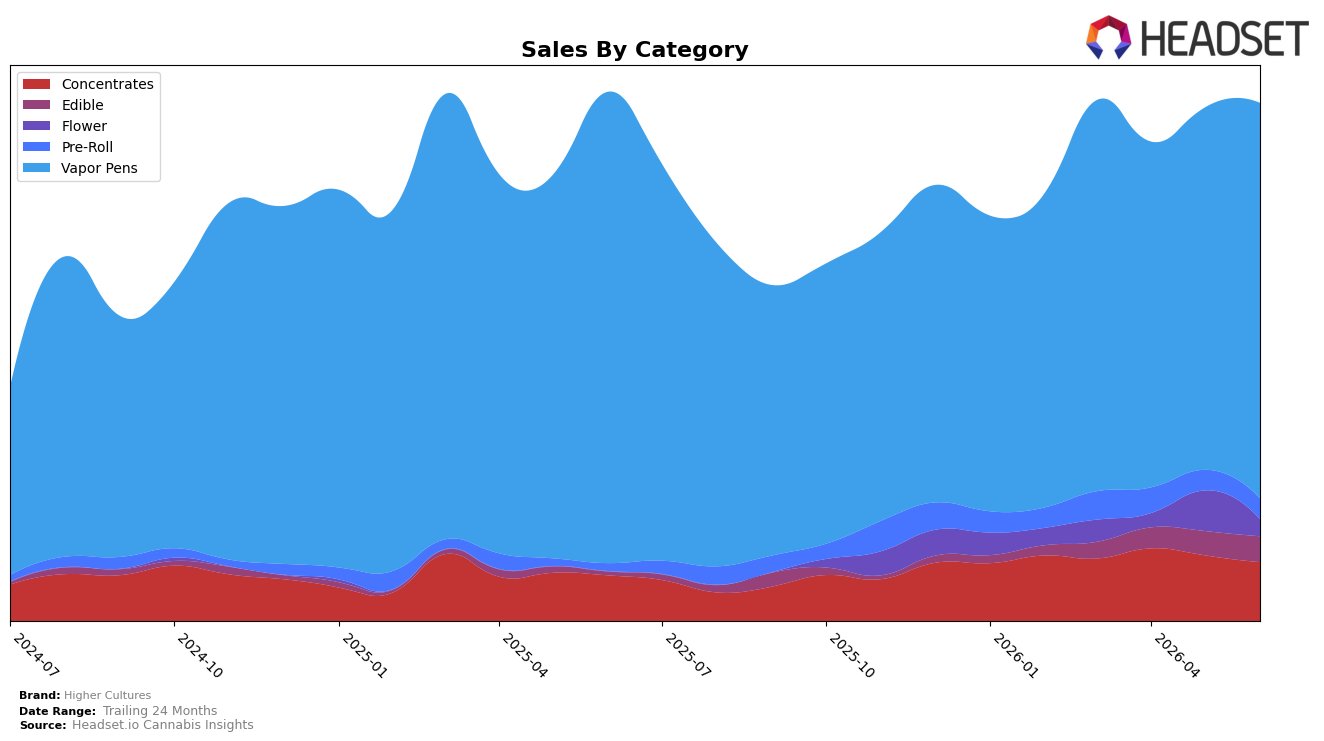

In June 2026, Higher Cultures remained concentrated in Vapor Pens at 76.55% share, while that category declined year over year by 16.16% but grew month over month by 9.14%; in contrast, Concentrates held 11.32% share with a 29.37% YoY increase but a 10.49% MoM decline. Edible expanded to 4.92% share on a 646.45% YoY surge and a 6.56% MoM gain, and Pre-Roll reached 3.97% share with 175.10% YoY growth and 1.84% MoM growth, whereas Flower slipped to 3.23% share with a 58.40% MoM drop. With overall brand sales down 2.11% YoY alongside a 25.30% YoY price decrease to an average of $16.60, the pattern implies a deliberate pivot from a contracting core (Vapor Pens) toward faster-growing adjacencies (Edible, Pre-Roll) to stabilize volumes despite pricing pressure.

The mix shift implies positioning risk and opportunity: reliance on Vapor Pens at rank 9 in Oregon limits upside if category headwinds persist, while triple-digit YoY growth in Edible (646.45%) and Pre-Roll (175.10%) can diversify revenue if sustained. However, Concentrates’ 29.37% YoY growth paired with a 10.49% MoM pullback, and Flower’s 58.40% MoM contraction, indicate near-term volatility that could be buffered by maintaining Vapor Pens’ 9-rank presence while selectively scaling Edible’s 6.56% MoM momentum; the thesis is that controlled expansion in high-growth minors can offset category cyclicality without overexposing the portfolio to short-term swings.

Competitive Landscape

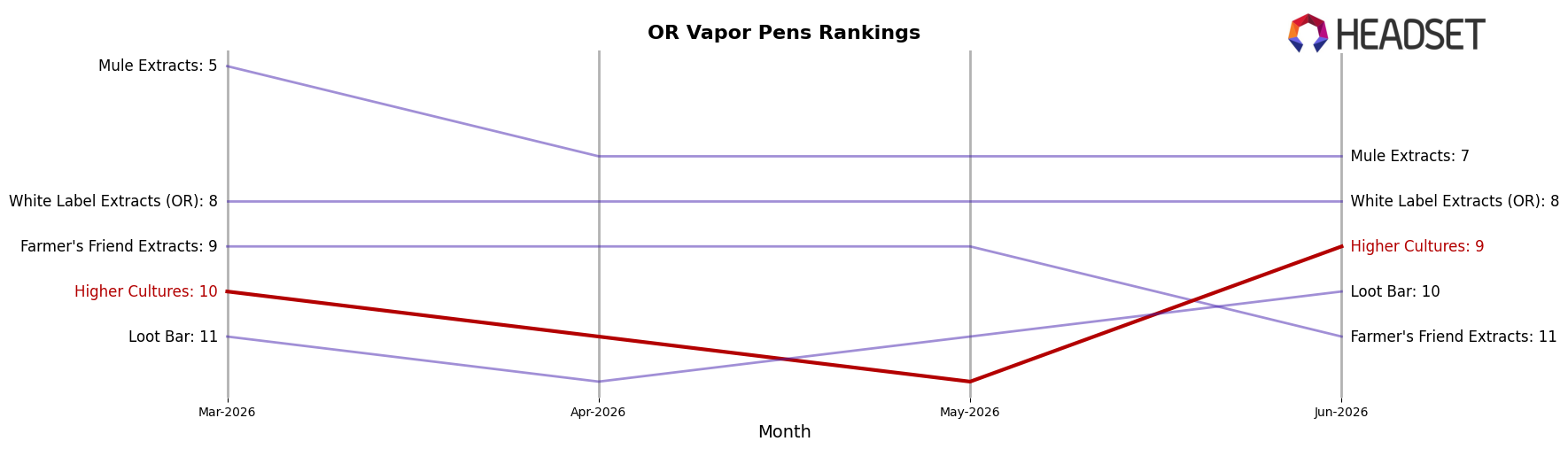

Higher Cultures is ranked #9 in OR Vapor Pens in June 2026, down 3 positions year over year from #6, and up 1 spot versus March 2026 when it sat at #10; this places the brand three ranks below its June 2025 peak of #6 while the category’s top tier has been volatile, as FRESHY climbed from #5 to #2 and Entourage Cannabis / CBDiscovery fell from #1 to #3 alongside a 38.9% sales decline, while Buddies advanced from #2 to #1. The pattern—slipping 3 ranks year over year but edging up 1 rank in the last three months amid competitors moving 3 to 4 places—implies Higher Cultures is stabilizing below the leadership cluster and must outpace mid-pack risers to regain a top-6 trajectory.

Notable Products

Kiwi Limeade Gummies 10-Pack (100mg) posted the steepest shift in June 2026 with a -44.5% month-over-month decline while sliding to rank 10, and Indica Puffberry Gummies 10-Pack (100mg) fell -31.5% at rank 8, signaling an Edibles pullback even as Yumberry High Dose Gemmies 10-Pack (100mg) was essentially flat at +0.1% at rank 3. Alley Oop (Bulk) in Flower rose +9.2% to hold rank 1, but the Edibles category still occupies four of the top ten slots, indicating breadth without momentum. With Vapor Pens anchored mid-table at ranks 5, 7, and 9 and no month-over-month increases reported there, the mix points to reliance on stable Flower leadership while Edibles volatility compresses near-term upsell potential despite a $38,281 Vapor Pens single-SKU revenue signal.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.