Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

UP! is stocked at 11 licensed dispensaries across California, with the deepest coverage in San Diego, La Mesa, Chula Vista, Encinitas, and Lemon Grove. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

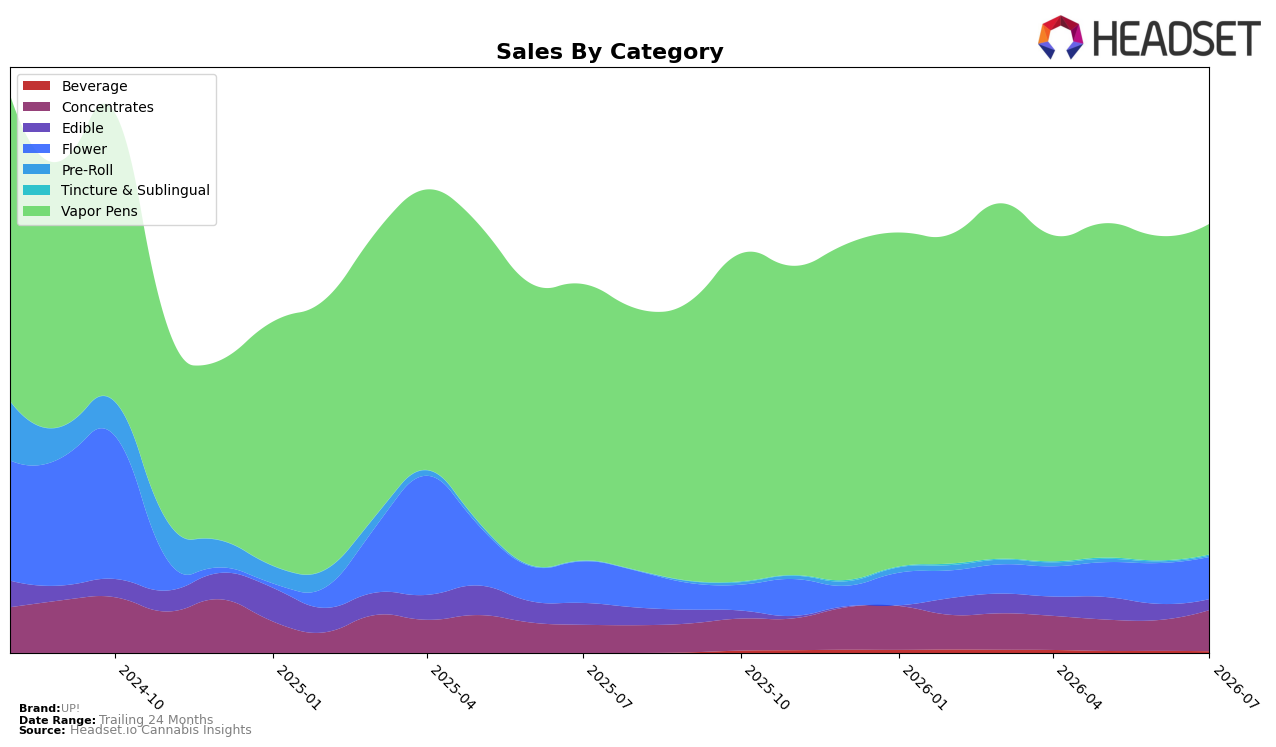

UP! concentrated 77.35% of July 2026 sales in Vapor Pens, where sales grew 19.64% year over year and 1.89% month over month, while the brand held rank 20 in Vapor Pens in California. Mix shifted into Concentrates at 9.55% share with a 46.80% YoY surge and 34.01% MoM gain, contrasted with Edible, which fell 50.64% YoY and 33.29% MoM to 2.49% share; Flower held 9.79% share with modest 1.37% YoY and 3.48% MoM growth. With Beverage down 16.34% MoM to 0.40% share and Tincture & Sublingual up 23.89% MoM to 0.19% share, the mix is polarizing toward inhalables, implying a portfolio tilt that prioritizes repeatable, lower-price inhalation formats over slower-turn ingestibles.

The category shifts imply UP! is leaning into price-accessible inhalables, evidenced by a 5.62% YoY decline in average price alongside a 16.43% YoY sales lift and heavier weight in Vapor Pens and Concentrates (a combined 86.90% share). The collapse in Edible (down 50.64% YoY and 33.29% MoM) alongside a Pre-Roll rebound YoY of 537.24% but a 28.76% MoM pullback suggests experimentation outside core lanes is volatile, so maintaining rank 20 in Vapor Pens in California while capturing MoM upside in Concentrates (+34.01%) is the practical path to defend share and margin through volume rather than premium pricing.

Competitive Landscape

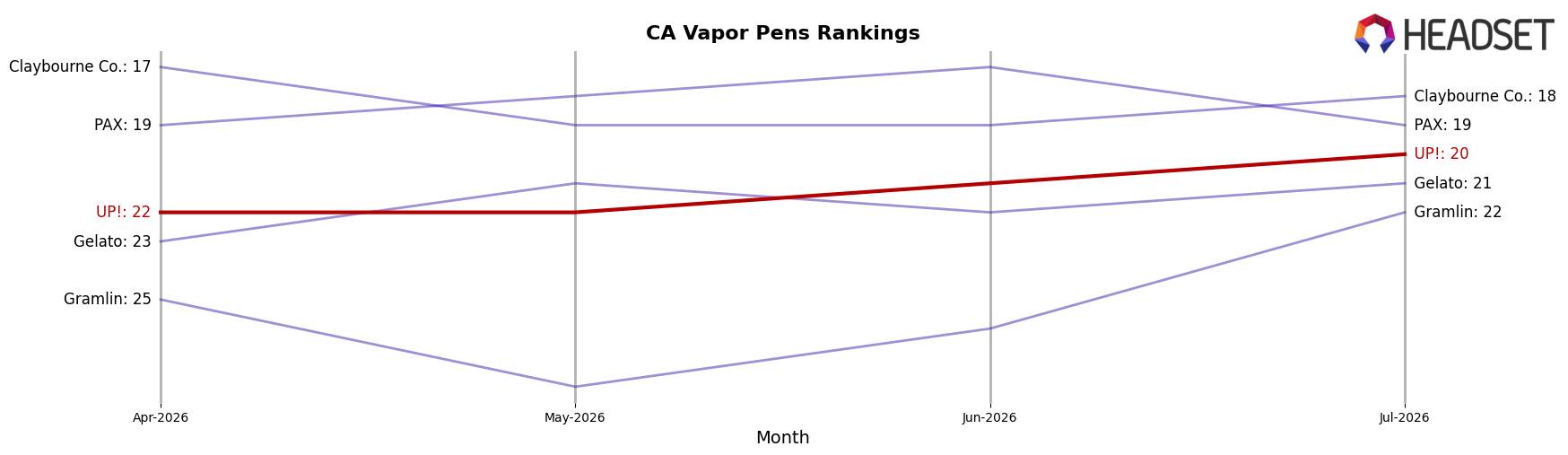

UP! sits at rank #20 in CA Vapor Pens in July 2026, improving 5 positions from #25 year over year and slipping 2 spots from #22 in April 2026; the brand’s peak at #19 in March 2026 underscores a ceiling just above current placement, while category leaders moved unevenly as Jetty Extracts climbed from #4 to #3 and Plug Play fell from #3 to #4. Against a flat top-tier, STIIIZY held #1 with a -6.8% year-over-year sales change and Raw Garden stayed #2 with +4.6% year-over-year growth, signaling that UP!’s 5-rank annual gain is coming from mid-pack churn rather than pressure on the top five; the pattern implies UP!’s trajectory is upward but capped unless it converts intermittent peaks into sustained share that closes the 1-rank gap to its March 2026 best and stabilizes month-to-month rank losses of 2 positions.

Notable Products

SFV OG Live Resin Cartridge (1g) posted the largest move in July 2026 with a +144.7% month-over-month surge, jumping into rank 3, while Mango Kush Live Resin Cartridge (1g) slipped -16.5% yet held rank 1. Skywalker OG Live Resin Cartridge (1g) fell -24.2% to rank 5 as Blue Dream Live Resin Cartridge (1g) inched up +6.5% at rank 2, concentrating momentum in mid-tier ranks rather than the top slot. With all top-10 entries in Vapor Pens and four live resin SKUs occupying ranks 1–5, the mix signals UP! leaning into live resin depth to stabilize leadership even as the flagship softens.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.