Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Korova is stocked at 99 licensed dispensaries across Arizona, California, and Oregon, 49 of them in Arizona, with the deepest coverage in Phoenix, Mesa, Glendale, Chandler, and Avondale. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

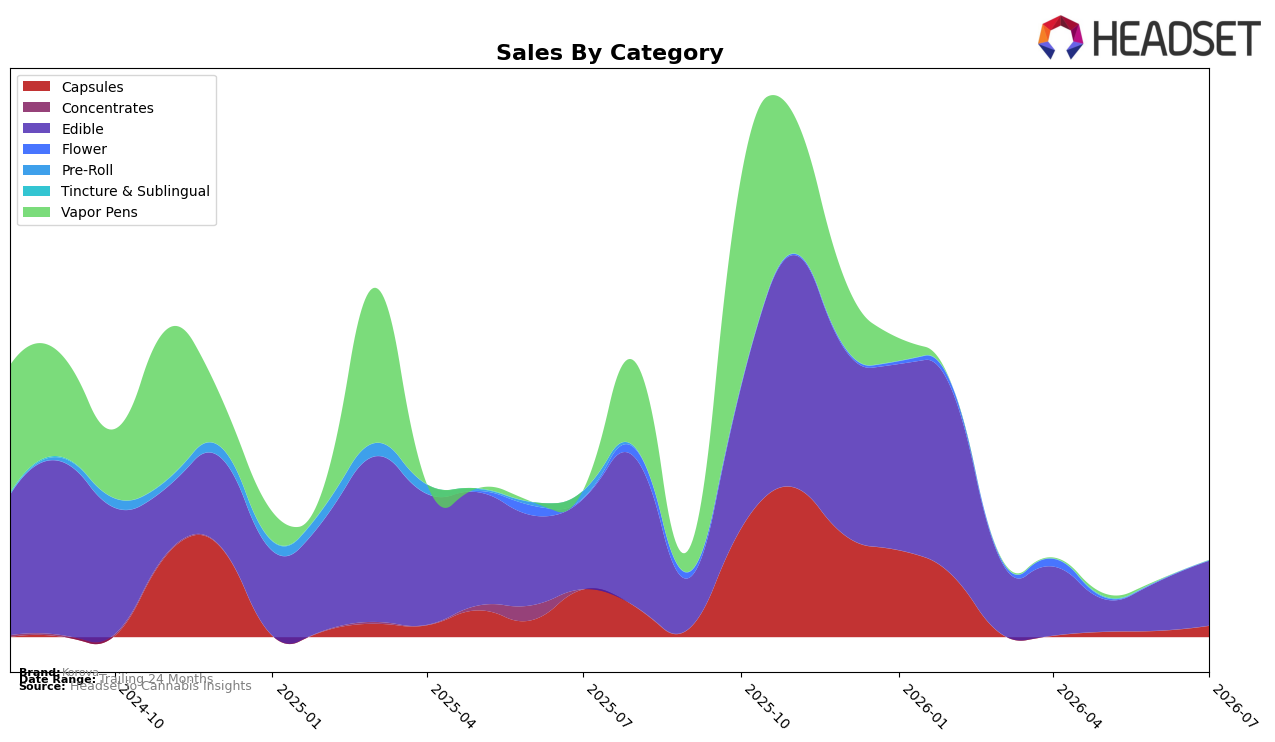

In July 2026, Korova concentrated 85.38% of sales in Edible while Capsules held 14.62%, a mix that tightened around Edible as Capsules contracted year over year by 76.68% versus a 28.04% decline in Edible. Month over month, both categories expanded, with Capsules up 83.43% and Edible up 32.93%, yet the annual picture stayed negative with total brand sales down 47.78% as average price fell 29.32% to $16.04. The combination of a sharp YoY pullback in Capsules alongside a smaller YoY decline in Edible, despite strong MoM rebounds in both, implies Korova is de-risking around Edible while using short-term Capsule lift to stabilize share without reversing the longer-term downdraft.

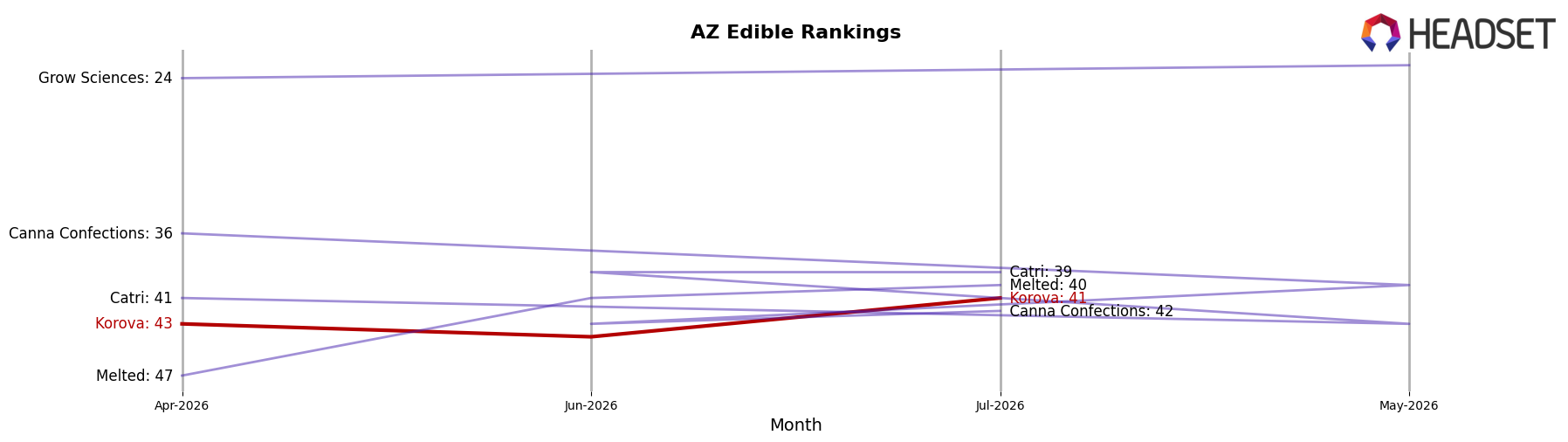

Korova’s Edible-led mix aligns with its Arizona Edible ranking at position 41, but the 14.62% share from higher-ticket Capsules at an average price of 37.10 versus 14.62 in Edible raises a margin-versus-scale tradeoff as Capsules shrink 76.68% YoY even while surging 83.43% MoM. With total brand sales down 66.01% over 24 months and Edible declining 28.04% YoY against a 32.93% MoM bounce, the data point to a positioning that relies on Edible for volume while Capsules serve as a volatility lever rather than a durable pillar; the strategy implied is to lean into Edible assortment and pricing architecture while only selectively rebuilding Capsules where repeat signals justify the higher price point.

Competitive Landscape

Korova sits at rank #41 in AZ Edible as of July 2026, matching its peak rank of #41 and improving 2 positions from April 2026’s #43, while year-over-year rank is unspecified but the current placement marks a new high. In directional context, Wyld holds #1 despite a -10.0% year-over-year sales shift, and Baked Bros climbed from #4 to #3 alongside a 27.6% sales increase, whereas Gron / Grön slid from #3 to #4 with a -1.8% change; this spread indicates Korova’s 2-rank lift over three months is occurring amid both contraction at the top and selective gains mid-pack, implying the brand’s trajectory depends on converting recent rank stability at #41 into sustained upward movement before entrenched leaders widen their lead.

Notable Products

Indica Grape Twerpz Rope Gummy (100mg) led July 2026 with a 114% month-over-month surge into rank 3, outpacing the category while Strawberry Twerpz Rope Gummy (100mg) rose 13% to hold rank 1. Twerpz Rope - Peach Gummy (100mg) slid 12% at rank 4, and Hybrid Fruit Punch Twerpz Rope Gummy (100mg) declined 16% at rank 6, indicating winner-take-most momentum within a narrow flavor set. With eight of the top ten in Edibles and only one Capsules item cracking the top five, the mix points to a flavor-driven gummy core where volatility can be exploited by doubling down on high-velocity SKUs and pruning underperforming variants.

Geltab 10-Pack (1000mg) vaulted 83% month over month to rank 5 with approximately $2,851 in July 2026 sales, while Black Bar Brownie (100mg) climbed 21% at rank 8 against a 25% drop for Chocolate Chip Dip Mini Cookies 10-Pack (100mg) at rank 7. The concentration of rope gummies among the top ten suggests format concentration risk alongside upside from rapid switchovers, implying Korova can steer commercial direction by prioritizing the fastest-ascending gummy flavors while ring-fencing exposure to declining cookie formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.