Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

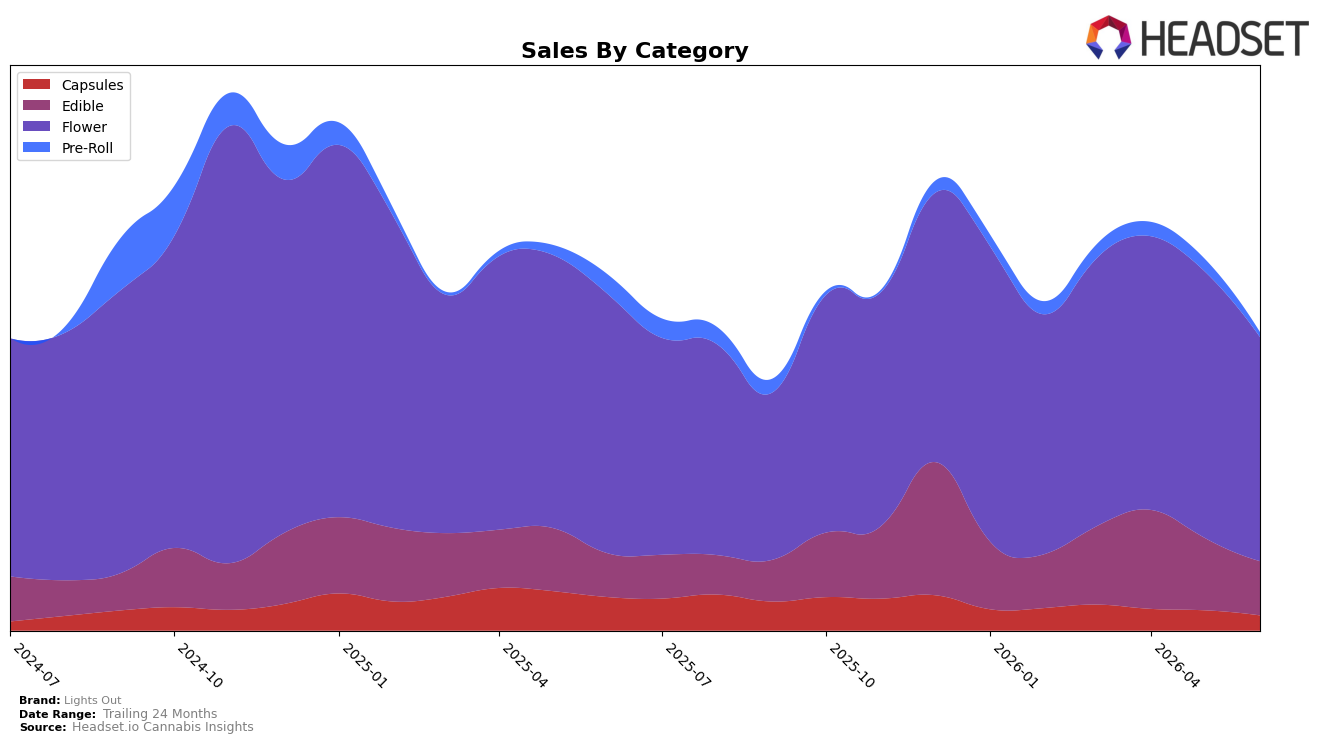

In June 2026, Lights Out concentrated 75.31% of sales in Flower with a year-over-year decline of 13.49% and a month-over-month drop of 15.95%, while Edible expanded year-over-year by 24.39% but contracted month-over-month by 25.29%; Capsules fell 55.12% year-over-year and 25.54% month-over-month, and Pre-Roll contracted 76.04% year-over-year and 62.33% month-over-month. Despite a 9.33% year-over-year decrease in average price and an overall brand sales decline of 16.17% year-over-year, Flower still anchors the mix and aligns with a rank of 65 in Flower for California, implying that concentration risk in a softening lead category is outweighing Edible’s year-over-year growth.

The shift shows dependency on a single category where share leadership is not implied by a 65th rank in California Flower, while Edible’s 18.12% share and positive year-over-year of 24.39% have not offset steep month-over-month declines of 25.29% and 62.33% in Edible and Pre-Roll respectively. With Capsules at 5.02% share and down 55.12% year-over-year versus Flower down 13.49% year-over-year, the portfolio skews toward lower-momentum segments, implying that near-term positioning depends on reallocating emphasis from contracting Flower and collapsed Pre-Roll toward sustained Edible growth while protecting price architecture around the $20.90 average ticket.

Competitive Landscape

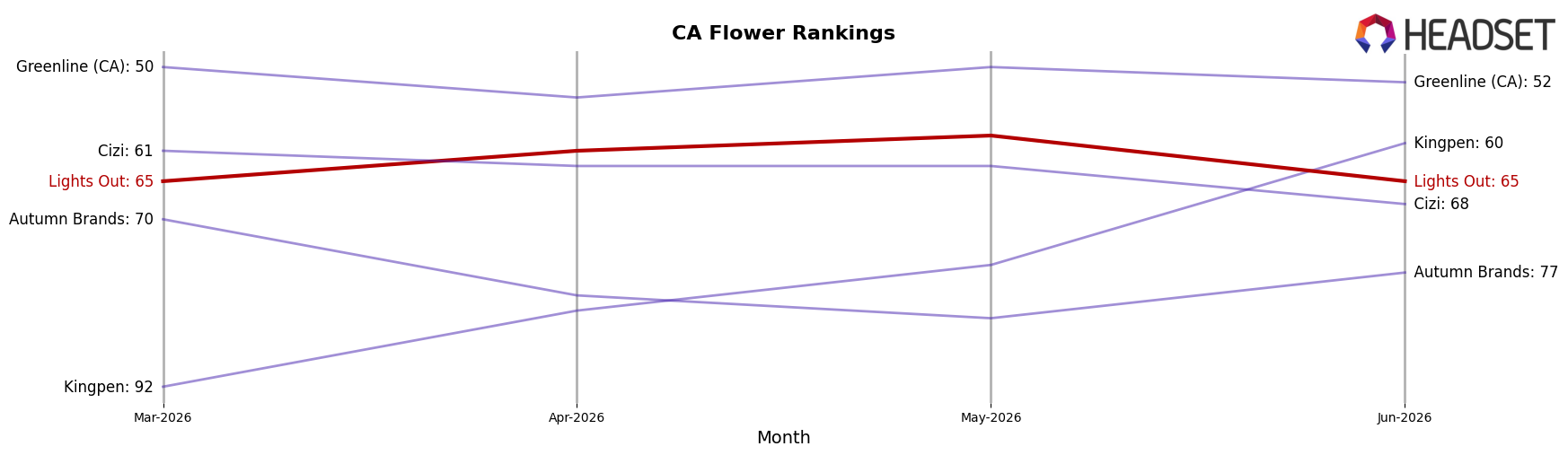

Lights Out sits at rank #65 in CA Flower for June 2026, a 1-position improvement from #66 year over year, while holding flat versus March 2026 at #65; against the category ceiling, the brand remains 21 spots below its peak of #44 from November 2024 and trails the top tier where STIIIZY advanced from #2 to #1 and CAM climbed from #3 to #2 as CannaBiotix (CBX) slipped from #1 to #3; this mix of a 1-rank YoY gain and zero movement over the last quarter suggests incremental recovery without momentum, implying that Lights Out’s rank trajectory points to stabilization rather than a path back toward its prior #44 peak.

Notable Products

Sativa Strawberry Live Rosin Gummies 10-Pack (100mg) posted the steepest decline at -60.7% MoM while holding rank 9, contrasting with Orange Live Rosin Gummies 10-Pack (100mg) up 14.2% at rank 7 and THC/CBN/CBD 1:1:1 Wildberry Deep Sleep Gummies 10-Pack (100mg THC, 100mg CBN, 100mg CBD) down 12.5% at rank 3. Saturn OG (3.5g) stayed at rank 1 but fell 22.1% MoM on $124,005, as Pink Acai (3.5g) slipped 1.9% at rank 2 and Indica Watermelon Live Rosin Gummies 10-Pack (100mg) dropped 23.7% at rank 5. With six of the top ten as Edible SKUs and two Flower SKUs anchoring ranks 1–2, the skew toward Edibles with mixed month-to-month volatility implies Lights Out is leaning into a two-pillar mix where Flower leads share while Edibles cycle through sharper trial-driven swings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.