Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

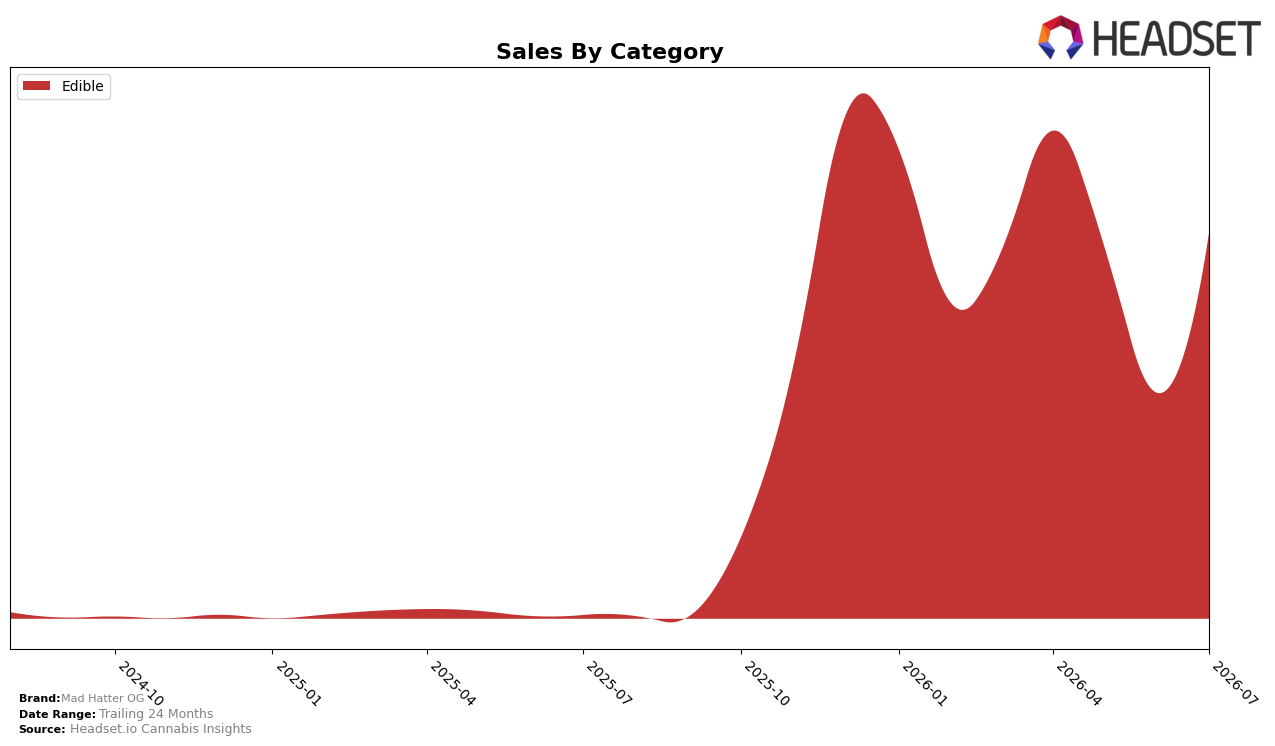

Edible accounted for 100.0% of Mad Hatter OG’s mix in July 2026, with month-over-month sales up 70.65% and a rank of 11 in Saskatchewan Edible. The single-category concentration alongside a 1,743.49% two-year sales increase implies deliberate consolidation around Edible that is translating into faster recent velocity than the broader portfolio would support, concentrating risk and upside in one lane.

Holding 100.0% in Edible while moving to rank 11 in Saskatchewan positions Mad Hatter OG as a specialist rather than a portfolio balancer, and the 70.65% month-over-month gain against a null year-over-year signal suggests momentum is recent and potentially timing-driven rather than seasonally entrenched. The implication is that near-term share capture will hinge on sustaining Edible throughput and price architecture around the current $25.45 average, because a single-category footprint can climb a few rank positions quickly on continued double-digit monthly growth but can also slip just as quickly if monthly comps normalize.

Competitive Landscape

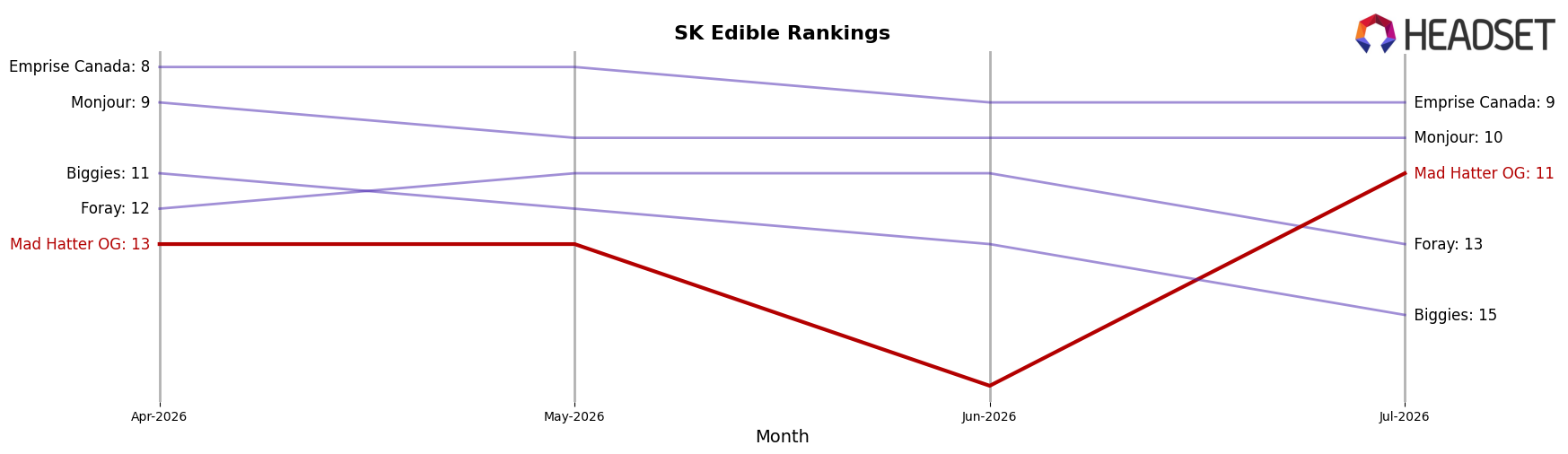

Mad Hatter OG is ranked #11 in SK Edible in July 2026, improving 2 positions from #13 in April 2026, and matching its peak rank of #11 in July 2026 while competitors at the top are shifting ranks by larger margins; for context, Wyld held #1 with a -7.8% year-over-year sales change, while Wana climbed from #10 to #4 alongside a 543.0% year-over-year increase, indicating that Mad Hatter OG’s gradual rank gain is occurring amid divergent competitor momentum and implies a steady share consolidation opportunity if the brand converts incremental rank wins into sustained mid-tier penetration.

Notable Products

Delta-8/THC 10:1 Raspberry Lime Zinger Gummies 10-Pack (100mg Delta-8, 10mg THC) posted a 70.6% month-over-month increase and moved into rank 1, indicating outsized momentum concentrated in a single Edible SKU. With no ranked presence for Mango Habanero Soft Chews 2-Pack (10mg) and one Edible accounting for $18,057 in July 2026, the assortment is concentrated rather than diversified. The combination of a +70.6% surge and a rank 1 position points to a near-term strategy centered on cannabinoid-ratio gummies rather than a broader portfolio push.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.