Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Verdant Leaf Farms is stocked at 168 licensed dispensaries across Oregon and Michigan, 167 of them in Oregon, with the deepest coverage in Portland, Eugene, Salem, Bend, and Corvallis. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

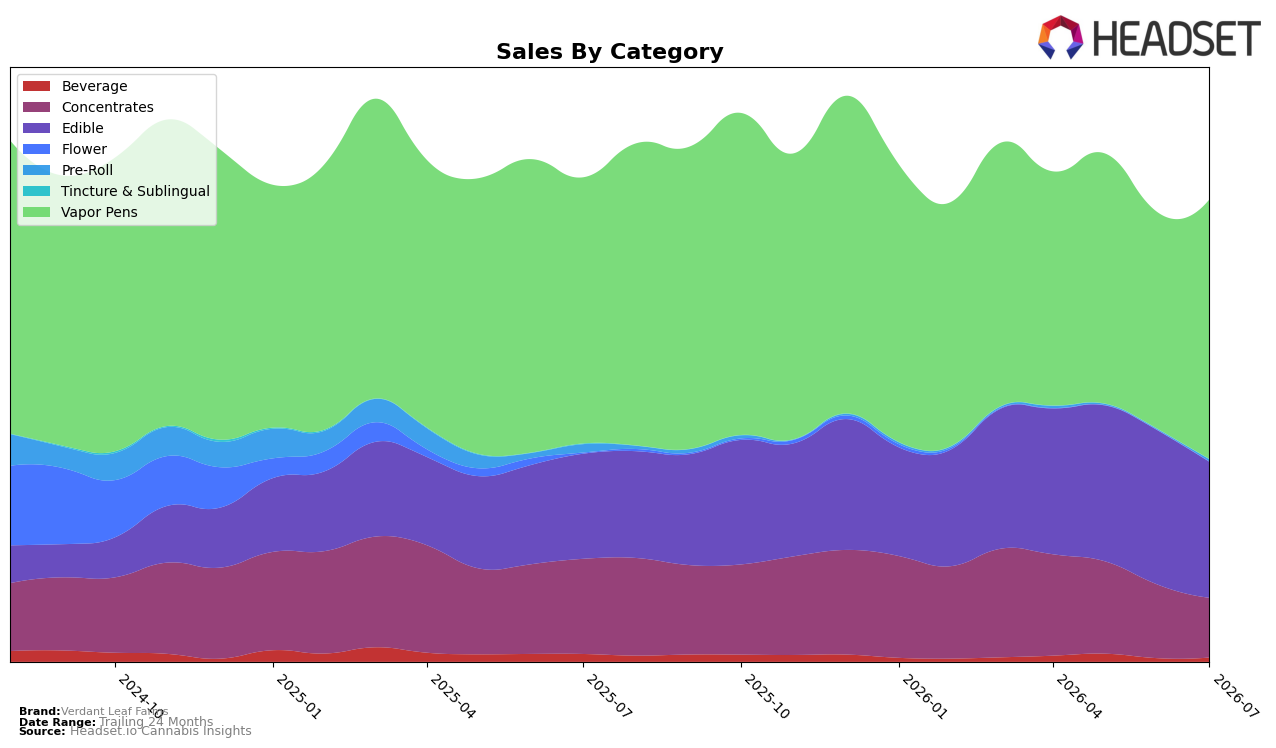

Verdant Leaf Farms concentrated 56.34% of July 2026 sales in Vapor Pens with a 19.96% month-over-month lift but a 2.45% year-over-year decline, while Edible held 29.46% share with a 29.45% year-over-year increase offset by an 11.85% month-over-month drop; this mix change raises reliance on two categories moving in opposite monthly directions. Concentrates fell to 12.91% share with a 37.35% year-over-year decline and an 18.77% month-over-month slide, and Beverage remained under 1.00% share despite a 20.34% month-over-month increase and a 46.58% year-over-year decline; together with a Pre-Roll rebound of 236.30% month-over-month from a low 0.41% share and a 76.70% year-over-year drop, the pattern implies defensive stabilization via Vapor Pens momentum while long-term category attrition limits aggregate growth.

Positioning now skews toward higher-ticket inhalables: Vapor Pens averaged $17.83 versus the brand’s overall $11.21, and Concentrates averaged $19.18 despite steep volume pressure, while Edible averaged $5.91 and lost 11.85% month-over-month share contribution; this price tiering suggests margin mix depends on sustaining Vapor Pens velocity. With a July 2026 rank of 17 in Vapor Pens in Oregon and a 3.75% year-over-year average price decrease alongside a 2.45% Vapor Pens sales decline year-over-year, the implied strategy is to lean on price-accessible cart offerings to protect rank while reallocating away from structurally declining Concentrates and Beverage where year-over-year drops of 37.35% and 46.58% point to weak repeat pull.

Competitive Landscape

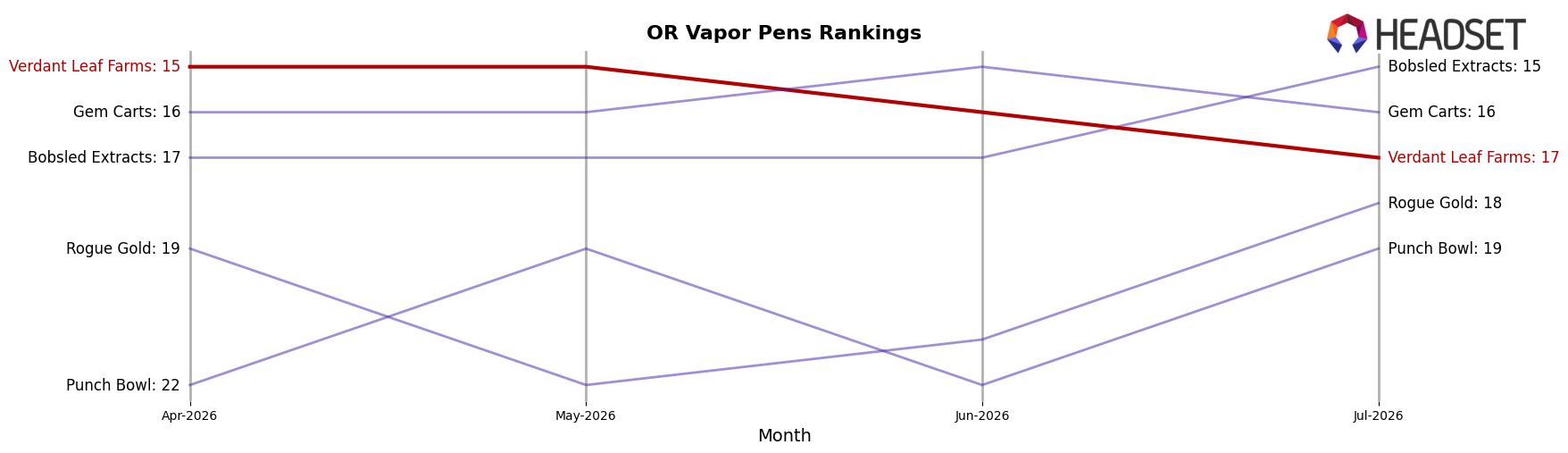

Verdant Leaf Farms sits at rank #17 in OR Vapor Pens in July 2026, down 1 position from #16 year over year and 2 positions from #15 in April 2026, after previously peaking at #13 in December 2025; meanwhile, Buddies moved from #2 to #1 with 17.3% YoY sales growth and Entourage Cannabis / CBDiscovery slipped from #1 to #2 on a 33.4% YoY sales decline, indicating that Verdant Leaf Farms’ slight rank erosion alongside leadership churn at the top implies share is consolidating around rising leaders while mid-tier brands face incremental pressure to regain momentum.

Notable Products

There were no month-over-month moves above +50% or below -10% in July 2026, so the clearest signal comes from concentration: five of the top ten are Edible SKUs, led by Pink Lemonade x Government Oasis Live Rosin Nanotech Gummy (100mg) at rank 1 with +22.8% MoM, while Blue Raspberry Hash Rosin Nanotech Gummy (100mg) climbed to rank 3 with +24.1% MoM. Cherry Live Rosin Gummy (100mg) held rank 2 with a modest +4.4% MoM, and GMO Live Rosin Nano Infused Single Gummy (100mg) slipped to rank 10 at -1.5% MoM. This tilt toward Edibles at ranks 1–5 signals Verdant Leaf Farms is consolidating demand in solventless gummy formats, implying further emphasis on flavor-extension and dosage variants over expanding other form factors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.