Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

In June 2026, Time Machine leaned heavier into Pre-Roll, with Pre-Roll holding a 59.5% mix and Flower at 40.5%, while overall brand sales were down 12.1% year over year and average price fell 6.3%. Pre-Roll volume momentum showed up in month-over-month growth of 6.2% even as its year-over-year sales declined 21.6%, whereas Flower moved the other way with a 38.4% year-over-year increase but a 7.9% month-over-month decline; the brand’s ranking in California Pre-Roll sat at 16. Together, those divergences indicate a portfolio in which the core Pre-Roll pillar still drives June 2026 sell-through week to week, but the annual comp pressure suggests mix imbalance risk if Flower’s recent month-over-month softness persists.

The combination of a 6.2% Pre-Roll month-over-month lift alongside a 7.9% Flower month-over-month drop implies near-term reliance on Pre-Roll traffic despite its 21.6% year-over-year contraction, while the 38.4% year-over-year Flower gain signals longer-cycle traction at a lower average price point of $21.65 versus $34.51. With a 59.5% Pre-Roll share and rank 16 in California Pre-Roll, the brand’s positioning skews toward value-seeking multi-pack or budget-friendly formats, and June 2026 strategy likely benefits from rebalancing mix toward Flower to capture the higher year-over-year growth while using price architecture to stem Pre-Roll’s annual declines.

Competitive Landscape

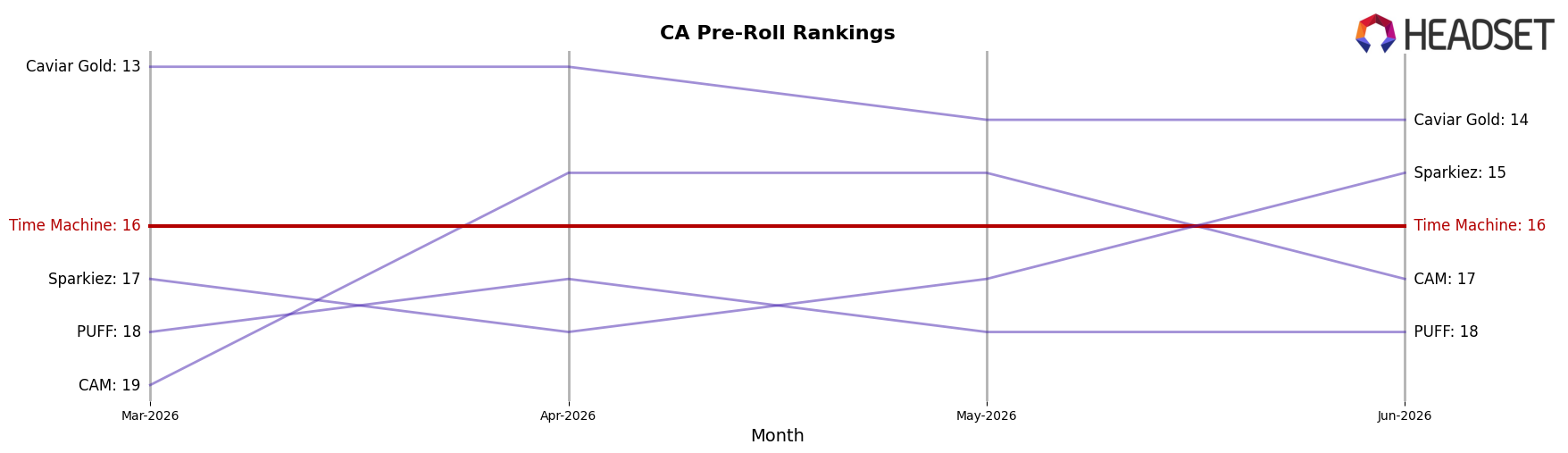

Time Machine sits at rank #16 in CA Pre-Roll in June 2026, down 4 positions year over year from #12, with no change versus March 2026 at #16; in contrast, CannaBiotix (CBX) advanced from #7 to #4 while growing sales an estimated 39.09%, and category leaders like Jeeter held #1 with roughly 0.66% sales growth as STIIIZY maintained #2 on approximately 4.82% growth; given Time Machine’s slip from its December 2025 peak at #11 to #16 and a flat three-month trend at #16, the pattern implies share consolidation at the top and that Time Machine must overcome a 5-rank gap to re-enter prior peak territory.

Notable Products

Gorilla Glue #4 Pre-Roll 28-Pack (14g) posted the steepest decline at -7.1% MoM while slipping to rank 4, whereas Blue Dream Pre-Roll 28-Pack (14g) rose 20.5% MoM to hold rank 1. Wedding Cake (1g) climbed 32.4% MoM at rank 6, and GG4 (1g) advanced 26.7% MoM at rank 7, indicating momentum in 1g Flower even as a related pre-roll cooled. With six of the top ten in Pre-Roll and three SKUs clustered at ranks 1–3, the mix points to concentration in large-count pre-rolls, suggesting the brand is leaning into multi-pack value while selectively nurturing 1g Flower as an upsell path.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.