Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

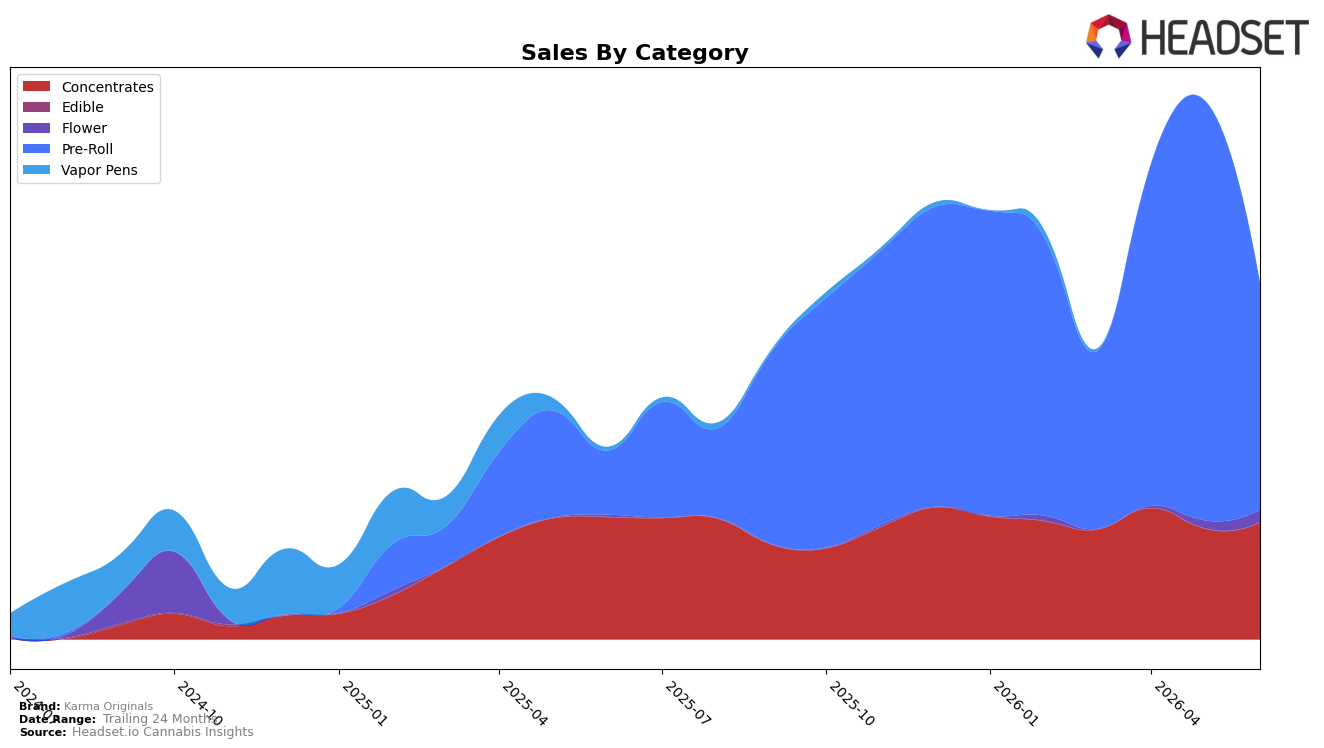

Pre-Roll holds 63.78% share in June 2026 with year-over-year growth of 255.75% but a month-over-month drop of 45.96%, while Concentrates accounts for 32.85% share with a -4.31% YoY change and a 5.52% MoM increase. Flower remains small at 3.37% share yet posts a 588.78% YoY surge and 61.90% MoM lift, alongside an average price of $25.34 versus $15.06 in Pre-Roll. With the brand ranked 14 in Pre-Roll in Nevada, the combined spike in Flower and stability in Concentrates point to a portfolio tilt away from a single-category dependence, even as Pre-Roll still anchors volume.

The sharp Pre-Roll MoM contraction of 45.96% alongside a 5.52% MoM gain in Concentrates and 61.90% MoM growth in Flower implies near-term exposure to volatility in the lead category and a hedge emerging in higher-priced formats. The 255.75% YoY rise in Pre-Roll versus a -4.31% YoY dip in Concentrates indicates that long-run momentum remains Pre-Roll-led, but the 588.78% YoY surge in Flower at a premium price signals room to reposition toward value-per-use and potency cues; together with a 14th rank in Nevada Pre-Roll, the pattern implies that mix diversification could be the pathway to improve rank without leaning solely on discount-driven Pre-Roll volume.

Competitive Landscape

Karma Originals sits at rank #14 in June 2026, improving 28 positions from #42 year over year, and up 5 spots from #19 in March 2026; despite this climb, the brand remains below its peak at #7 from January 2026, indicating a partial rebound rather than a full return to prior positioning. In the same period, STIIIZY held at #1 year over year while its sales declined 34.8%, and Rove advanced from #4 to #2 with 63.7% YoY sales growth, suggesting Karma Originals’ rank gains are occurring alongside mixed competitor momentum at the top. The pattern implies Karma Originals’ upward rank trajectory is driven by consistent share recovery rather than category lift alone, but closing the gap to its January 2026 peak will require converting recent positional wins into sustained top-10 presence.

Notable Products

Octane Runtz Rush Infused Pre-Roll (1.2g) posted the largest month-over-month surge at 89.9% and climbed to rank 2, while Dipstick - Strawberry Cookies Infused Pre-Roll (1g) fell 14.7% to rank 5, indicating a sharp divergence within infused pre-rolls. Indica RSO Syringe (1g) rose 7.9% and held rank 1, whereas Sativa RSO Syringe (1g) added 7.0% at rank 3, creating a stable top-three anchor around RSO syringes. Four of the top ten are infused pre-rolls, but with one SKU up 89.9% and another down 39.7% at rank 7, the category shows volatility that contrasts with steady RSO concentration gains. The pattern implies Karma Originals is leaning on consistent RSO syringe demand to fund experimentation in infused pre-rolls, using breakout wins to offset SKU-level churn.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.