Market Insights Snapshot

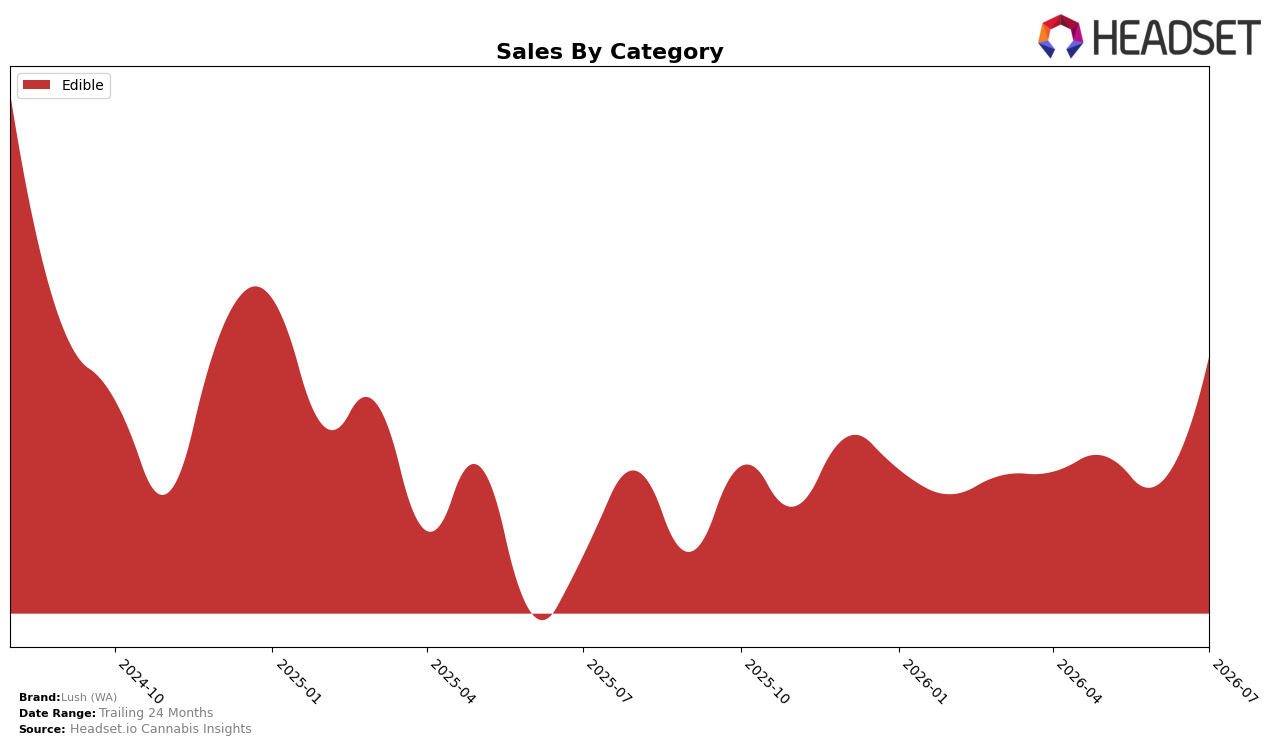

In July 2026, Lush (WA) operated as a single-category brand with Edible accounting for 100.0% of sales, posting a 24.2% year-over-year increase alongside a 14.3% month-over-month gain; average price in Edible rose 0.8% year over year while the category’s sales rank in Washington stood at 20 within Edible. The combination of a 24.2% YoY lift with full category concentration and a 14.3% MoM upswing implies the brand is leaning into depth over breadth, using Edible price stability (+0.8% YoY) to convert demand rather than relying on mix diversification.

With rank 20 in Washington Edibles and a 100.0% category share, the 14.3% MoM growth tied to just a 0.8% price increase suggests volume was the primary driver, while the 24.2% YoY gain against a 21.8% two-year decline signals a rebound phase rather than an expansion into new categories. This pattern implies Lush (WA) is positioned as a focused Edible specialist aiming to regain shelf velocity through volume-led gains at a stable mid-teens average price point ($15.86), prioritizing penetration and repeat rates over cross-category reach.

Competitive Landscape

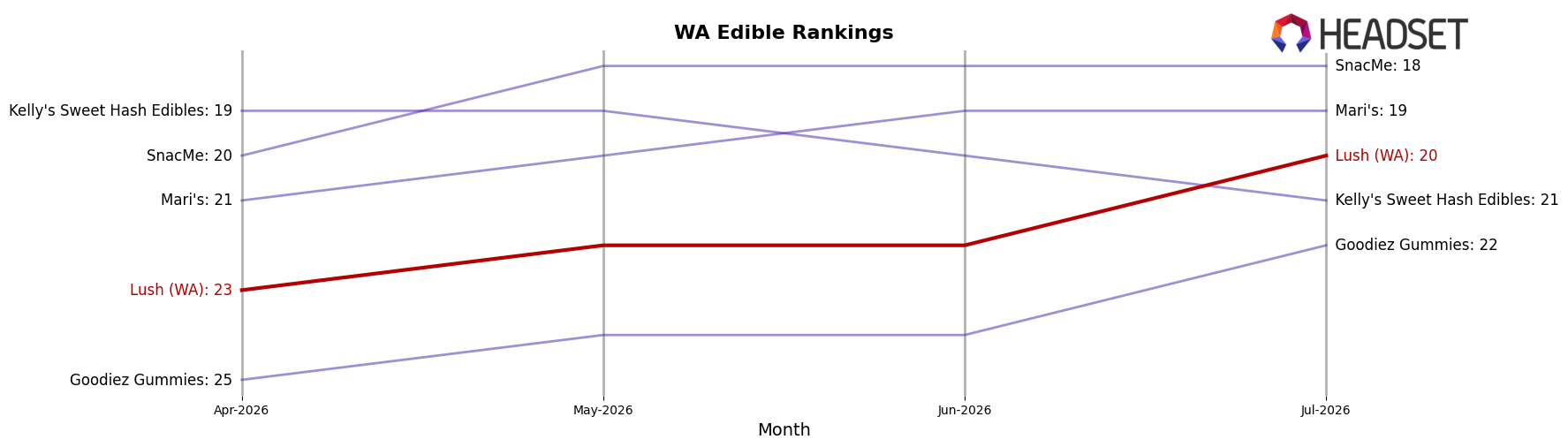

Lush (WA) sits at rank #20 in WA Edible for July 2026 with a 0-position YoY change from #20, while improving 3 ranks versus April 2026 from #23 to #20; against that steadiness, the brand’s peak of #16 in August 2024 marks a 4-position slide from its best point, indicating recovery without breakout. In contrast, Wyld holds #1 with a 0-position YoY shift and a 7.99% YoY sales increase, and Journeyman advanced from #5 to #4 with a 6.47% YoY lift, while Craft Elixirs moved the other way from #4 to #5 alongside an -8.01% YoY decline; this mix of upward and downward competitor movement alongside Lush (WA)’s flat YoY rank implies the brand is holding share but not converting category churn into upward rank momentum.

Notable Products

Lush - Hawaiian Mix Soft Jelly Chews 10-Pack (100mg) posted the largest move in July 2026 with a 60.5% month-over-month gain to $9,989 while climbing to rank 2, contrasting with Lush - CBG/THC 1:1 Sour Watermelon Fruit Chews 10-Pack (100mg CBG, 100mg THC) dropping 15.7% and still holding rank 1. Lush - Wild Berries Soft Jelly Chews 10-Pack (100mg) advanced 35.7% to rank 4, whereas Lush - Mango Lime Gummy 10-Pack (100mg) was essentially flat at -0.7% at rank 3, and five of the top ten are 1:1 CBD/THC SKUs that together indicate a tilt toward balanced formulations. This mix of a +60.5% surge alongside a -15.7% pullback implies a rotation within Lush (WA)’s gummy portfolio toward flavor novelty and balanced-dose formats rather than a uniform tide lifting all SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.