Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Clout King is stocked at 383 licensed dispensaries across Michigan, Washington, and 6 other states, 154 of them in Michigan, with the deepest coverage in Detroit, New Buffalo, Monroe, Inkster, and Ann Arbor. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

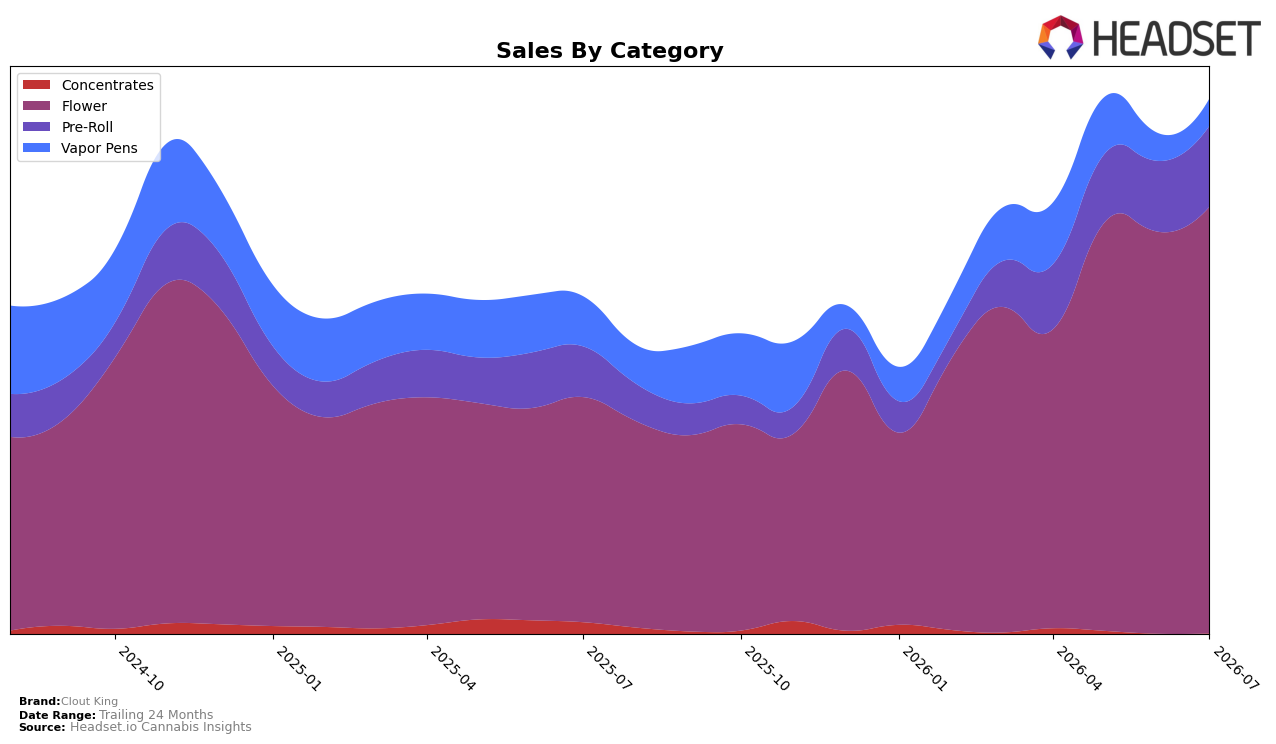

Clout King's mix in July 2026 concentrated 77.72% in Flower with year-over-year growth of 87.61% and month-over-month growth of 6.04%, while Pre-Roll held 15.45% share with 54.28% YoY and 13.36% MoM gains. Vapor Pens fell to 5.81% share with a -41.39% YoY decline and a -1.52% MoM change, and Concentrates were 1.02% share with -66.34% YoY but a 7.29% MoM uptick. Average price fell 14.85% YoY to $23.20 as Flower’s $34.07 average and Vapor Pens’ $24.02 contrast with Pre-Roll at $8.80, and the brand’s overall sales were up 55.33% YoY alongside a 24‑month rise of 43.46%. The pattern implies a deliberate tilt toward Flower and Pre-Roll volume expansion, using lower pricing to amplify share gains while deemphasizing Vapor Pens and Concentrates.

With Flower at rank 24 in Nevada and 77.72% of mix, the 6.04% MoM gain in Flower combined with a 13.36% MoM lift in Pre-Roll indicates near-term share capture potential anchored in inhalables, even as Vapor Pens contract by -41.39% YoY. The -14.85% YoY average price shift, alongside Pre-Roll’s 54.28% YoY growth and Concentrates’ -66.34% YoY drop, points to a price-to-volume trade that prioritizes basket conversion over premium positioning. The implication is a positioning strategy centered on Flower-led scale with Pre-Roll as the entry engine, accepting reduced presence in oil-based formats to consolidate rank through throughput rather than margin density.

Competitive Landscape

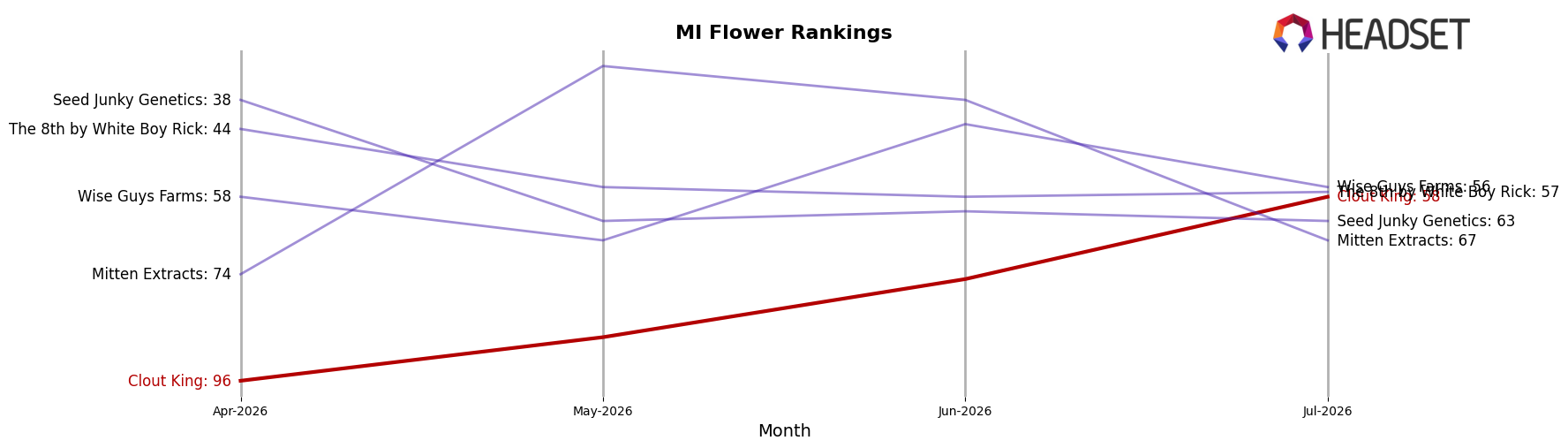

Clout King sits at rank #58 in MI Flower in July 2026, improving 59 positions from #117 year over year and rising 38 spots from #96 in April 2026, marking its peak rank to date at #58 in July 2026; by contrast, Goodlyfe Farms advanced from #5 to #3 with 36.8% YoY sales growth while Pro Gro slipped from #3 to #5 alongside a 12.0% YoY sales decline, and the gap to High Minded at #1 has widened even as that leader posted a 12.5% YoY sales contraction; the mix of a 59-rank YoY leap and a 38-rank improvement over three months implies Clout King has transitioned from lower-tier volatility to mid-pack relevance, with further share gains contingent on converting momentum into sustained velocity against top-5 incumbents.

Notable Products

Clout King’s largest month-over-month mover was Clout Berries (3.5g), up 54.6% to push into rank 9, outpacing the Flower peer set where Tussin Snacks (3.5g) rose 52.8% to seize rank 1. Hood Snacks (3.5g) also climbed 29.9% to rank 3 while Wagyu Pre-Roll (1g) slipped 0.4% at rank 4, and six of the top ten SKUs are Flower, indicating a concentrated tilt toward eighths rather than Pre-Rolls. With three Flower SKUs in the top three ranks and only one Pre-Roll in the top five, the mix signals an emphasis on flagship eighths as the primary growth engine, suggesting the brand is prioritizing package-flower velocity over breadth in Pre-Rolls.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.