Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

THC Design is stocked at 251 licensed dispensaries across California and Nevada, 211 of them in California, with the deepest coverage in Los Angeles, San Diego, Santa Ana, Costa Mesa, and San Francisco. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

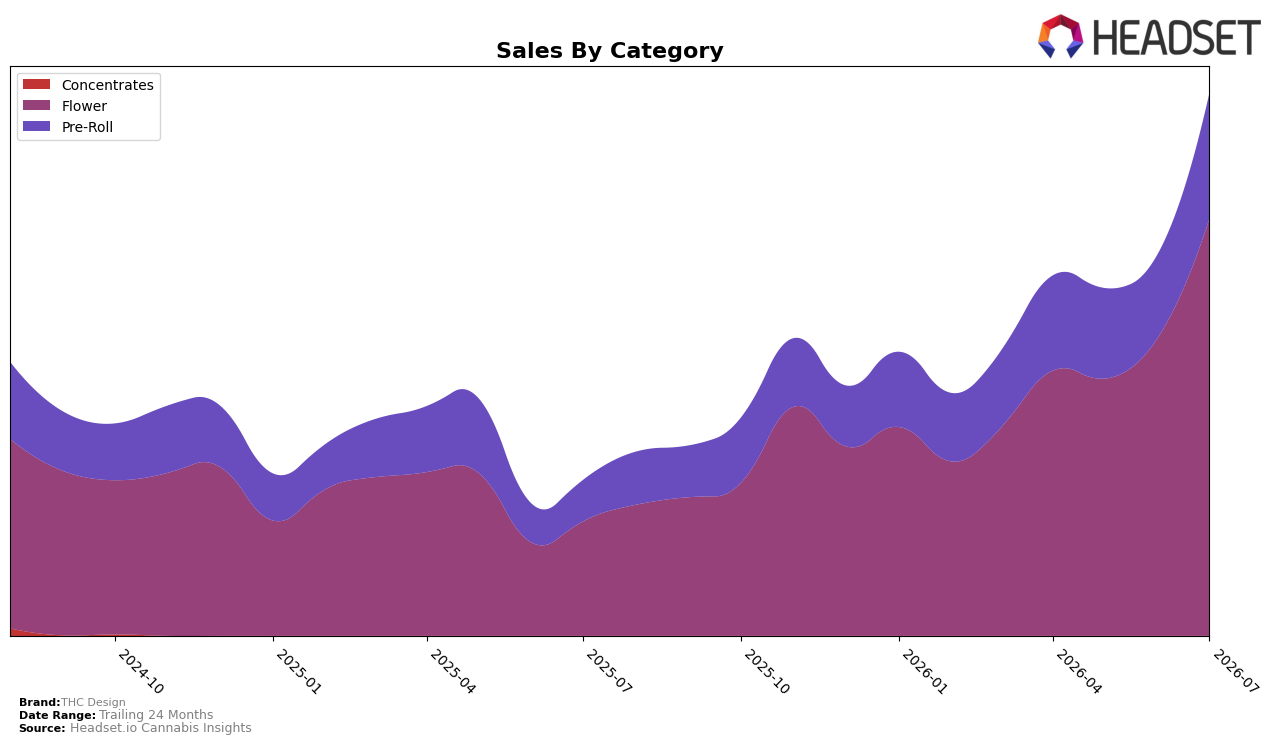

In July 2026, THC Design concentrated 76.88% of sales in Flower with a 265.52% year-over-year gain and a 39.91% month-over-month lift, while Pre-Roll held 23.12% share with 204.18% YoY growth and a 49.92% MoM increase; together this aligns with a brand-level 249.24% YoY sales expansion and a 17.48% YoY drop in average price to $25.23. With Flower’s average price at 34.76 and Pre-Roll at 13.20, the mix skew and faster MoM in Pre-Roll indicate volume-led growth, implying THC Design is trading into broader baskets while maintaining Flower as the primary revenue engine.

Positioning-wise, a 76.88% Flower share combined with a 49.92% MoM surge in Pre-Roll suggests portfolio reach is widening without diluting the Flower anchor, supported by a 92.73% 24-month growth trajectory and an average price down 17.48% YoY. Holding rank 10 in Flower in Nevada alongside a 39.91% MoM gain in Flower and a 23.12% Pre-Roll share implies competitive traction from price-enabled trial and multipack-oriented formats, signaling that THC Design is positioning for basket penetration and repeat purchase rather than premium-only share.

Competitive Landscape

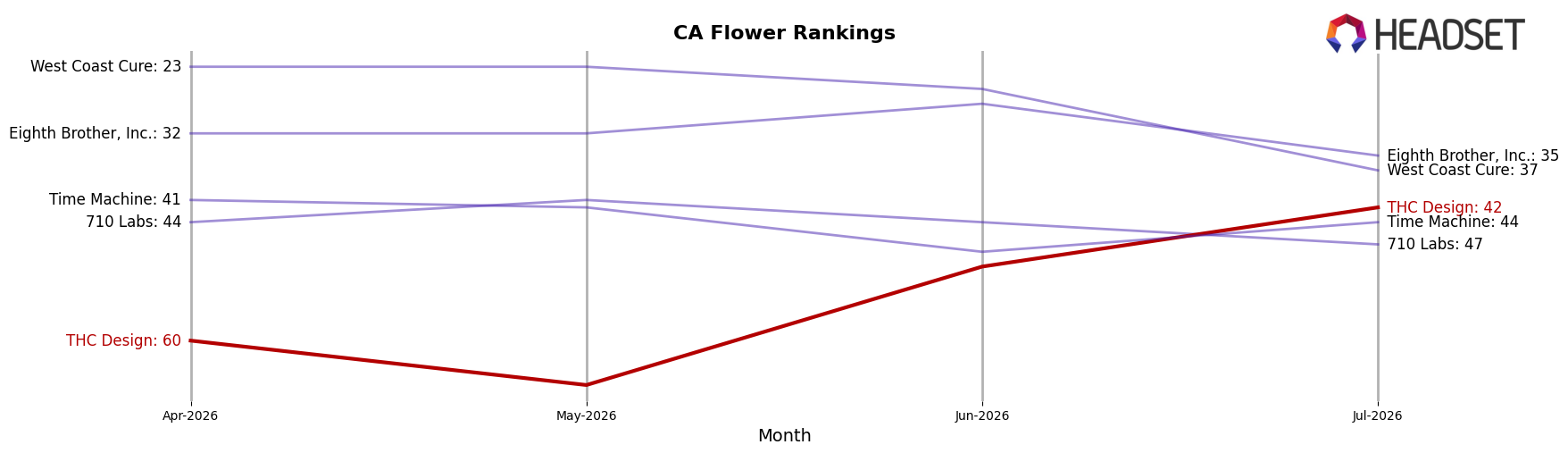

THC Design sits at rank #42 in California Flower in July 2026, improving 71 places year over year from #113 while rising 18 positions from #60 since April 2026, and both moves coincide with a new peak rank reached in July 2026; by comparison, STIIIZY advanced from #2 to #1 while growing sales 59.7% year over year and CAM climbed from #4 to #3 with 52.2% sales growth, indicating that THC Design’s rapid rank ascent is catching up from a deep prior trough rather than pressuring the top tier yet, and the trajectory implies continued mid-pack momentum if multi-month gains persist against leaders consolidating near the top.

Notable Products

Super Lemon Haze Pre-Roll (1g) posted the largest shift with a 142.5% month-over-month increase and reached rank 2, while Crescendo (3.5g) climbed 82.8% to rank 1 with $137,089 in July 2026. El Chivo (3.5g) advanced 93.9% to rank 3 as Garlic Cocktail (3.5g) dipped 2.2% at rank 7, and Flower accounted for four of the top ten while Pre-Roll held five of the top ten. The pattern implies THC Design is leaning into a two-engine mix where Flower anchors the top ranks and accelerating Pre-Roll growth expands the reach, setting up a portfolio weighted toward high-velocity strain extensions and format variety.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.