Apr-2026

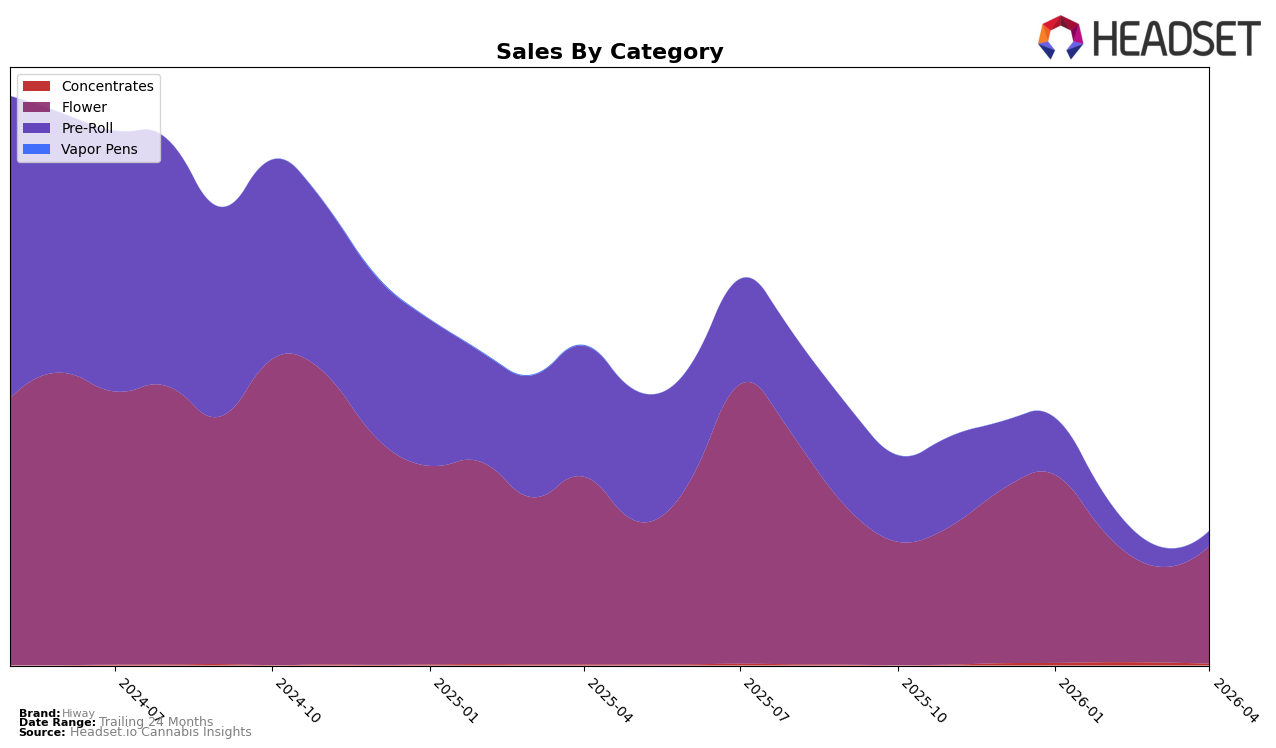

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

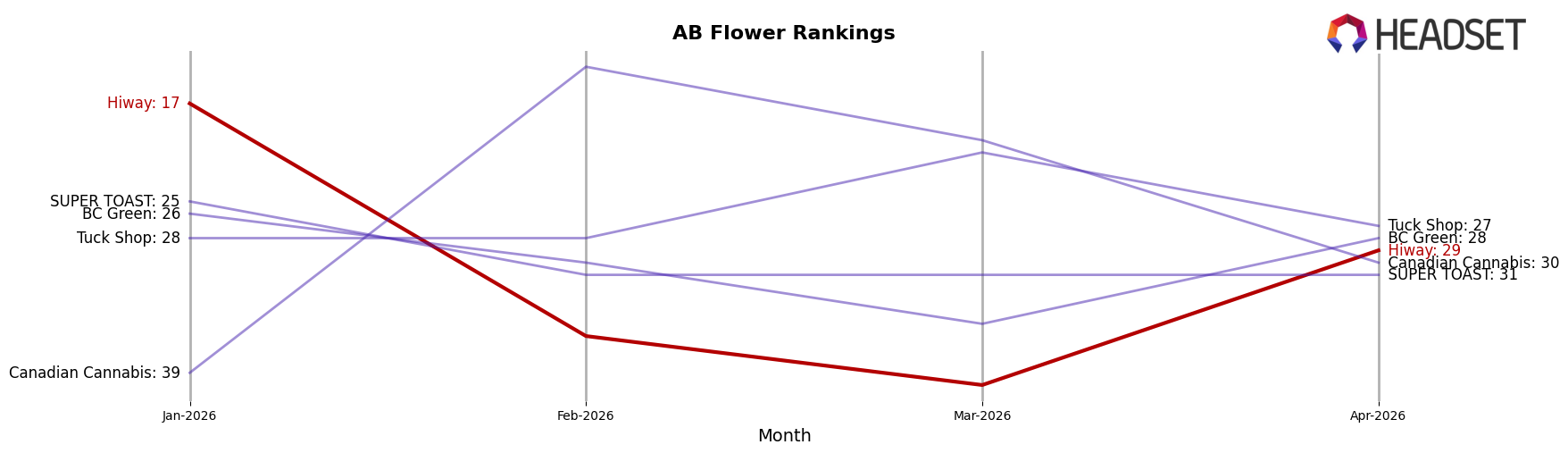

In the province of Alberta, Hiway has shown some fluctuations in the Flower category rankings. Starting the year strong at 17th position in January, Hiway experienced a dip in the subsequent months, falling out of the top 30 in February and March, before climbing back to 29th in April. This resurgence in April is noteworthy and suggests a potential strategy shift or market adaptation by Hiway. However, in the Pre-Roll category, Hiway struggled to maintain a presence, ranking 49th in January and dropping out of the top 30 by February. This decline indicates challenges in this segment, possibly due to increased competition or changing consumer preferences.

In British Columbia, Hiway's performance in the Flower category has been inconsistent, with rankings fluctuating between 45th and 65th over the first four months of 2026. Despite this, the brand managed to improve its position from March to April, moving from 65th to 46th. This positive movement might indicate a recovery phase or a successful promotional effort. Meanwhile, in Ontario, Hiway's presence in the Flower category dwindled, with rankings slipping from 82nd in January to falling out of the top 30 by April. This decline could be attributed to intensified competition or market dynamics that favored other brands. Additionally, in Saskatchewan, Hiway made a brief appearance in the Flower category rankings at 47th in January, but did not maintain a top 30 position in the following months, highlighting potential market penetration challenges in this region.

Competitive Landscape

In the Alberta flower category, Hiway experienced notable fluctuations in its competitive standing from January to April 2026. Starting at rank 17 in January, Hiway saw a decline, dropping out of the top 20 in February and March, before recovering to rank 29 in April. This recovery coincides with a sales increase from March to April, suggesting a positive response to market strategies or product adjustments. In contrast, BC Green maintained a more stable trajectory, consistently ranking around the mid-20s, and even surpassing Hiway in April. Tuck Shop also showed resilience, improving its rank from 28 in January to 27 in April, with a significant sales peak in March. Meanwhile, Canadian Cannabis demonstrated a volatile pattern, peaking at rank 14 in February but dropping to 30 by April. These dynamics highlight the competitive pressures Hiway faces and underscore the importance of strategic positioning to regain and sustain higher rankings in the Alberta flower market.

Notable Products

In April 2026, the top-performing product from Hiway was the Sativa Pre-Roll 2-Pack (2g) maintaining its first-place rank consistently since January, despite a decrease in sales to 2739 units. Fast Lane Sativa (28g) rose to second place from third in March, showing a notable increase in sales. Indica Pre-Roll 2-Pack (2g) slipped to third place from its consistent second-place ranking in the previous months. Slow Lane Indica (28g) held steady in fourth place, demonstrating stability in its sales performance. Fast Lane Sativa (14g) entered the rankings in fifth place, marking its presence with a notable sales figure of 1040 units.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.