Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Pressure Concentrates (NV) is stocked at 119 licensed dispensaries across California, Oklahoma, and 2 other states, 53 of them in California, with the deepest coverage in Modesto, San Jose, Fresno, Lake Elsinore, and San Diego. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

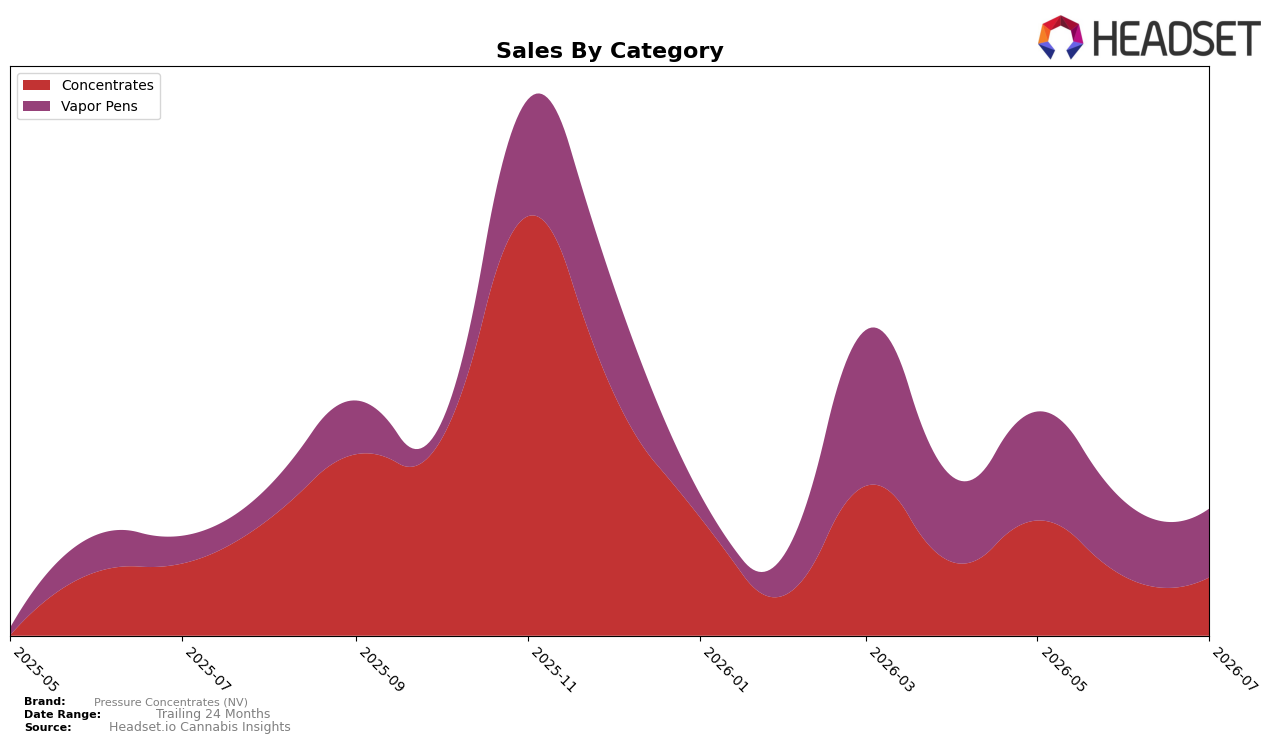

Pressure Concentrates (NV) split July 2026 sales roughly half-and-half between Vapor Pens at 52.74% share and Concentrates at 47.26% share, with Vapor Pens up 67.40% year over year while down 5.72% month over month, and Concentrates down 13.19% year over year and down 0.85% month over month. The brand’s overall year-over-year sales rose 16.35% alongside an 11.80% decline in average price to $32.73, while Vapor Pens carried a higher average price of $36.19 than Concentrates at $29.57. This pattern implies a pivot where growth is being carried by higher-priced Vapor Pens despite a recent monthly pullback, while Concentrates act as a stabilizer with a shallower month-over-month decline but a contracting year-over-year base.

Within Nevada Vapor Pens, the brand ranked 66 in July 2026, a position consistent with a niche presence even as the category now commands 52.74% of its mix and logged 67.40% year-over-year growth. The simultaneous 5.72% month-over-month dip in Vapor Pens and 0.85% month-over-month dip in Concentrates, paired with an 11.80% average price decline, indicates the brand is trading into mainstream price bands to win volume while leaning on Vapor Pens for trajectory. The implication is a positioning strategy centered on gaining share in Vapor Pens through price accessibility and mix weighting, while Concentrates serve as a complementary line that tempers volatility but currently dilutes year-over-year momentum.

Competitive Landscape

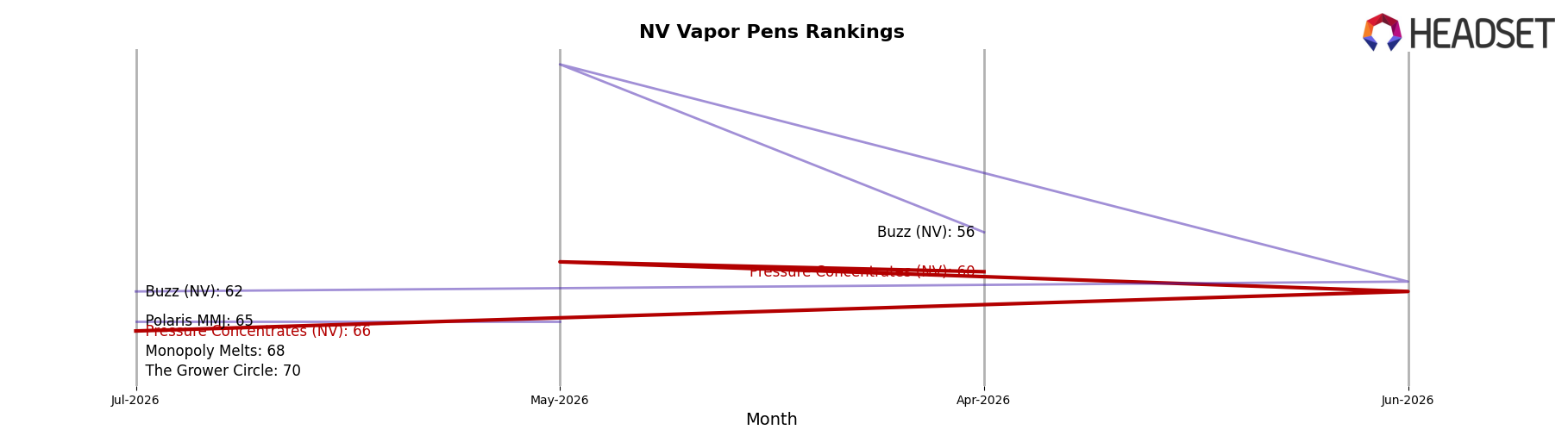

Pressure Concentrates (NV) sits at rank #66 in NV Vapor Pens in July 2026, slipping 1 position year over year from #65 while falling 6 spots since April 2026 from #60, versus its peak of #53 in December 2025; meanwhile, Rove held #1 with a -32.0% year-over-year sales change and AiroPro climbed from #8 to #5 alongside a 103.6% year-over-year increase, indicating that Pressure Concentrates (NV) is losing relative position as faster-rising competitors compress the middle tier and the brand’s downward rank drift points to share pressure concentrated between its post-peak slide and rivals’ gains.

Notable Products

Zushi Live Resin Disposable (1g) posted the standout move in July 2026 with a 105% month-over-month surge to $1,905 and climbed to rank 2, while Wedding Cake Live Resin Disposable (0.5g) fell 28% to rank 6, signaling volatility within the disposable mix. Gusher Lemonade Live Resin Disposable (1g) also contracted by 10% and sat at rank 6, whereas Super Boof Live Rosin Disposable (0.5g) rose 11% to rank 5, indicating a tilt toward newer or differentiated disposable formats. Four of the top ten are Vapor Pens, led by Cap Junky Live Resin Disposable (0.5g) at rank 1 and Acai Runtz Live Resin Disposable (1g) inching up 4% to rank 4, implying the brand’s momentum is anchored in disposables rather than jarred concentrates. The pattern points to a commercial direction prioritizing high-velocity disposable SKUs and rapid iteration, with selective pruning where rank erosion exceeds 10%.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.