Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

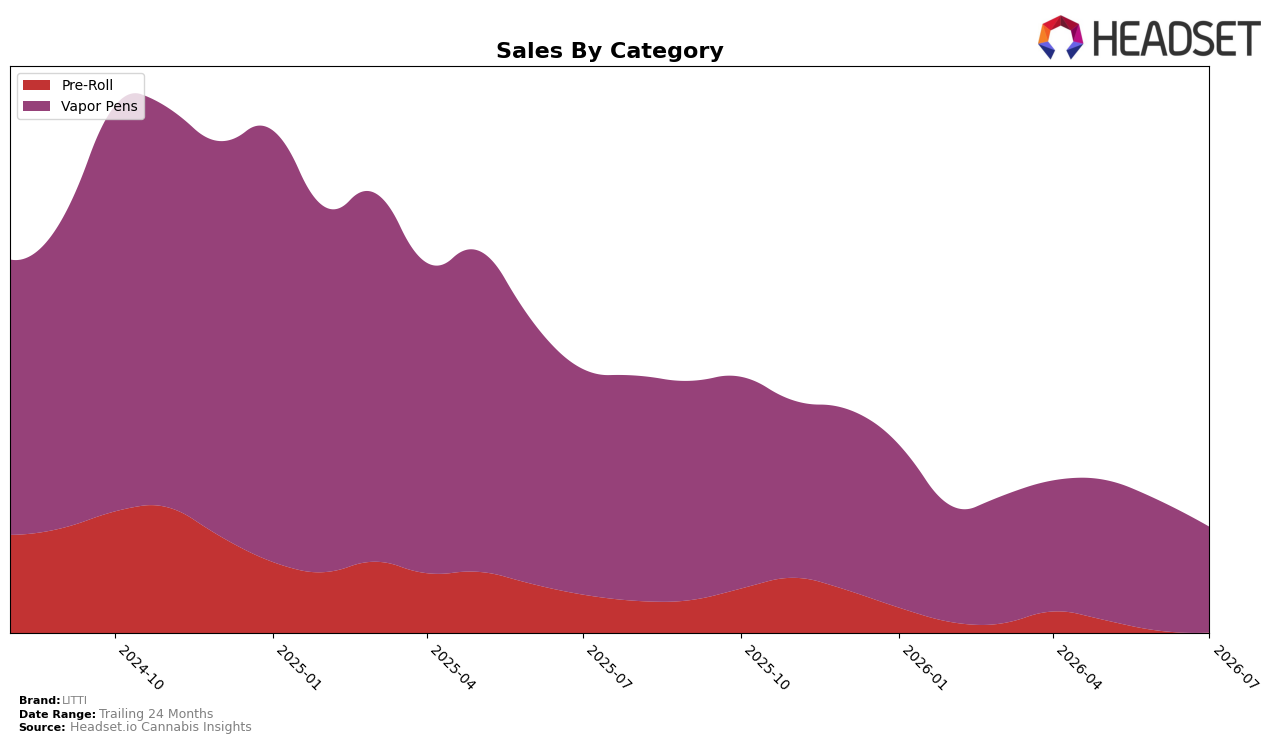

In July 2026, LITTI’s mix concentrated further into Vapor Pens at 86.83% share, while Pre-Roll held 13.17% share, indicating a narrower portfolio despite a brand-level year-over-year sales change of -52.42%. Vapor Pens declined -49.07% YoY and -16.66% MoM, whereas Pre-Roll fell deeper at -66.81% YoY and -9.66% MoM, and the average price moved +9.29% YoY to $29.47. With Vapor Pens carrying both the largest share and the steeper month-on-month volume pressure, and Pre-Roll underperforming faster year over year, the pattern implies reliance on a contracting core that is not being offset by secondary categories.

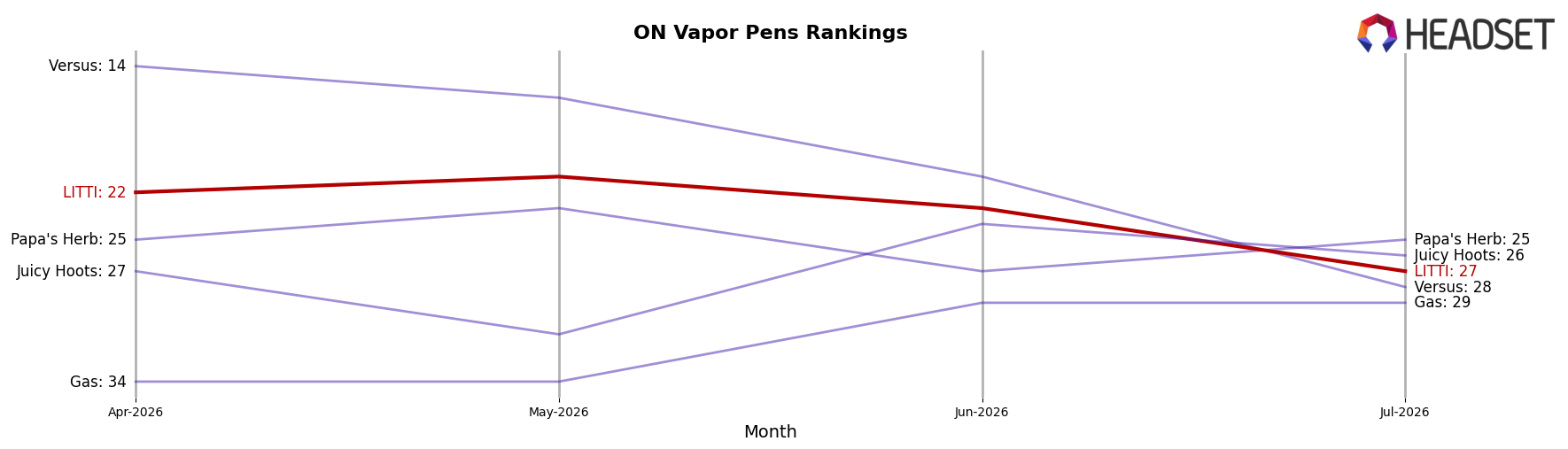

Given a Vapor Pens rank of 27 in Ontario and a category share nearing 87%, the brand’s footprint is concentrated in a mid-pack position rather than diversified protection across formats. The -16.66% MoM decline in Vapor Pens versus a -9.66% MoM drop in Pre-Roll, paired with a -49.07% versus -66.81% YoY split, implies that short-term elasticity is testing the core while the secondary line lacks scale to rebalance mix; this positioning suggests LITTI must either defend Vapor Pens at rank 27 in Ontario or reallocate toward formats with better retention to prevent further share erosion.

Competitive Landscape

LITTI sits at rank #27 in ON Vapor Pens in July 2026 after sliding 13 positions year over year from #14, and falling 5 ranks since April 2026 from #22, while its historical peak was #8 in October 2024; in contrast, Spinach climbed from #4 to #1 with 144.72% YoY sales growth and BoxHot edged up from #2 to #3 as General Admission moved down from #3 to #4 alongside a -18.96% YoY sales change, indicating LITTI’s downward rank momentum amid top-tier consolidation and that reclaiming mid-teen share will likely require reversing multi-quarter slippage rather than counting on category churn.

Notable Products

Bussn' Blackberry Distillate Cartridge (1g) posted the steepest decline in July 2026 at -28.0% MoM while dropping within the top five to rank 5, and Slappn' Berry Distillate Cartridge (1g) also contracted -17.1% MoM despite holding rank 1. Sunrise Smash Liquid Diamonds Cartridge (1g) slid -5.8% MoM at rank 2 as Pushn' Peach Distillate Cartridge (1g) fell -16.9% MoM at rank 4, and Cherry Chonk Liquid Diamonds Disposable (1g) deteriorated -34.7% MoM at rank 6 against a modest +5.5% MoM uptick for Berry Blaze Liquid Diamonds Disposable (1g) at rank 7. With eight of the top ten concentrated in Vapor Pens and both distillate and liquid diamonds showing mixed momentum, the pattern implies LITTI is overexposed to pen formats that are cooling month over month and needs mix shifts toward SKUs with proven resiliency and fewer sequential declines.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.