Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

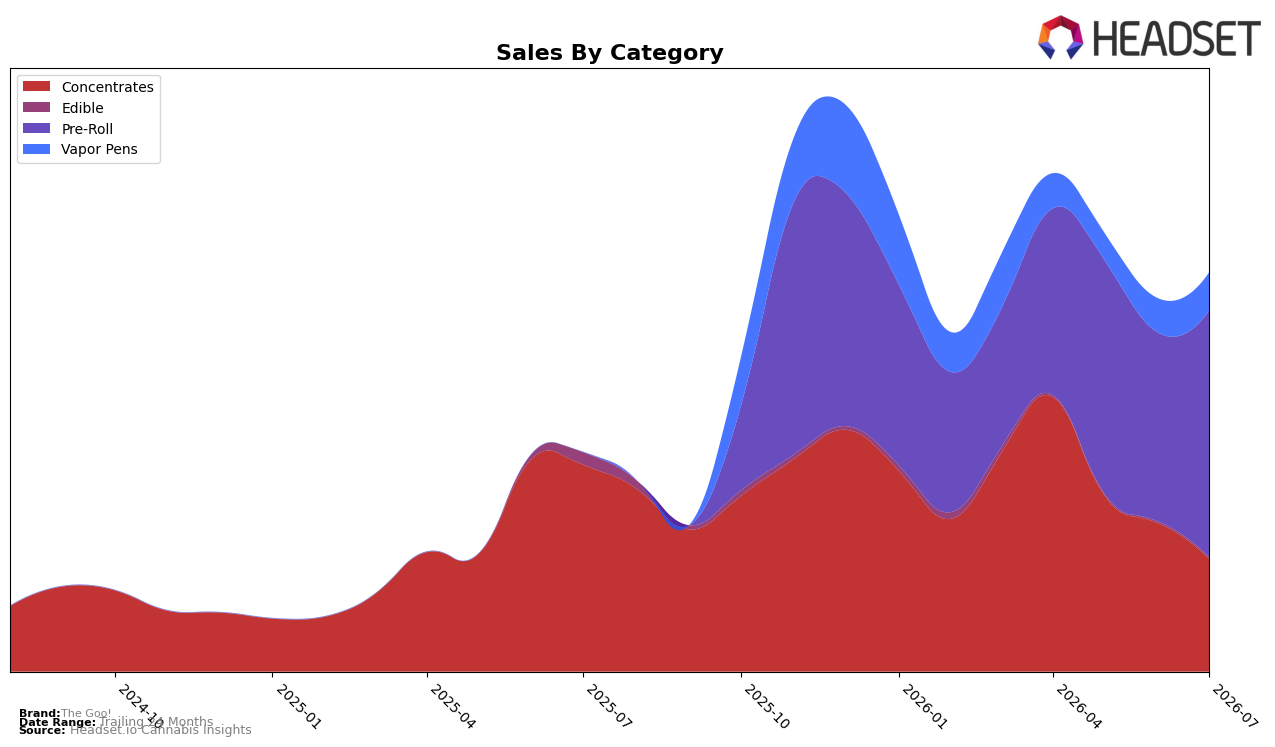

In July 2026, The Goo! concentrated 61.88% of sales in Pre-Roll while Vapor Pens reached 9.48% share, indicating mix consolidation even as Concentrates fell to 28.27% share. Month over month, Pre-Roll expanded 30.61% and Vapor Pens rose 11.09%, while Concentrates contracted 24.13% and Edible slipped 3.56%; year over year, Concentrates declined 45.56% and Edible dropped 88.12%. With brand-level average price down 7.69% and Pre-Roll average price at 25.76 relative to Vapor Pens at 35.71, the mix tilt combined with July 2026 Pre-Roll category rank of 48 in Alberta implies The Goo! is leaning into volume-accretive segments to offset price compression.

The pivot toward Pre-Roll and a smaller but growing Vapor Pens footprint suggests a bid for broader basket reach, as the 30.61% MoM gain in Pre-Roll alongside a 24.13% MoM pullback in Concentrates reweights revenue toward faster-turn SKUs. Given the 45.56% YoY decline in Concentrates and the 88.12% YoY decline in Edible, the current mix positions The Goo! to prioritize shelf presence and trial over premium ticket, which aligns with a 7.69% average price decrease and a mid-pack rank of 48 that signal a need to trade up within the category ladder while sustaining share through value-led formats.

Competitive Landscape

The Goo! sits at #48 in AB Pre-Roll in July 2026, improving 8 ranks from #56 three months prior, while still trailing its #42 peak from November 2025; this contrasts with General Admission holding #1 despite a -14.5% YoY sales change and Back Forty / Back 40 Cannabis advancing to #2 with a +6 rank YoY gain and +34.3% sales YoY. Meanwhile, Space Race Cannabis stays at #3 with a -37.9% sales YoY decline and Thumbs Up Brand surged to #5 with a +19 rank YoY climb and +138.3% sales YoY, indicating that recent upward movement for The Goo! is occurring amid volatile leader dynamics and accelerating mid-pack mobility; the trajectory implies a recovery path is open but requires sustained share capture to surpass the #42 prior ceiling.

Notable Products

It Came From The Kush Live Rosin Infused Pre-Roll 3-Pack (1.5g) led July 2026 with a +51.6% month-over-month surge to rank 1, while Brain Fruit Live Rosin Infused Pre-Roll 3-Pack (1.5g) fell -17.1% to rank 3. Four of the top ten are Pre-Roll SKUs, and within that cluster Goobies! Live Rosin Infused Pre-Roll 3-Pack (1.5g) declined -25.3% at rank 4 versus Earthquake Infused Pre-Roll 3-Pack (1.5g) gaining +44.0% at rank 2. The split between a +51.6% leader and a -25.3% laggard inside the same format implies the brand is concentrating demand behind a few standout infused SKUs rather than lifting the entire Pre-Roll portfolio.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.