Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Lolo is stocked at 305 licensed dispensaries across California and Washington, 301 of them in California, with the deepest coverage in Los Angeles, San Francisco, Costa Mesa, Long Beach, and San Diego. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

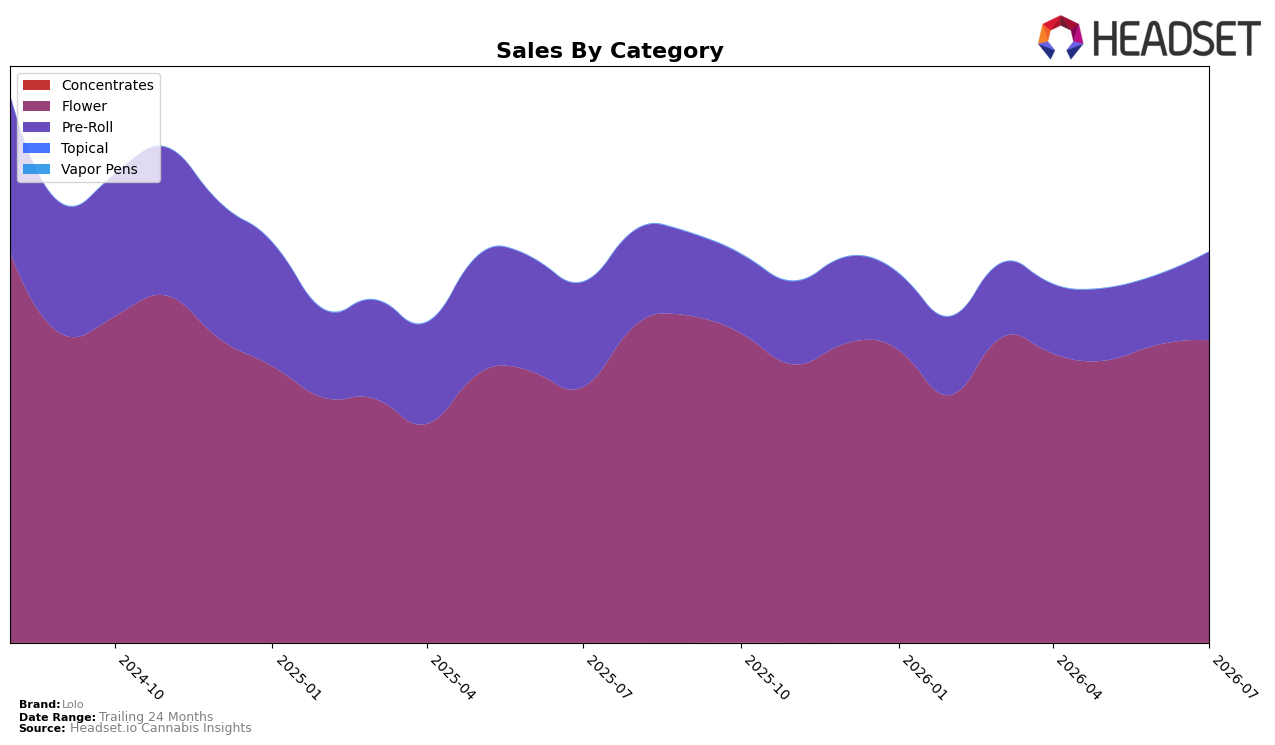

In July 2026, Lolo’s mix is concentrated in Flower at 77.43% share with a 1.57% month-over-month lift and an 18.31% year-over-year increase, while Pre-Roll holds 22.57% share with a 26.25% month-over-month surge but a 15.84% year-over-year decline. Average price rose 16.60% year over year to $13.55, and within the mix, Flower’s higher average price relative to Pre-Roll aligns with Lolo’s rank of 33 in Flower in California. The pattern implies Lolo is leaning into higher-priced Flower momentum to offset softer Pre-Roll trends, using July 2026 mix stability and sequential gains to reinforce visibility where it already competes for position.

With total brand sales up 8.36% year over year but down 38.71% over 24 months, a 77.43% Flower dependency paired with a 22.57% Pre-Roll buffer suggests risk concentration if Flower growth moderates; however, the 1.57% Flower month-over-month increase versus a 26.25% Pre-Roll month-over-month jump indicates near-term elasticity to re-engage value-seeking buyers without abandoning premium cues. Given the 18.31% Flower year-over-year rise alongside a 15.84% Pre-Roll year-over-year contraction, the portfolio trajectory points to a positioning that centers on core Flower credibility while tactically restoring Pre-Roll velocity to stabilize share and improve rank efficiency within July 2026 category lanes.

Competitive Landscape

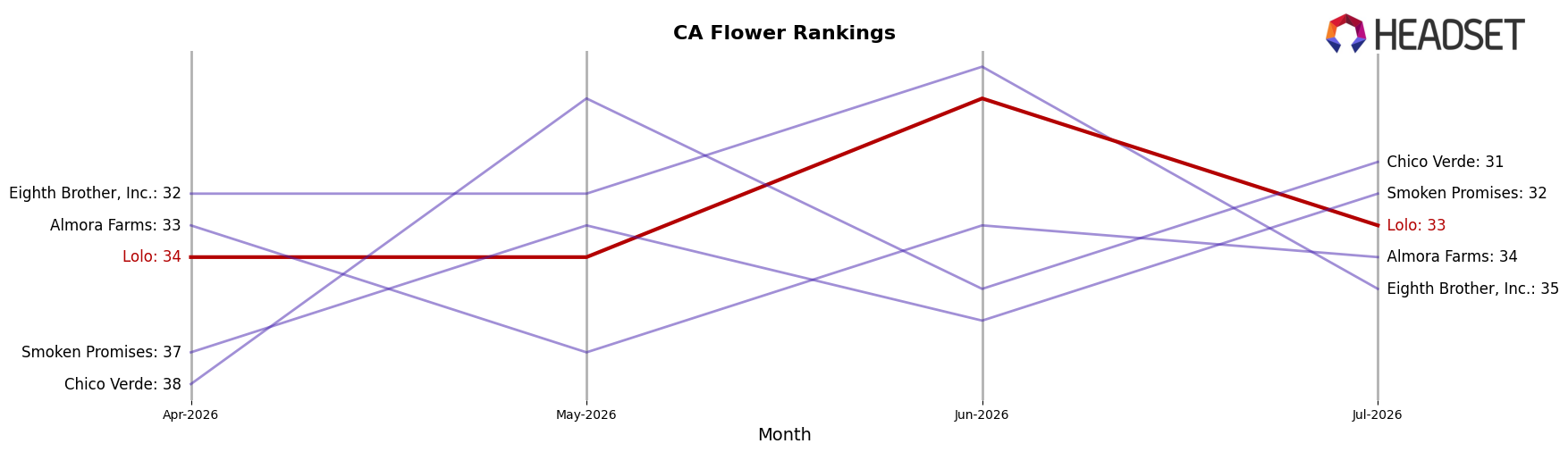

Lolo sits at rank #33 in California Flower in July 2026, a 6-position improvement from #39 year over year, while slipping 1 spot from #34 three months prior; the brand’s historical ceiling remains #24 from July 2024, placing current performance 9 ranks below its prior peak and 31 positions behind the present category leader. Competitively, STIIIZY climbed from #2 to #1 as its sales grew 59.7% year over year, and CAM moved from #4 to #3 with a 52.2% lift, whereas Claybourne Co. fell from #3 to #5 alongside a 1.4% sales decline; this mix of upward pressure at the top and selective slippage among incumbents implies Lolo’s modest rank gain amid a 1-position quarter-over-quarter dip signals stabilization rather than acceleration, suggesting the path back toward its July 2024 peak depends on outpacing mid-tier movers rather than chasing top-three momentum.

Notable Products

OG Chem Pre-Roll (1g) delivered the standout move in July 2026 with a 376.5% MoM surge that vaulted it to rank 1, while Kosher Tangie Infused Pre-Roll (1g) also accelerated 62.0% MoM to enter the top ten at rank 9. Across the leaderboard, Pre-Rolls dominated with eight of the top ten SKUs, and Blueberry Scone Pre-Roll (1g) and Gold Rush Pre-Roll (1g) posted mid-tier gains of 24.2% and 25.2% while holding ranks 4 and 6, respectively. In contrast, the Flower segment showed steadier momentum as Peanut Butter Cake (3.5g) grew 9.6% MoM at rank 8, and Holy Grail OG Smalls (3.5g) sat at rank 3 with the month’s highest dollar total at $38,217. Together, the outsized Pre-Roll gains at ranks 1, 4, 6, 9, and 10 point to a portfolio tilting toward ready-to-use formats, signaling resource allocation should favor Pre-Roll depth over incremental Flower breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.