Apr-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

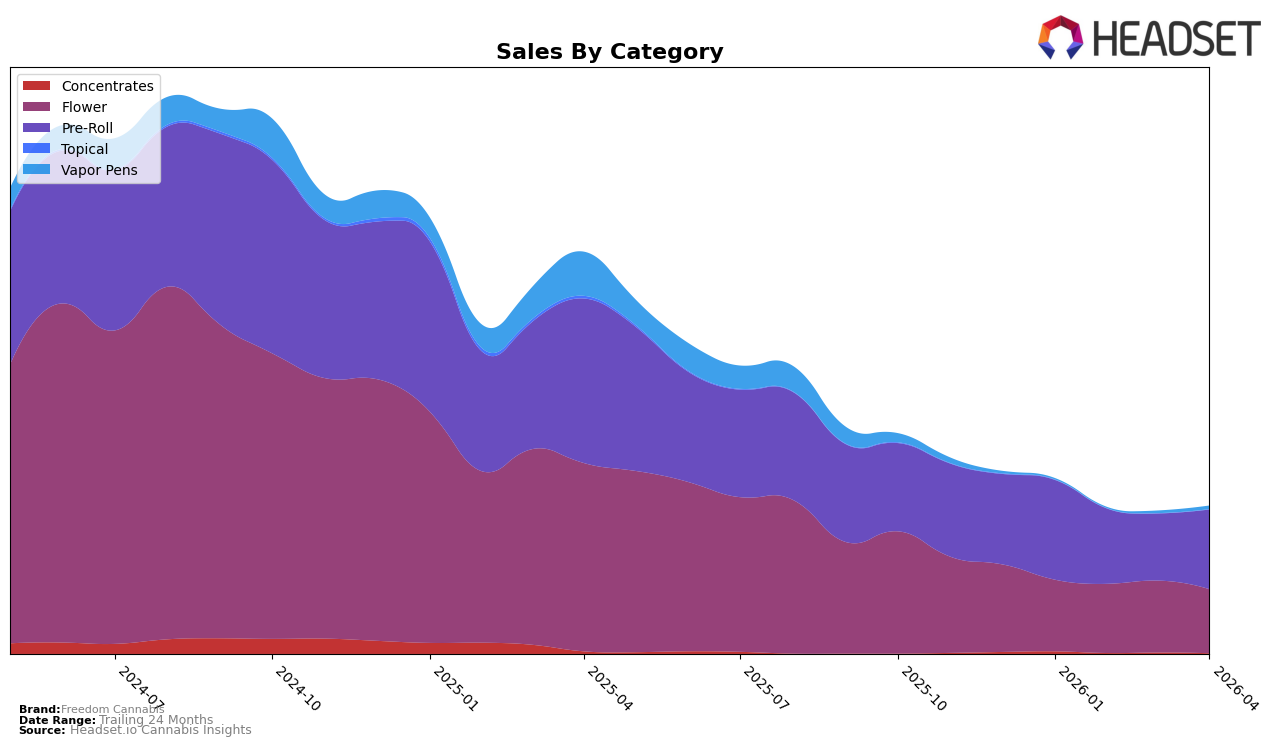

Market Insights Snapshot

Freedom Cannabis has shown varied performance across different categories and regions, with notable trends in certain areas. In the Alberta market, the brand's Flower category experienced a modest upward trend in rankings, moving from 44th place in January 2026 to 35th by April 2026. This improvement is mirrored by a steady increase in sales, indicating a growing consumer preference for their Flower products in this region. However, the brand's Pre-Roll category in Alberta presents a more fluctuating pattern, where it ranked 33rd in January, dropped to 42nd in March, and then climbed back to 38th in April. This inconsistency suggests a competitive landscape in the Pre-Roll category, though the recovery in April could imply strategic adjustments or shifts in consumer interest.

In contrast, the performance of Freedom Cannabis in Saskatchewan reveals challenges, particularly in the Flower category. The brand's ranking fell steadily from 43rd in January to 52nd in March, and by April, it did not appear in the top 30, indicating a significant decline in market presence. This drop is accompanied by a notable decrease in sales figures, which may reflect either increased competition or changing consumer preferences in Saskatchewan. The absence from the top 30 in April could be a concerning indicator for the brand's market strategy in this region, highlighting the need for potential reevaluation to regain traction.

Competitive Landscape

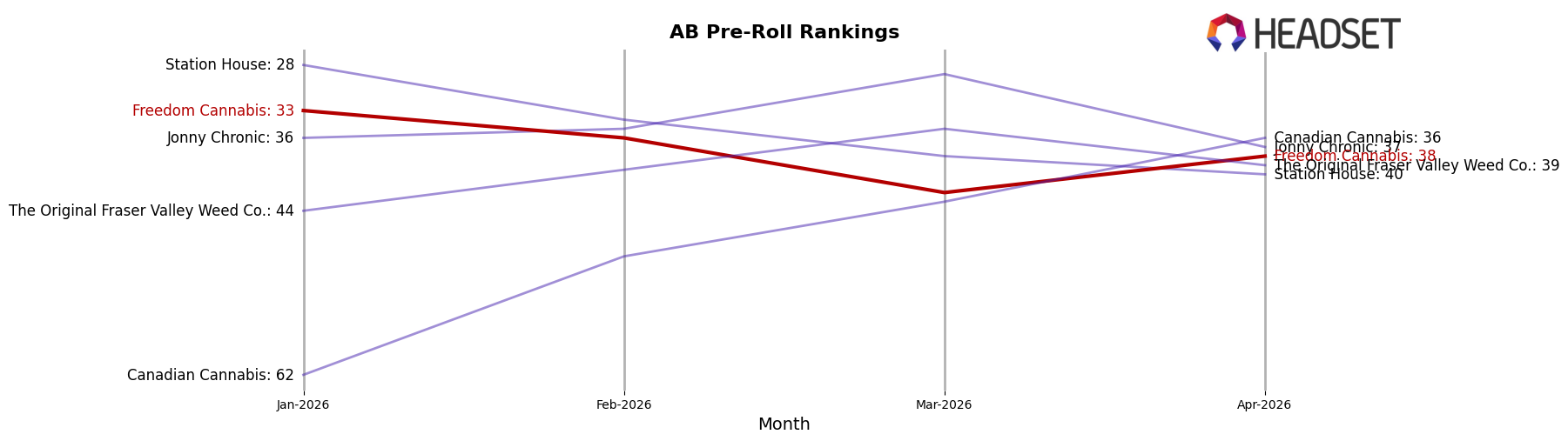

In the competitive landscape of pre-rolls in Alberta, Freedom Cannabis has experienced notable fluctuations in its market position from January to April 2026. Starting at rank 33 in January, Freedom Cannabis saw a decline to rank 42 in March before recovering slightly to rank 38 in April. This period of volatility contrasts with the performance of other brands such as Jonny Chronic, which maintained a relatively stable presence, peaking at rank 29 in March. Meanwhile, Station House experienced a downward trend, dropping to rank 40 by April. Interestingly, Canadian Cannabis showed a significant upward trajectory, climbing from rank 62 in January to surpass Freedom Cannabis at rank 36 in April. The dynamic shifts in rankings highlight the competitive pressures Freedom Cannabis faces, emphasizing the need for strategic adjustments to regain and sustain higher market positions in Alberta's pre-roll category.

Notable Products

In April 2026, Mango Haze Pre-Roll 2-Pack (2g) retained its top position as the leading product for Freedom Cannabis, with impressive sales of 3059 units. Double Double Medium Pre-Roll 10-Pack (5g) maintained its consistent performance, holding the second rank with a slight increase in sales compared to March. Lemon Hedz Pre-Roll 2-Pack (2g) saw a decline in ranking, moving from the top spot in January and February to third place in April. Happy Hour Special Pre-Roll 2-Pack (2g) improved its position from fifth in March to fourth in April, indicating a positive sales trend. Pink OG Pre-Roll 2-Pack (2g) re-entered the top five, ranking fifth in April after being unranked in March, suggesting a resurgence in popularity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.