Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

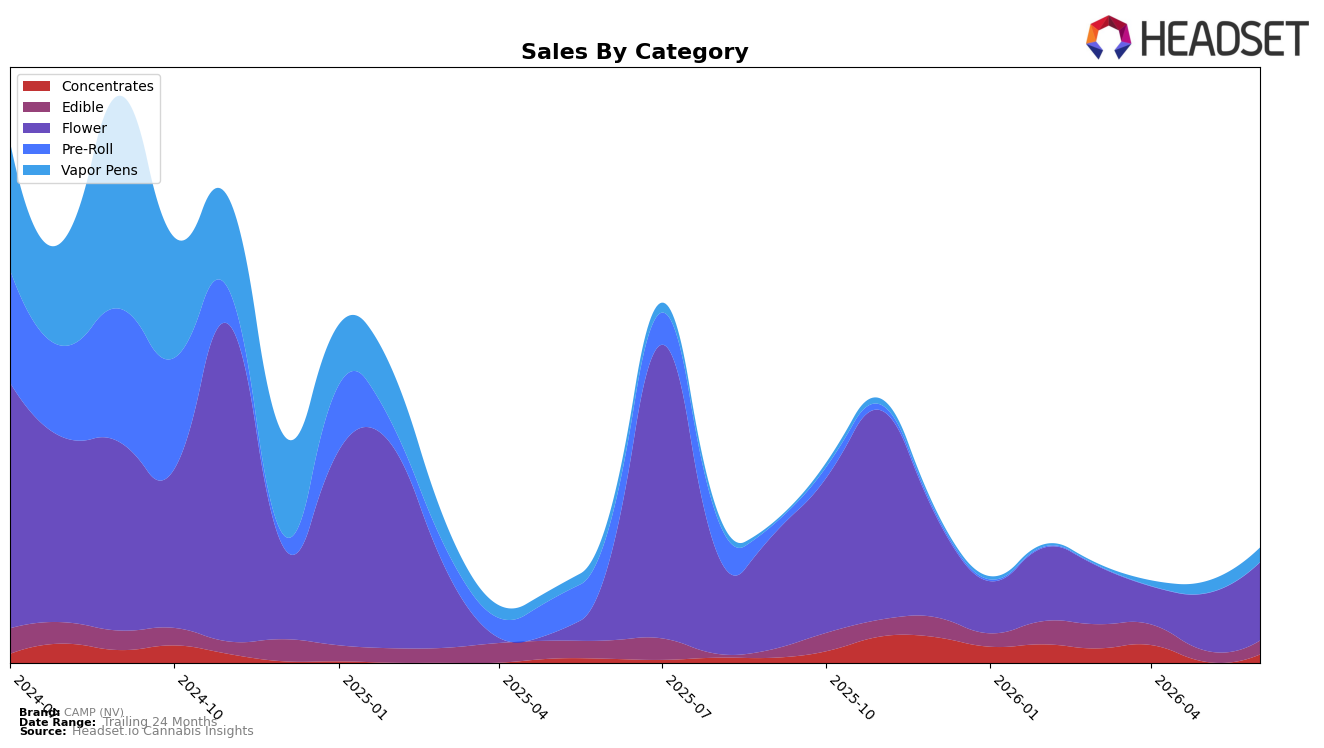

In June 2026, CAMP (NV) concentrated 68.24% of sales in Flower, where sales grew 3.57% year over year and 38.04% month over month, while Vapor Pens held 12.47% share with 23.74% YoY and 24.06% MoM gains; by contrast, Edible at 11.87% share declined 24.85% YoY even as it grew 23.96% MoM, and Concentrates at 7.42% share surged 104.72% YoY and 568.71% MoM from a smaller base. Despite a 47.57% YoY increase in average price and a brand-level sales decline of 20.29% YoY, category momentum skewed toward inhalables, implying a pivot toward higher-velocity, inhalation-led baskets that can offset weakness in Edible.

With Flower anchoring share and Vapor Pens expanding, the mix indicates reliance on quick-turn formats, while the outsized 568.71% MoM jump in Concentrates alongside a 104.72% YoY lift signals experimentation that could rebalance revenue if sustained; however, Edible’s 24.85% YoY contraction constrains diversification benefits. Holding rank 22 in Flower in Nevada alongside a 3.57% Flower YoY uptick suggests mid-pack placement where incremental share gains hinge on maintaining MoM Flower growth (38.04%) and translating Concentrates’ spike into stable repeat, implying a positioning path that prioritizes inhalable differentiation while selectively repairing Edible to reduce volatility.

Competitive Landscape

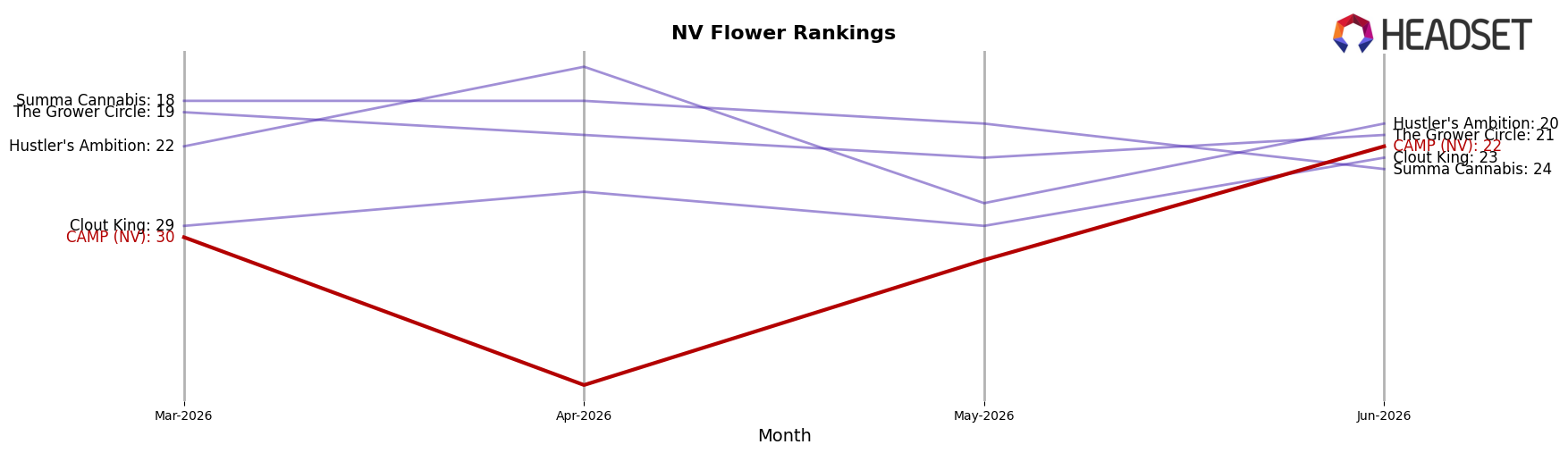

CAMP (NV) sits at rank #22 in NV Flower in June 2026, improving 2 positions from #24 year over year, and rising 8 spots from #30 three months ago, while still far from its peak at #4 in November 2024; by contrast, STIIIZY holds #1 with a 5.2% year-over-year sales lift and RYTHM is #2 despite a 6.9% sales decline, indicating CAMP (NV) is gaining rank even as top-tier dynamics remain mixed. The sharper rank ascent of FloraVega / Welleaf to #3 from #22 year over year alongside a 260.4% sales increase contrasts with CAMP (NV)’s steadier climb of 2 positions year over year and 8 ranks quarter-to-date, implying CAMP (NV) is rebuilding share methodically rather than via a breakout surge, and this trajectory points to incremental competitive re-entry rather than rapid recapture of its November 2024 peak.

Notable Products

Plum Sangria (3.5g) led June 2026 with a 106% month-over-month jump to rank 3, while First Class Funk #5 (3.5g) rose 99% to rank 1, indicating outsized momentum concentrated at the top. In contrast, Gush Mints (3.5g) slid 10% to rank 2 and LA Kush Cake (3.5g) dipped 1% to rank 4, suggesting rotation within Flower even as leaders expand. Four of the top ten are Flower SKUs clustered at ranks 1, 2, 3, and 4, and the Glitter Bomb Flower Rosin Cartridge (0.5g) surged 125% to rank 6, pointing to solventless crossovers supporting both inhalable segments. The mix implies CAMP (NV) is consolidating around high-velocity Flower while seeding solventless Vapor Pens to diversify volume without abandoning core demand.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.