Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

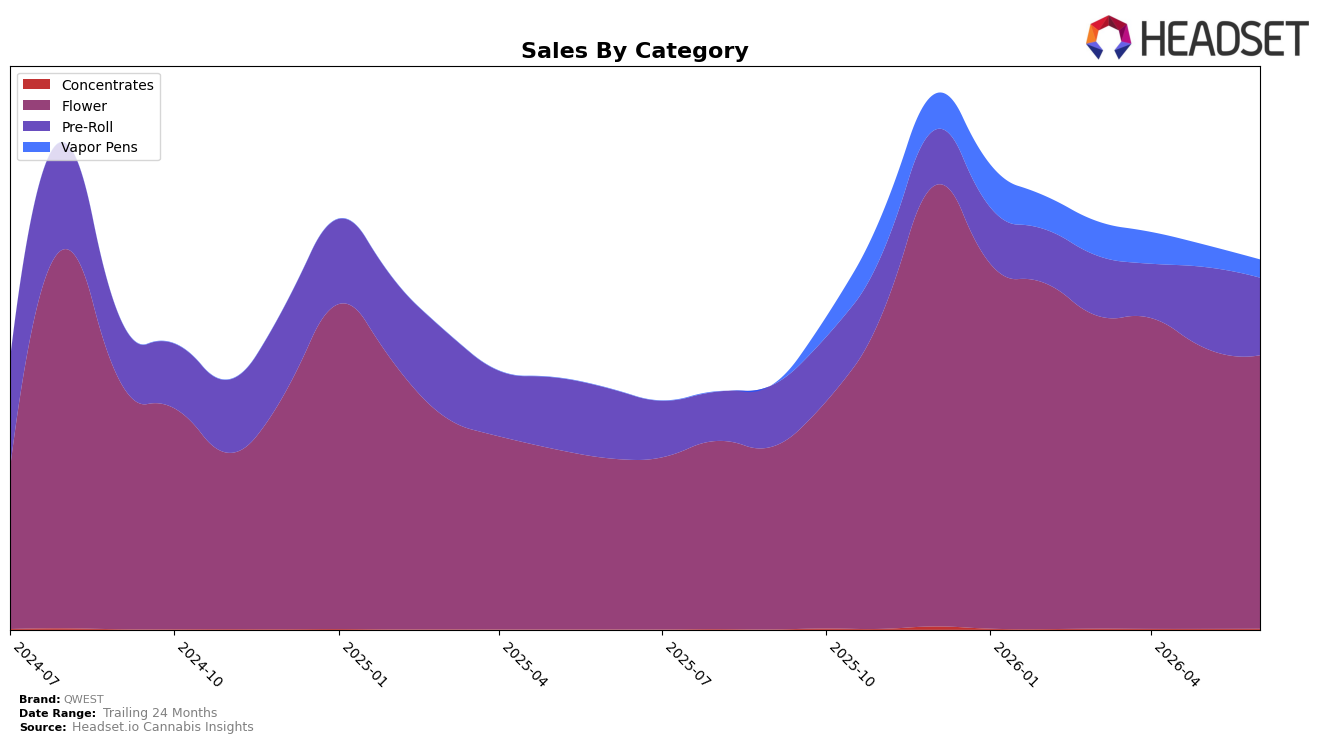

In June 2026, QWEST concentrated 74.05% of sales in Flower with 59.92% year-over-year growth but a 2.67% month-over-month dip, while Pre-Roll held 20.92% share with 10.89% year-over-year growth and a 4.12% month-over-month decline; Vapor Pens carried 4.85% share with an 18.52% month-over-month drop and no year-over-year comps, and Concentrates were 0.18% share with a 23.48% month-over-month rise from a small base. The brand’s overall sales grew 53.44% year over year alongside a 2.70% year-over-year decrease in average price to $32.35, and Flower’s average price at 40.99 outpaced the brand average, implying mix-up within Flower even as Pre-Roll at 17.98 pulled basket price down. The pattern implies QWEST is leaning further into premium-priced Flower to drive most of the year-over-year lift while absorbing tactical price pressure and seasonal softness in Pre-Roll and Vapor Pens.

Positioning-wise, the 10th rank in Flower in Saskatchewan sets a mid-tier anchor despite Flower holding nearly three-quarters of mix and growing 59.92% year over year, while the 4.12% month-over-month contraction in Pre-Roll and the 18.52% month-over-month slide in Vapor Pens suggest QWEST’s demand is less elastic outside Flower. With Concentrates up 23.48% month over month but only 0.18% share, the incremental lift is too small to offset soft Vapor Pens, and the 2.67% month-over-month Flower dip indicates near-term volatility even within the lead category. The implication is that QWEST’s defensible edge is concentrated in Flower, and maintaining or improving rank will likely depend on reinforcing Flower assortment and price-value tiers while using Pre-Roll and Concentrates surgically to stabilize month-over-month swings.

Competitive Landscape

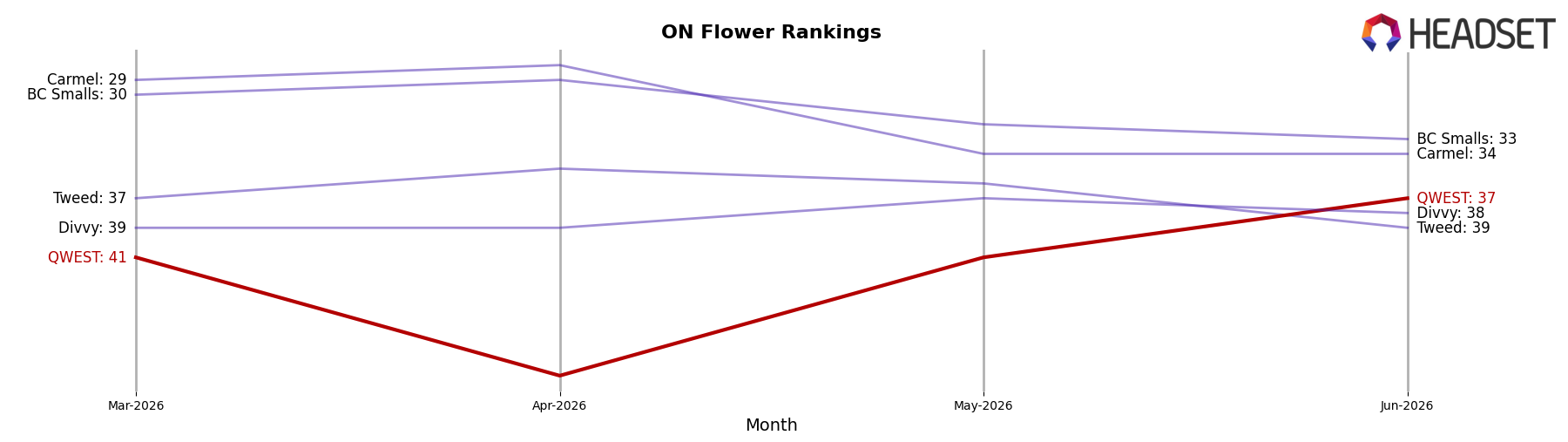

QWEST sits at rank #37 in Ontario Flower in June 2026, improving 24 places from #61 year over year and edging up 4 spots from #41 in March 2026, marking a new peak rank at #37 in June 2026 and breaking prior ceiling by 4 ranks over three months; meanwhile, Spinach climbed from #4 to #1 with a 38.3% year-over-year sales lift while Back Forty / Back 40 Cannabis slipped from #1 to #4 alongside an 11.3% sales decline, indicating QWEST’s movement is occurring amid leadership turnover and mixed competitor momentum; taken together, rank improvement from #61 to #37 while leaders diverge on sales trends implies QWEST is re-entering the consideration set but must translate share gains into sustained velocity to keep advancing against top-five stability.

Notable Products

Georgia Pie (7g) posted the steepest decline at -12.20% month over month and held rank 3, while White Walker #2 (7g) fell -10.52% at rank 2, signaling pressure in larger Flower formats despite Platinum Gas (7g) rising 11.29% at rank 4. Three of the top ten are Pre-Roll SKUs, led by Vision Pre-Roll 2-Pack (2g) up 8.08% at rank 1 and contrasted by Georgia Pie Pre-Roll 5-Pack (2.5g) down -16.71% at rank 9, indicating pack-size sensitivity and format bifurcation. With Flower declines concentrated in two top ranks and mixed Pre-Roll performance including a 22.80% lift for Georgia Pie Pre-Roll 10-Pack (3.5g) at rank 6 against an -11.74% drop for Platinum Gas Pre-Roll 10-Pack (3.5g) at rank 10, the pattern implies QWEST is pivoting toward targeted Pre-Roll variants while rationalizing underperforming Flower sizes.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.