Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Locals Only Concentrates is stocked at 139 licensed dispensaries across New Jersey, Nevada, and 2 other states, 59 of them in New Jersey, with the deepest coverage in Franklin Township, Evesham, Hackettstown, Trenton, and Union. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

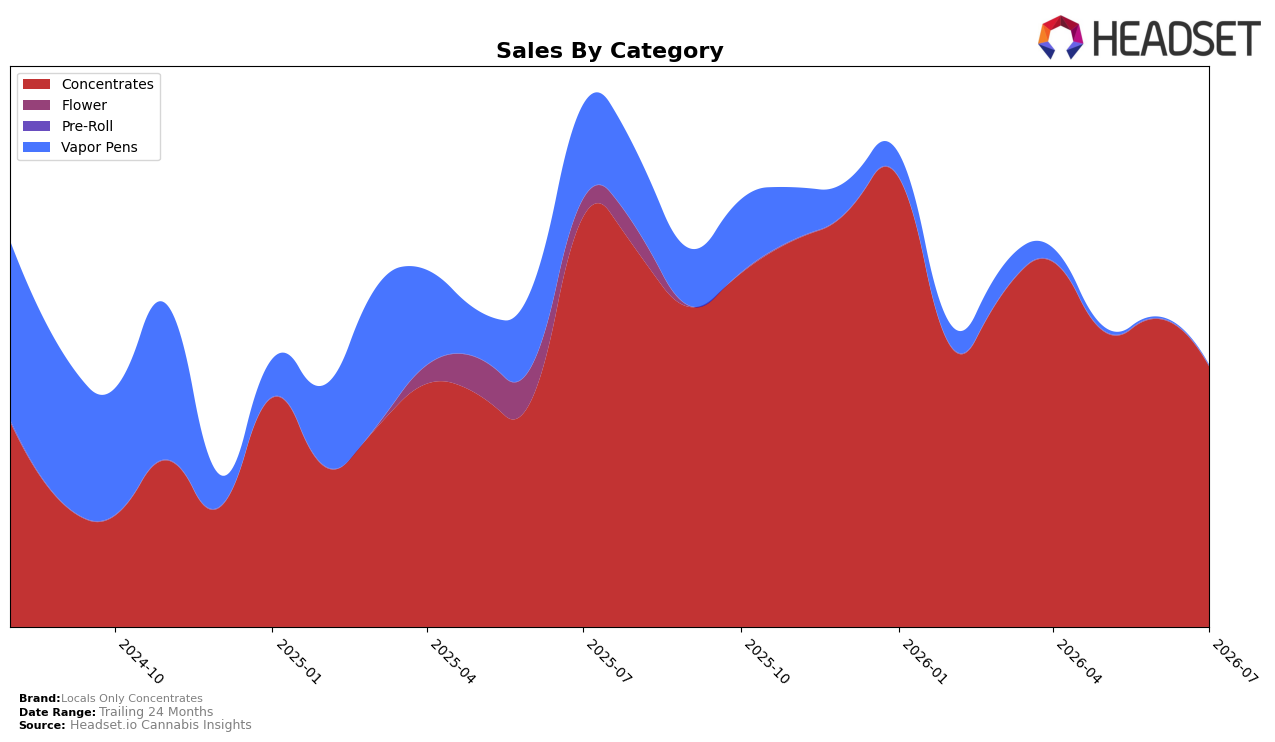

In July 2026, Locals Only Concentrates concentrated 99.76% of sales in Concentrates, while Vapor Pens fell to 0.24% share; within these, Concentrates declined 36.45% year over year and 15.43% month over month, and Vapor Pens dropped 99.32% year over year and 44.93% month over month. With average price up 27.62% year over year to $31.15 alongside a 49.91% brand-level year-over-year sales contraction, the mix indicates a retreat from multi-category participation and a price-led compression of volume that is most visible in Concentrates.

Holding rank 9 in Concentrates in New Jersey while category share sits at 99.76% suggests dependence on a single shelf battle where the month-over-month drop of 15.43% in the core category outpaced the 44.93% slide in the negligible Vapor Pens base. The combination of a 24-month sales change of -29.24% and a July 2026 price point 27.62% above last year implies the brand is trading fewer units at higher tickets, narrowing its addressable audience and raising the risk that small rank losses in Concentrates could cascade into disproportionate total-brand declines.

Competitive Landscape

Locals Only Concentrates sits at rank #9 in July 2026, down 3 positions year over year from #6, and 4 positions lower than its three-month mark of #5, indicating a 5-rank slide from its peak of #4 in June 2026; meanwhile, Grassroots advanced to #1 from #3 YoY while growing sales by 36.3%, and RYTHM held near the top at #2 despite an 11.1% YoY sales decline, placing Locals Only Concentrates at a relative disadvantage versus both upward and resilient incumbents. The juxtaposition of Locals Only Concentrates’ 3-rank YoY decline and 4-position drop since April–June levels against competitors maintaining or improving top-two placements implies a trajectory toward the lower half of the top 10 unless share recapture reverses the post–June peak erosion.

Notable Products

Orange Push Pop Live Wet Diamonds (1g) posted the largest month-over-month gain at +55.8% and climbed to rank 3, while Fig Bar Wet Badder (1g) also surged +52.9% at rank 4. Countering that momentum, J1 Live Wet Diamonds (1g) fell -32.8% at rank 5 and Lemon Cherry Gelato Live Wet Diamonds (1g) dropped -43.1% at rank 10, indicating selective demand rather than a category-wide lift. With Fig Bar Live Wet Diamonds (1g) holding rank 1 on a +38.5% increase and three Live Wet Diamonds SKUs sitting in the top 5, the mix tilts toward fresh-frozen formats where flavor-led variants are consolidating share. The simultaneous -21.9% slide for Orange Push Pop Badder (1g) at rank 2 versus one Live Wet Diamonds namesake up +55.8% suggests shoppers are trading into wetter textures even when strain branding is constant, pointing to a product strategy that favors Live Wet Diamonds over Badder at scale.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.