Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

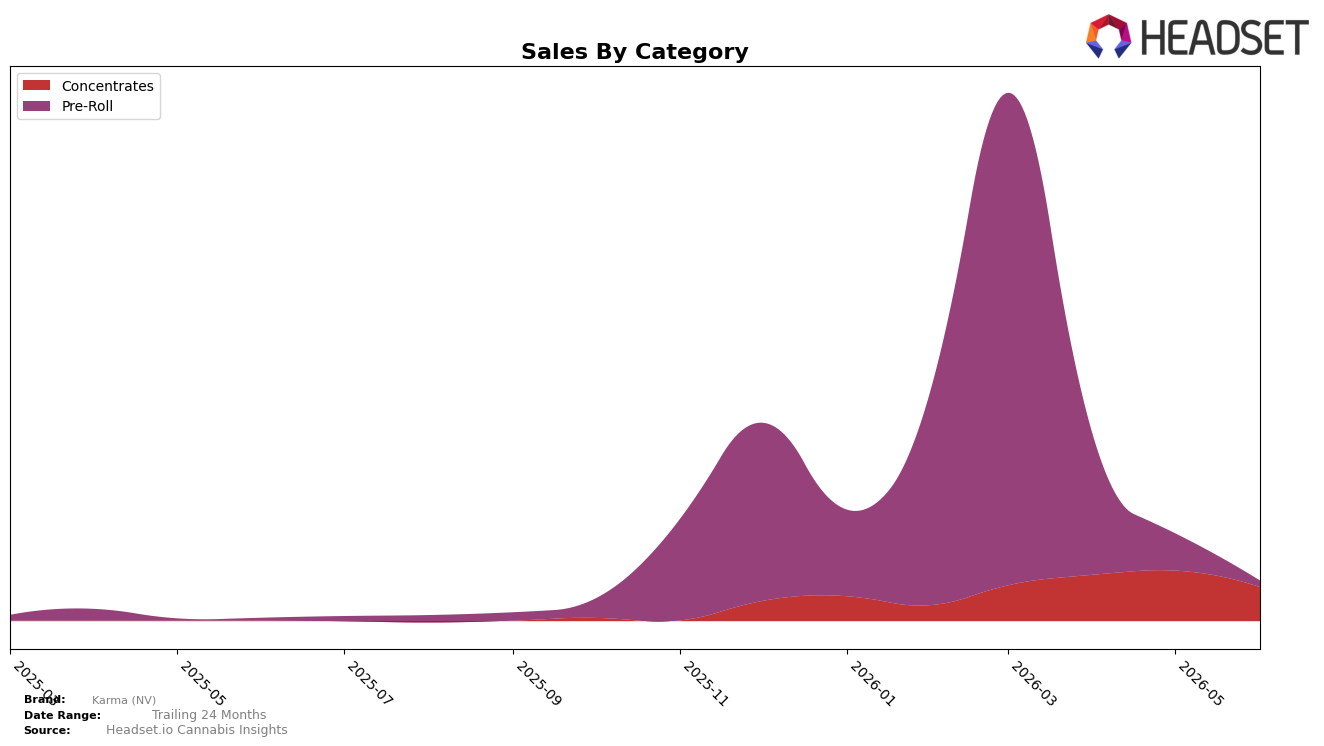

Karma (NV) derived 84.66% share from Concentrates in June 2026, with Pre-Roll at 15.34%, indicating a narrow category mix; within the month, Concentrates fell 32.84% MoM while Pre-Roll dropped 83.44% MoM. Year over year, Pre-Roll expanded 144.17% while brand-level sales rose 1,491.33% and average price declined 36.86%, implying volume-led growth concentrated in a low-priced Concentrates core while Pre-Roll is volatile on a much smaller base. The concentration in Concentrates alongside sharply divergent MoM trends suggests the brand is overexposed to month-to-month swings in a single category in Nevada, and the price compression points to deliberate down-tier positioning to accelerate unit throughput.

The combination of an 84.66% Concentrates mix and a 36.86% YoY price decline indicates a value-led stance that prioritizes unit velocity over ticket size, while the 144.17% YoY growth in Pre-Roll adds an experimental secondary pillar without yet changing the center of gravity. With Concentrates dropping 32.84% MoM versus an 83.44% MoM drop in Pre-Roll, the portfolio is bearing asymmetric downside from smaller segments, implying Karma (NV) should treat Pre-Roll as episodic demand capture rather than a stable driver and reinforce price-pack architecture in Concentrates to defend baseline share in Nevada.

Competitive Landscape

Karma (NV) sits at rank #29 in NV Concentrates in June 2026, improving 6 positions from #35 in March 2026, while its peak rank of #26 in May 2026 indicates a 3-position slide month over month; by contrast, Medizin holds #1 despite a -37.0% YoY sales change and Nature's Chemistry is #4 after jumping from #13 YoY with +102.0% sales growth, implying Karma’s near-peak in May 2026 followed by a June 2026 pullback suggests mid-tier volatility where small share shifts can move ranks materially.

Notable Products

Cream Soda Badder (0.05g) delivered the standout move in June 2026 with a +344.3% MoM surge to rank 1, while Indica Rest Rso Syringe (1g) fell -40.8% to rank 4, signaling a sharp pivot toward inhalable concentrates. Side Peace Crumble (0.05g) added +85.8% MoM at rank 3, and five of the top ten are Concentrates, indicating category concentration rather than broad portfolio momentum. Pre-Roll exposure softened as Cake Pop Honey Infused Pre-Roll (1.2g) dropped -50.0% to rank 6 against a single-month revenue peak of $1,845 from Citrus Butter Badder (1g), reinforcing that June 2026 demand clustered in small-format badder and crumble while ingestible syringes retrenched. The pattern implies Karma (NV) is leaning into high-velocity Concentrates led by small-pack badder, with Pre-Rolls and RSO positioned as secondary.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.