Mar-2026

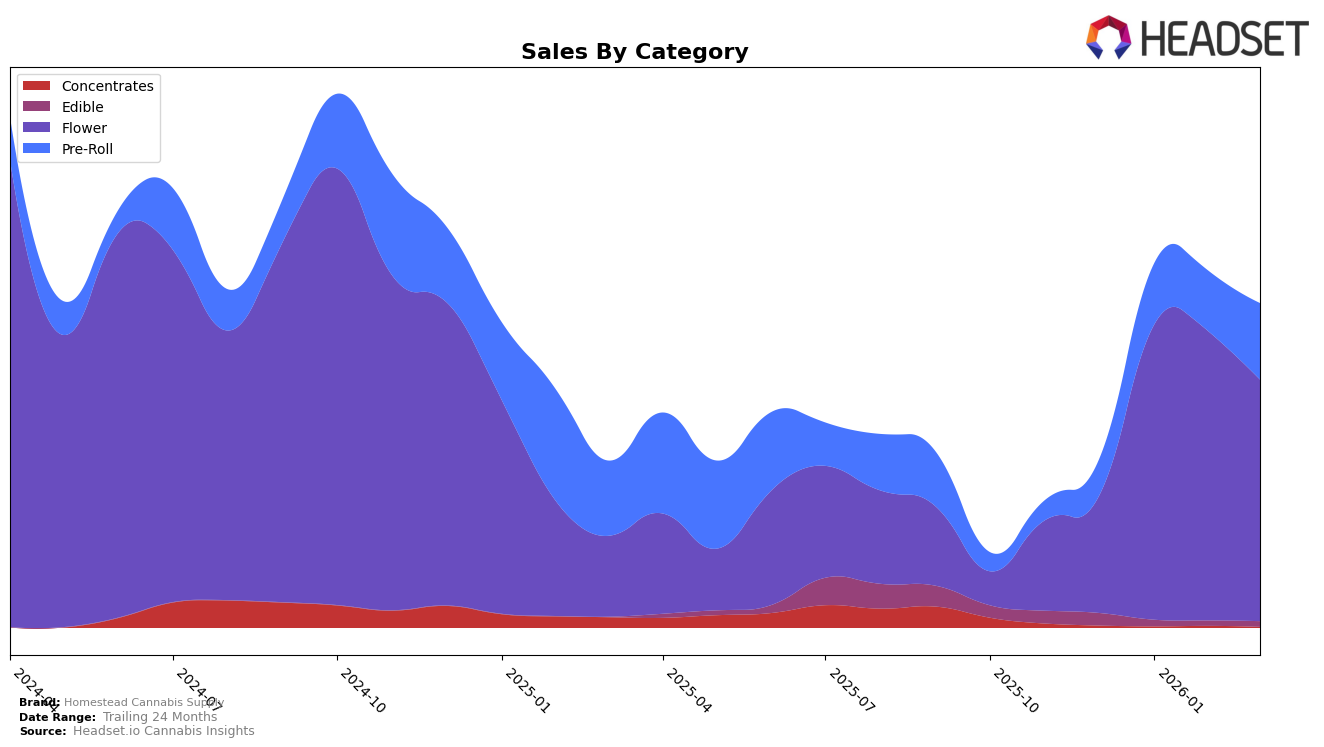

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

In the province of British Columbia, Homestead Cannabis Supply has shown a notable performance in the Flower category. Starting from a rank of 59 in December 2025, the brand made a significant leap to rank 22 in January 2026, before slightly declining to ranks 23 and 26 in the subsequent months. This upward trend in early 2026 indicates a strong market presence and consumer preference for their products in this category. Conversely, in the Pre-Roll category, Homestead Cannabis Supply was not in the top 30 in December but managed to secure ranks 85, 77, and 74 in the first three months of 2026, reflecting a gradual improvement in their standings.

In Ontario, the performance of Homestead Cannabis Supply appears more varied across categories. The brand was ranked 30th in the Edible category in December 2025, but it did not appear in the top 30 in the following months, suggesting a potential decline in market competitiveness or shifts in consumer preferences. In contrast, the Flower category saw the brand entering at rank 99 in March 2026, indicating a late but emerging presence in this segment. Such movements highlight the brand's fluctuating performance across different product lines and regions, suggesting areas of strength and opportunities for growth.

Competitive Landscape

In the competitive landscape of the flower category in British Columbia, Homestead Cannabis Supply has shown notable fluctuations in its market position from December 2025 to March 2026. Initially ranked at 59th place in December 2025, Homestead made a significant leap to 22nd in January 2026, indicating a strong surge in sales and market presence. However, this momentum slightly waned as it settled at 26th by March 2026. In comparison, Good Buds demonstrated a steady climb from 57th to 25th, surpassing Homestead by March. Meanwhile, Highly Dutch experienced a volatile trajectory, dropping from 27th in December to 35th in January, then rising to 18th in February before falling back to 24th in March, consistently outperforming Homestead in terms of rank. Magi Cannabis and BC 1/4 maintained more stable positions, with Magi Cannabis ending at 28th and BC 1/4 at 27th in March, both slightly ahead of Homestead. These dynamics suggest that while Homestead Cannabis Supply has made significant strides, it faces stiff competition from brands like Good Buds and Highly Dutch, which have shown stronger upward trends in recent months.

Notable Products

In March 2026, the top-performing product for Homestead Cannabis Supply was the Sativa Cherry Gummy (10mg) in the Edible category, maintaining its leading position from January 2026 with sales reaching 1,193 units. Following closely was Bandwagon Indica (7g) in the Flower category, which slipped to second place from its top spot in February. Bandwagon Sativa (7g), also in the Flower category, improved its ranking to third, up from fourth in February. The Indica Triple Berry Resin Gummy (10mg) dropped to fourth place, continuing its decline from the top spot in December 2025. Lastly, the new entry Bandwagon (7g) held steady in fifth place since its introduction in February 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.